Personal Wealth Management / Economics

Manufacturing a Connection

Alleged connections between manufacturing’s contraction and the fiscal cliff seem, well, manufactured.

When the ISM announced its gauge of US manufacturing contracted a bit in November, most reports saw it as evidence of one of two things: a weakening US economy or the fiscal cliff’s potential impact.

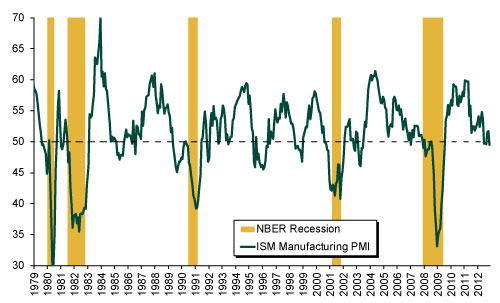

In our view, it’s neither. Monthly data are volatile, and manufacturing’s no exception. Short-term contractions regularly occur amid long-term expansions. Manufacturing contracted a few times during each of the past three economic expansions, without much disrupting the economy’s overall progress (Exhibit 1).

Exhibit 1: ISM Manufacturing Index (Above 50 Indicates Expansion)

Sources: ISM, NBER, Thomson Reuters, as of 12/3/2012.

November wasn’t manufacturing’s first contraction of this cycle. That occurred from June through August, partly coinciding with US GDP growth’s acceleration in Q3. November’s small contraction is likely another blip in this spate of volatility, not a sign of mounting economic weakness. The ISM seemingly agrees, as its report deemed the broader economy to be in its 42nd month of expansion—not surprising when you remember manufacturing’s less than 15% of our economy, and our robust service sector’s chugging along more or less fine.

Looking at the report’s different components helps mitigate the headline contraction. New orders and production continued expanding, though at a slower pace than October. Imports grew, suggesting a small increase in domestic demand. Much of the contraction came from shrinking employment—a backward-looking indicator—and falling exports, which imply the volatility isn’t truly much driven by anything domestic (*ahem, fiscal cliff). Inventory drawdowns, another source of contraction, aren’t necessarily a negative—firms that slash inventories will likely need to boost production to meet future demand increases.

Some outlets suggested that when taken in context with the many international surveys released the same day that showed improvement, the US’s weakness means it’s falling behind globally. To us though, the data don’t support this claim. Sure, eurozone manufacturing improved, but it remained well in contraction for the 16th straight month. South Korea and the UK also saw notable improvement, but they remained in contraction for the sixth and eighth month, respectively. Vietnam grew, but for the first time in 14 months. Both Chinese manufacturing surveys expanded, but only a bit—and the expansion followed over a year of weakness. US manufacturing may have moved in the opposite direction from these areas in November, but if you look at a larger time sample, the US hardly resembles a global weakling.

Other outlets suggested manufacturing’s contraction signified something else: The big bite they believe the fiscal cliff could take out of the US economy. In an interview, the chairman of the ISM’s survey said more manufacturers registered concern about the cliff in November, suggesting uncertainty over whether and how Congress will avert the cliff caused them to hit the brakes. Perhaps there’s some truth to this. Some business owners might not expect Congress to compromise on the cliff, and they might have adjusted payrolls and other aspects of their business according to their expectation for rising taxes. But it’s difficult to imagine all businesses holding back all activity today in anticipation of higher taxes tomorrow. Typically, it’s the reverse—if folks expect taxes to rise, they’ll pull forward as much activity as they can to take advantage of soon-to-expire lower rates. Hence, if businesses truly dreaded the fiscal cliff, we might see a surge of activity in November and December. But there’s not much evidence firms are trying to beat the clock.

Even if businesses are treading lightly while they await more clarity over the cliff, that only speaks to businesses’ tendency to sit tight amid regulatory uncertainty. That’s not unique to the cliff. And in those scenarios, simply getting clarity often provides a measure of relief. Thus, if firms are indeed in “wait and see” mode today, we might reasonably expect the release of some pent-up activity once Congress reaches a deal.

None of this is to say all is rosy in the US—risks and economic headwinds always exist. But November’s manufacturing report is only one snapshot of one small piece of the global economy at one point in time—a time, remember, when a nasty hurricane took some factories offline in the northeast. Plenty of other data continue pointing to a healthy and growing US.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today