Personal Wealth Management / Market Analysis

Keep Calm as We Brexit On

Taking stock of the Brexit vote’s second anniversary.

June 23 marked the two-year anniversary of the UK’s narrow—52% to 48%—vote to leave the EU. For some, it also marks the two-year anniversary of waking up in a cold sweat, paralyzed by bear market and EU collapse fears. Two years later, Brexit hasn’t proven disastrous for markets. Actually, not much has changed—nor does it appear likely to in the near term. Parliament remains gridlocked, and despite some recent choppy data, UK economic fundamentals are sound. While it is always possible Brexit negotiations deteriorate, we continue to believe any catastrophic breakdown in talks remains unlikely. Instead, as slow-moving public negotiations continue reducing Brexit uncertainty, we expect overly dour sentiment to improve.

Where Do Negotiations Stand Today?

Despite initial fears of a rushed breakup, the multi-phase Brexit negotiations are plodding along. (Exhibit 1) In Phase 1, politicians drafted the “divorce bill,” determined post-Brexit EU/UK citizens’ rights and debated options for keeping the Irish border physically free and open once it becomes an EU border. While many aspects of these issues (notably, the Irish border) remain unresolved, late last year the two parties agreed to move into Phase 2’s trade relationship and transition-period talks anyway. Thus far, trade negotiations are proceeding glacially. However, the UK and EU agreed to a transition period, granting Brits access to the EU’s single market through December 31, 2020—well beyond the scheduled Brexit date of March 29, 2019. This date could even be extended—EU officials hinted at extending the two-year negotiation period recently. Negotiation progress is possible at this week’s EU summit, but sweeping change is unlikely, especially considering leaders remain preoccupied with the issue of migration. Some EU leaders—most notably Spanish Foreign Minister Josep Borrell—have signaled they will reject UK Prime Minister Theresa May’s proposal to keep the UK in the EU’s single market for trade in goods while revoking the free movement of people. As we have long argued, this process will likely be slow and grinding and play out very publicly. The chance of a shocking surprise from Brexit proceedings is, therefore, very low.

Exhibit 1: Brexit Timeline

Source: Various EU media.

Additionally, Prime Minister Theresa May’s minority government remains gridlocked and divided over Brexit. Lawmakers have already revolted over parts of the EU Withdrawal legislation, and May spent heaps of political capital to see off an amendment that would have enabled Parliament to set the agenda if Brexit negotiations fell through. This divisive and near-exclusive focus on Brexit proceedings helps bar potentially problematic non-Brexit-related legislation from passing. About the only significant non-Brexit measure passed since last year’s snap election was Tuesday’s bill approving a third runway at Heathrow airport. This is gridlock taken to the extreme.

