Personal Wealth Management / Economics

Jittery Over Bad Statistics?

How should we interpret December’s employment report?

Optimism showered headlines last week ... until Friday. Earlier in the week, ADP estimated private firms added 238,000 jobs in December, planned layoffs dropped to lowest levels since 2000 and even jobless benefits claims hit a monthly low. In turn, economists raised their forecasts for December’s official employmentdata—some expecting hires to hit 200,000. The result was a thud. Only 74,000 non-farm payroll jobs were added, far below consensus estimates. And while the unemployment rate dropped to 6.7%, many were quick to note it dropped for the wrong reason: Unemployed workers stopped seeking jobs (aka, the labor participation rate fell further). In the jobs reports’ wake, cue the fears of a stagnating US economic recovery. In our view, though, one month of relative weakness in a backward-looking economic indicator doesn’t have many forward-looking implications. In fact, some of these shifts—like the declining labor force participation rate—are so slow and gradual as to be near nonfactors as it pertains to markets.

As to the slow hiring, the Establishment Survey showed private sector employers added 87,000 jobs in total, with government employment detracting 13,000. Most blame the net 74,000 hires on cold and snowy weather. Perhaps that had an influence. After all, the construction industry shed 16,000 jobs and courier and messenger services another 6,400. Those seem like two areas fairly likely to be hit by bad weather. But we’d advise taking a broader view than any one individual month. It’s not the first time we’ve seen odd-seeming monthly employment data. March 2013’s initial report showed 88,000 hires versus expectations of 190,000. August 2011’s initial report showed zero hires. (Zero!) Both were subsequently revised up, to 205,000 and 132,000, respectively. Maybe cold weather kept some businesses from completing their surveys on time! Better to weigh the trend, which shows an average 182,000 per month. And better still to weigh the totality of employment data from official and private sector sources—no one report captures everything. And remember, jobs follow growth—not the other way around. There is little market forecasting value in lagging indicators.

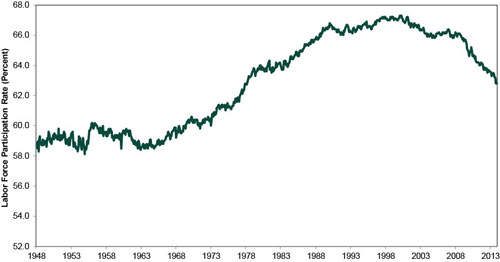

But even further removed from stocks is the labor force participation rate (LFPR). The 0.2 percentage point drop in the labor force participation rate to 62.8 percent disappointed many—folks are quick to allege this shows more “discouraged workers.” But there is likely another force at work: Demographics. In the 1960’s, the Labor Force Participation Rate rose steadily, largely due to women entering the workforce. It continued rising in the go-go 1970s as the baby boom generation entered their prime working years. (Yes, the go-go 1970s. That’s a joke.) It continued to rise in the 1980s. But note, there is little-to-no tie to economic growth or the stock market in this statistic. Bulls and bears, recession and expansion—the overall LFPR trend up was temporarily affected by recession, but then went right on with its trend.

Exhibit 1: US Labor Force Participation Rate, 1948 – 12/2013

Source: Federal Reserve Bank of St. Louis.

In the 1990s, LFPR growth slowed to a crawl, beginning the US’s longest expansion at 66.2% and ending at 67.0%. Not much of a move, given a decade-long, US-led economic boom. LFPR fell during the 2001 – 2007 expansion, even though the labor force itself reached an all-time high—working age population just grew faster (a factor many countries would envy). The same is largely true of this expansion. Ratios have two sides, and focusing on the numerator while ignoring the denominator tells half a story.

Overall though, there is just little evidence this statistic means much for market or economic direction. We’re sure there are unfortunately some discouraged workers, but it just doesn’t explain the slower rise in the total workforce. Perhaps it is in part due to the rise in retirees as Boomers age. Or the fact 21.8 million students are expected to attend American colleges or universities in 2013, roughly 6.5 million more than 2000. According to BLS data, nearly twice as many workers are out of the workforce due to “school or family responsibilities, ill health, and transportation problems, as well as a number for whom no reason for nonparticipation was determined.” And the numbers of discouraged and other workers not in the labor force have actually decreased throughout this jobs recovery, making it difficult to blame the decreasing LFPR on a so-called jump in discouraged workers. Further, those who decided to drop out of the labor force could very well change their mind soon—monthly data can be fickle. Every month a few million people re-enter the labor force.

Would a sustained trend of consistent re-entry make the unemployment rate rise? Quite possibly, yes. But that says more about employment data’s lag and wonky calculation than the economy.

But some still believe this report suggests the US economy is decelerating. We believe investors would get much more actionable, useful data from forward-looking indicators like ISM manufacturing new orders data, which rose to 64.2 in December, healthy corporate balance sheets, rising profits and rising Leading Economic Indexes—not just in the US, but globally. And since job growth lags economic growth, as economic growth continues to strengthen, we’d expect the employment situation to follow.

Last week’s reaction to employment data provided some evidence we’re still teetering between skepticism and optimism. Though, that’s not necessarily a bad thing, especially for markets! The longer it takes for people to move toward optimism, the longer the bull market likely lasts.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today