Personal Wealth Management / Economics

Markets Don’t Discriminate Between “Hard” and “Soft” Economic Data

"Hard" or "soft," economic data point to positive growth.

You may have heard of big data, but what about "hard" and "soft" data? The distinction is the latest source of economic handwringing. Hard data tell you what happened. How many widgets were produced or sold (or booked for sale) for how much in this time frame and for that sector or industry. Soft data are surveys that measure emotion and businesses' guesstimates on how things are going. But while soft data are largely soaring, hard data aren't. Many warn this means sentiment is stretched and stocks will struggle as they're forced to accept a reality of slower-than-expected growth, but this seems a rather hasty conclusion.

While the hard vs. soft data debate seems esoteric, it is stirring a lot of handwringing in economic circles. Soft surveys like purchasing managers' indexes (PMI) and consumer sentiment usually come out before hard data and help form analysts' expectations for the latter. Hence, when ISM's manufacturing PMI zoomed to 56.0 in January and 57.7 in February-and non-manufacturing hit 56.5 and 57.6 in those months, respectively-folks cheered and expectations rose.[i] PMIs over 50 indicate expansion, and those readings were far above 50. But hard data, on the surface, didn't keep pace. Industrial production (IP) fell -0.1% m/m in January and was flat in February.[ii] Retail sales rose 0.6% m/m in January but cooled to 0.1% in February.[iii]Broader consumer spending, adjusted for inflation, fell -0.2% m/m in January and -0.1% in February.[iv] Sad!

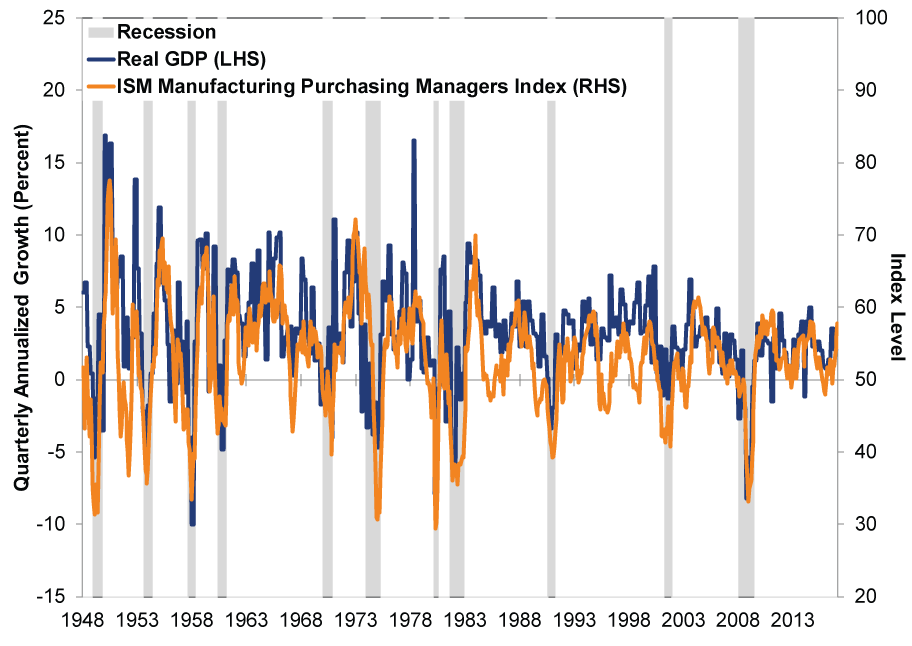

Stocks do move on the gap between reality and expectations, but not every hard data point must beat forecasts, and markets care more about the entire economic landscape. Hard and soft data alike paint that picture, and it is currently one of fundamentally sound economic growth. Different indicators show different magnitudes, but directionally they mostly match. Moreover, it shouldn't be breaking news that PMIs don't match harder data. They measure how many firms grew, but not by how much. Strong PMIs mean widespread growth, but you can't translate that to a specific magnitude. Q1's PMIs merely tell you first quarter growth was probably positive, which stocks already know. (Exhibit 1) Forward-looking stocks move on long before GDP figures come out.

Exhibit 1: PMIs and GDP Track Decently

Source: FactSet and Federal Reserve Bank of St. Louis, as of 4/4/2017. NBER recession data used for shading.

Ken Fisher often likens quibbling over whether growth is faster or slower to arguing over how many angels can dance on the head of a pin-the height of pointlessness for investors. Just look at the big picture. Are GDP's main private sector domestic components positive or negative? Are PMIs comfortably above or below 50? Is the yield curve positively sloped or inverted? In concert, those will tell you whether economic growth supports stocks. How these data relate to expectations does matter from a relative return standpoint-perhaps why European returns topped US in Q1. But directionally, growth is growth.