Fundamentals Aren’t Gangbusters, But They Are Largely Fine

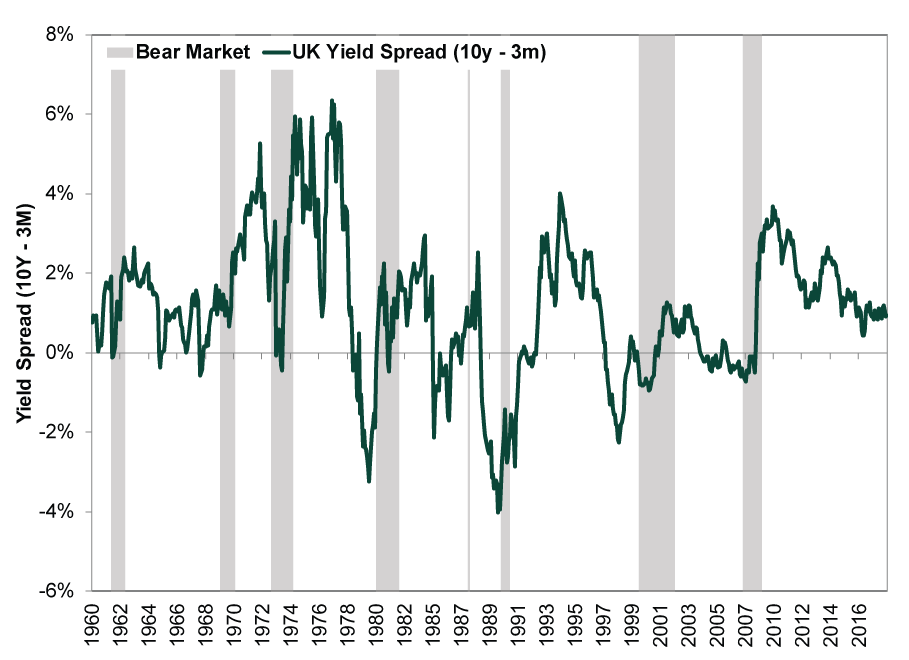

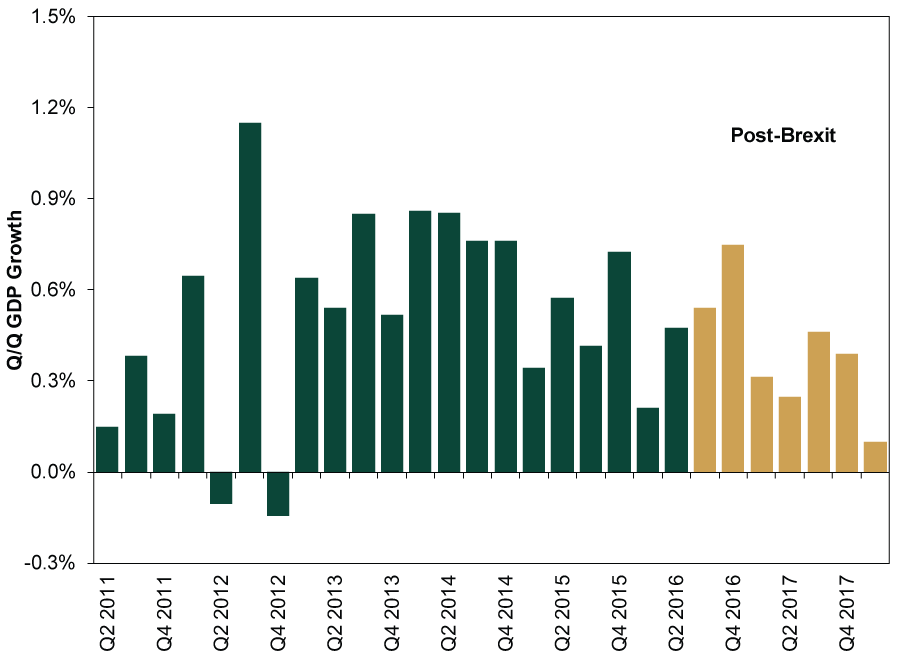

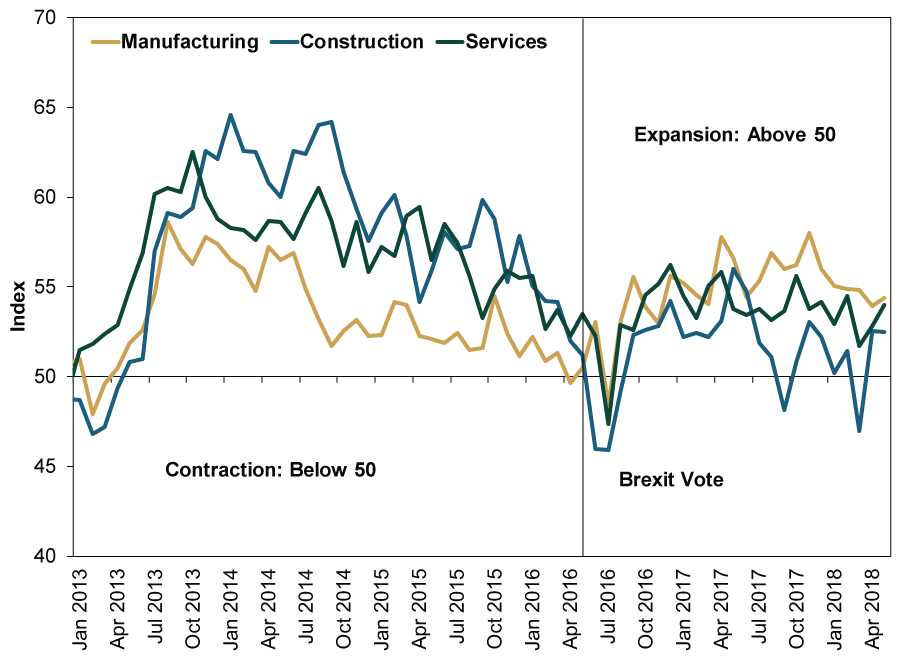

Meanwhile, most forward-looking UK indicators and other economic data continue to prove more resilient than expected. The UK yield spread remains mildly positive (Exhibit 2), which has helped lending and broad money supply (M4) grow approximately 4% y/y.[i] Despite persistent UK recession fears, GDP has grown in all seven post-Brexit quarters. Q1 2018 was weaker, but that is likely (at least in part) due to harsh winter weather, a temporary factor. (Exhibit 3) Aside from July 2016’s sentiment-driven blip tied to the Brexit vote, Services and Manufacturing Purchasing Managers’ Indexes (PMI) have been uniformly expansionary the past two years. (Exhibit 4)

Exhibit 2: UK Yield Spread

Source: Global Financial Data, Inc., as of 6/25/2018. 10-year and 3-month gilt yields, January 1960 – June 2018.

Exhibit 3: UK GDP Growth

Source: FactSet, as of 4/16/2018. Q2 2011 – Q1 2018.

Exhibit 4: UK PMIs

Source: FactSet, as of 6/6/2018. Markit UK Composite Purchasing Managers’ Index January 2013 – May 2018.

