Personal Wealth Management / Market Volatility

Lessons From a Choppy Nine Months

The past nine months illustrate the importance of not overreacting to past market movement.

Imagine you fell asleep, dear MarketMinder reader, on September 30, 2018 and pulled a Rip Van Winkle—waking up on June 30, 2019. Naturally, the first thing you do is check what global stocks did over this time.[i] You discover they returned 1.3%.[ii] Ok, but kind of meh. Must have been an uneventful stretch, right? Not much missed? Wrong! In our view, the past nine months illustrate the importance of not overreacting to past market movement. Whether down, up or flat—what stocks just did tells you nothing about what is coming next.

Here are a thousand words in picture form:

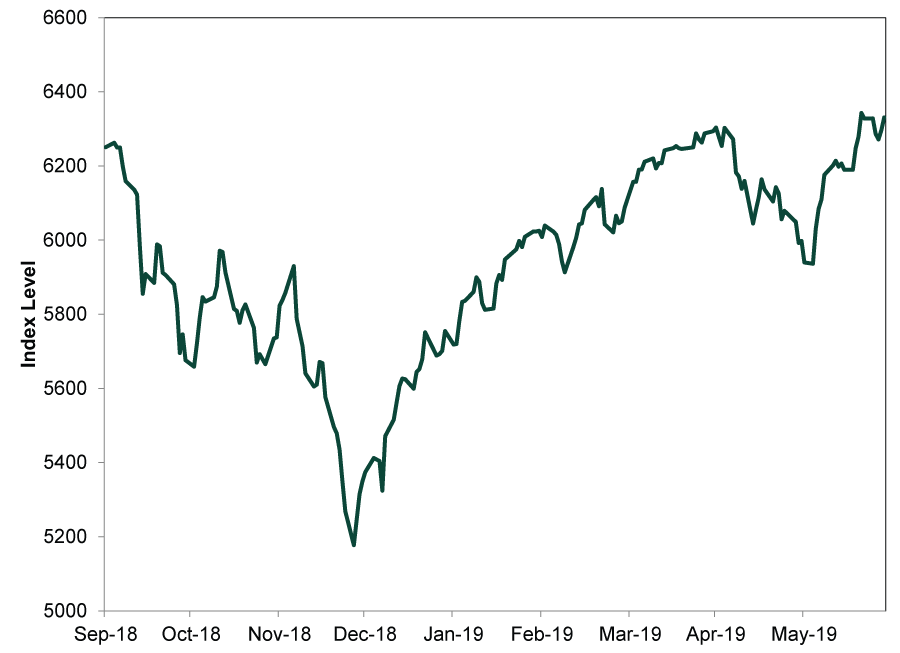

Exhibit 1: Global Stocks’ Wild Ride

Source: FactSet, as of 7/1/2019. MSCI World Index return with net dividends, 9/30/2018 – 6/30/2019.

For those who prefer numbers, global stocks fell -17.5% from the end of September through Christmas.[iii] US stocks fared even worse, dropping -18.9%.[iv] Q4 2018 was the S&P 500’s worst quarter since 2011, convincing pundits a bear market (a long, fundamentally driven decline exceeding -20%) was all but assured. But just as things looked their darkest, stocks rebounded—sharply. In Q1 2019, the S&P 500 enjoyed its best quarter since 2009—and just had its best first half since 1997. Global stocks are up a strong 17.0% over that timeframe.[v] It is the best start to a year since the 1980s.

With global markets up nicely, it may seem obvious today holding stocks was the way to go. Though many stock investors are aware short-term, uncomfortable volatility is the price tag for stocks’ high longer-term gains, paying this price—and staying cool—is often easier said than done. Data show many investors struggled to stay disciplined during December’s rout. Last December’s stock mutual fund outflows matched March 2009’s—the last bear market’s bottom. Fund flows are imperfect since they tell you only one half of a decision—what investors did with the proceeds isn’t addressed—but when they are at extremes, they speak volumes about sentiment. Extreme dour sentiment was everywhere before stocks rebounded—a phenomenon Fisher Investments’ Founder and Executive Chairman Ken Fisher described in his USA Today column, “Worried About Markets? Remember ‘V’ Is for Victory.”

But just as the left-hand, downslope of the V doesn’t last forever, neither does the right-hand’s climb. After soaring 22.3% from December’s bottom through April, global stocks then lurched downward -5.8% in May.[vi] US stocks slid -6.4%, the worst May since 2010 and second-worst since 1962.[vii] Again headlines freaked. Fund outflows jumped. Sentiment, generally, plunged. All right before a June rally, with world stocks up 6.6% and US stocks posting their best June since 1955.[viii] These “milestones” (including the S&P 500 breaching 3000 this week) are mere trivia. But the movement is also an illustrative example of how volatile stocks can be in the short term—both to the downside and upside. That positive volatility drives much of the positive gains constituting bull markets.

Despite a strong first half of the year, pundits remain focused on negatives. False fears—e.g., global trade tensions, slowing economic growth, fluctuating oil prices—still weigh on sentiment and dictate market narratives. Yet stocks are forward looking. They have already priced in those widely discussed stories and moved on. They don’t much mind about past price movement, either—whether negative or positive. Keep this in mind when folks start fretting over all-time highs. Just an arbitrary milestone—only a reflection of past market movement. The fact July 4 was the MSCI World’s 195th all-time high in this bull market should be evidence enough there isn’t anything predictive about records.[ix]

We believe there are still more all-time highs to come, too. The global expansion remains intact, with growth better than most appreciate—particularly in Europe. Gridlock persists across most major economies, decreasing the likelihood of market-upsetting major legislation. Persistently dour sentiment points to more wall of worry for stocks to climb. Even if stocks’ rise is bumpier and slows compared to the first half of the year, we believe stocks will keep climbing through at least 2019’s close.

[i] If you checked the sports and entertainment pages first, you would discover Tiger Woods won the Masters Tournament and another Toy Story movie came out. You may be forgiven if you thought you traveled back in time and woke up in the late 1990s.

[ii] Source: FactSet, as of 7/1/2019. MSCI World Index return with net dividends, 9/30/2018 – 6/30/2019.

[iii] Source: Ibid. MSCI World Index return with net dividends, 9/30/2018 – 12/25/2018.

[iv] Source: Ibid. S&P 500 Total Return Index, 9/30/2018 – 12/24/2018.

[v] Ibid. MSCI World Index return with net dividends, 12/31/2018 – 6/30/2019.

[vi] Ibid. MSCI World Index return with net dividends, 12/25/2018 – 4/30/2019 and 4/30/2019 – 5/31/2019.

[vii] Source: Global Financial Data, Inc., as of 6/28/2019. S&P 500 rolling three month total returns, December 1925 – June 2019.

[viii] Ibid.

[ix] Source: FactSet, as of 7/1/2019. MSCI World Index with net dividends, 3/9/2009 – 6/30/2019. The prior bull market’s all-time high was on 10/31/2007, initially eclipsed on 5/7/2013—more than six years ago.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today