Details, Details

Both sides of the "hard/soft divide" commit the error of taking headline data as gospel without looking deeper. For instance, hard data like IP, new orders for "core" capital goods (nondefense capital goods excluding aircraft) and business investment (real private nonresidential fixed investment) have been weak in recent years. However, that was primarily due to a huge drop in energy investment during and after 2014 - 2015's oil price fall. Oil's recovery brought a nascent rebound, visible in new orders for oil and mining-related machinery. More recently, IP's early-2017 weakness was tied to utilities, as warm winter weather hit gas and electricity usage. Manufacturing and mining production (including oil and gas drilling) grew both months.

Consumer spending's early-year dip, meanwhile, was mainly due to a December surge coupled with weaker auto sales and the aforementioned weather-related utility slump. Average spending in Q1's first two months still tops Q4's average, implying growth thus far. Plus, we're in April, dissecting February results. Markets already moved on.

Fretting over financial data (sort of hard data?) is similarly suspect. Take US bank lending, particularly business lending, which fell in December and February. March's weekly data was down, too. This isn't great news, but isolated lending pullbacks aren't unusual in an expansion. Furthermore, business lending was negative for this expansion's first two-plus years. This wee blip bears watching but isn't inherently a harbinger of doom.

Stick to What Works

Ultimately, different data tell you different stuff. No economic data are actually all that "hard" in a scientific sense. Just different. Even GDP-economists' hard data granddaddy of 'em all-has softer aspects. Inventory change, for example, is considered hard data. But the interpretation of it is squishy as heck applied to what it means for the private sector. One could say the same of government spending. It adds to growth, but is it necessarily "good" for publicly traded companies? Economists have debated that since Keynes and Hayek were alive.

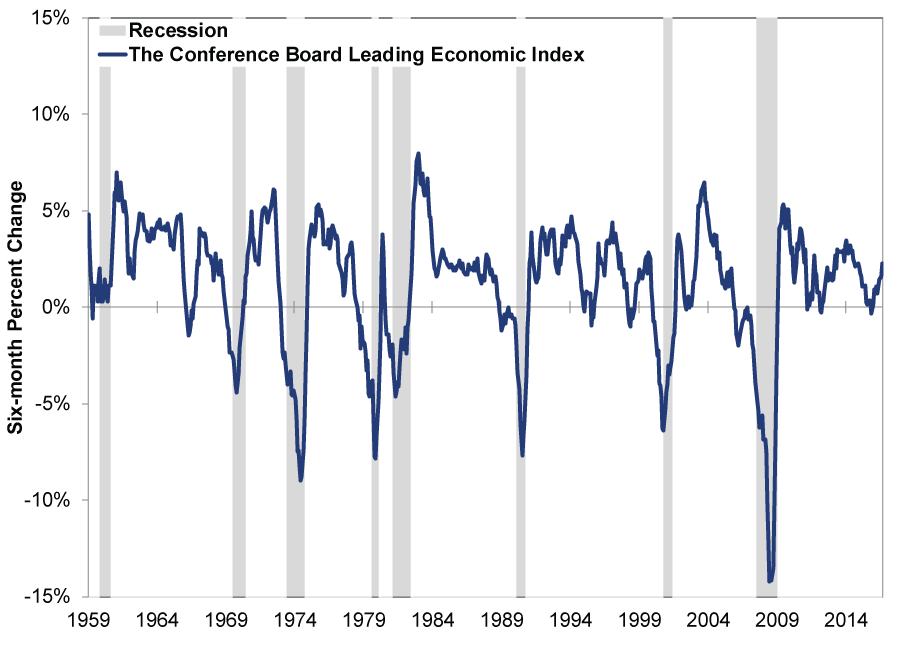

Assessing where things will go, which markets care most about, requires analysis of hard, soft and financial data-and relating those to expectations. We recommend paying most attention to economic gauges with historical successes like the Conference Board's Leading Economic Index (LEI)-a mixture of hard and soft data, as well as financial market indicators like the S&P 500 and the yield curve. (Exhibit 2) No recession in its nearly 60-year history has ever begun when it is high and rising-as it is now.

Exhibit 2: No Recession Ahead

Source: FactSet and Federal Reserve Bank of St. Louis, as of 4/4/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

-

Market Analysis The Investment Implications of Record-Low Consumer Sentiment2026-05-19

-

Market Analysis More Positive Surprise in Japan’s Q1 GDP2026-05-19

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today