Sentiment Still Sour

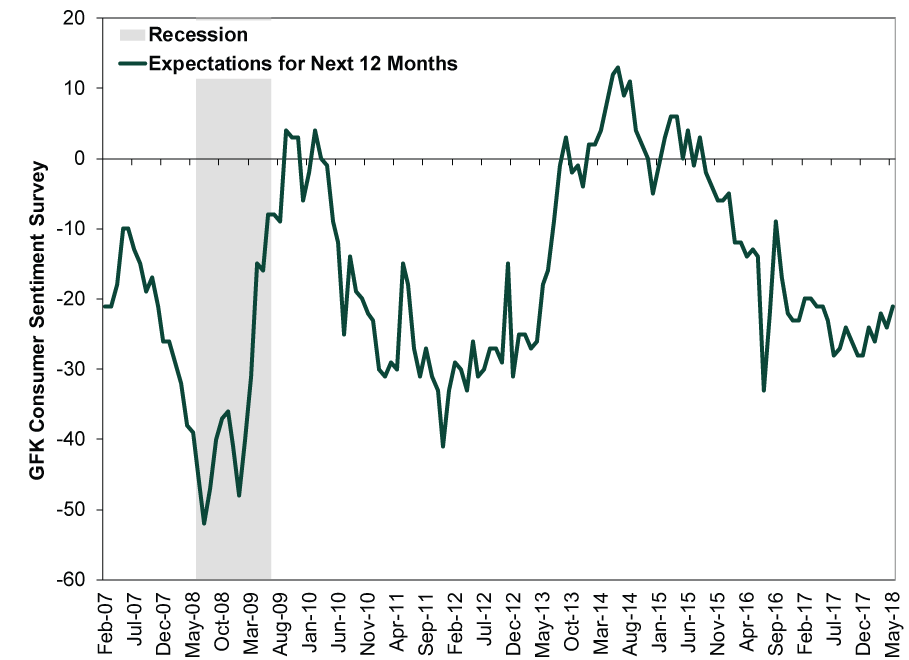

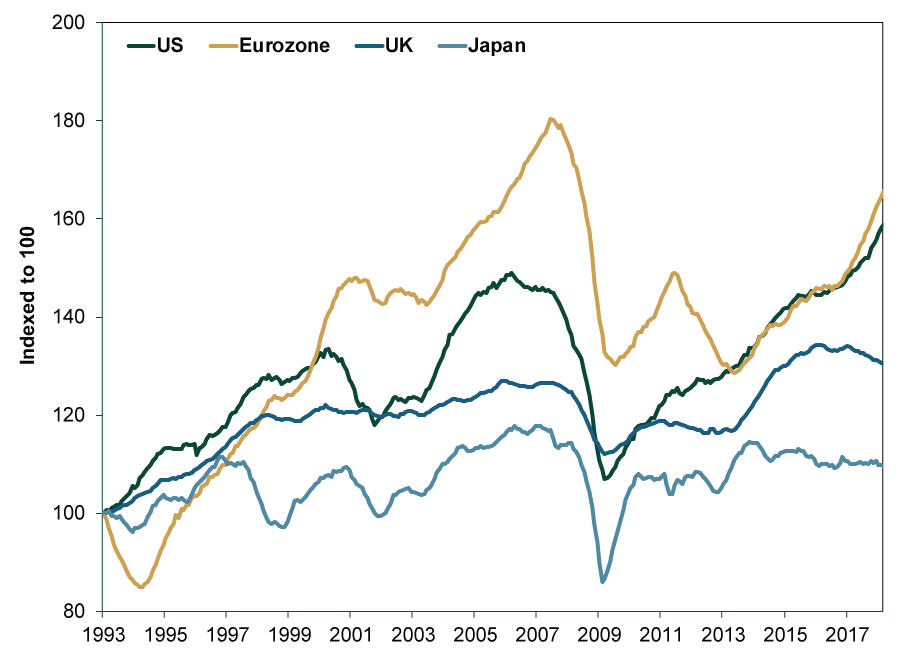

However, sentiment remains dour. Media continue portraying Brexit as a potential calamity, hyping stalled talks, “hard” Brexit risk, the grassroots campaign for a second referendum and more. Meanwhile, sentiment gauges like consumer expectations for the UK economy linger around Brexit lows. Moreover, because The Conference Board revised its UK Leading Economic Index (LEI) in 2016 and heavily weighted sentiment gauges, this has caused a string of dips in UK LEI. (Exhibits 5 & 6) This makes the UK outlook seem weaker than other economic measures suggest.

Exhibit 5: UK Consumer Expectations

Source: FactSet, as of 6/5/2018. Consumer expectations over the next 12 months, February 2007 – May 2018.

Exhibit 6: Major Leading Economic Indexes

Source: The Conference Board, as of 6/5/2018. US, eurozone, UK & Japan Leading Economic Index (LEI), January 1993 – March 2018. Copyright The Conference Board, Inc. Content reproduced with permission.

The Sentiment – Fundamentals Disconnect

While we normally view such a big disconnect between overly dour sentiment and a fine reality a big positive for stocks, UK markets might remain caught in a sentiment-related tug-of-war. Although we expect the eventual Brexit agreement to bring far fewer disruptions than many in the media foresee, the uncertainty surrounding talks can impact risk-taking. When businesses are waiting to see what the new rules look like, they may delay long-term investments. The lingering fog could also prevent investors from getting too excited about UK stocks in the near term. Overall and on average, we believe slow-going Brexit negotiations give stocks the ability to see changes coming at them with plenty of advance notice, reducing big shocks. But dreary sentiment, combined with UK markets’ heavy commodity-related bent, could prevent UK stocks from outperforming in the near term.

[i] Source: Bank of England, as of 6/26/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today