Personal Wealth Management / Market Analysis

Chart(s) of the Day: Remember That Manufacturing Recession?

A look back at when manufacturing data spooked folks.

The beginning of the month means different things to different people.[i] I call the first business day of the month PMI Day to celebrate the release of the latest purchasing managers' indexes.[ii] The fine folks at the Institute for Supply Management released their March manufacturing PMI on Monday, and while it was solid (57.2), there is a more interesting takeaway. Go back in time, just a little more than a year ago, and folks feared several weak manufacturing PMIs heralded a "manufacturing recession" that could lead to broader problems. Those fears are now long forgotten, and the latest data confirm those contractionary months were a soft patch rather than the start of lasting weakness. Manufacturing has flipped from modest headwind to minor tailwind, one of many underappreciated economic drivers underpinning this bull market.

Let's rewind 13 months and check out some headlines from that time[iii]:

- US Manufacturing Index at Worst Level Since 2009 (1/4/2016)

- US Manufacturing Teeters on the Edge of Recession (1/29/2016)

- US in Longest Manufacturing Recession Since 2009 (3/1/2016)

Sounds bad! The cause of concern: The ISM's manufacturing PMI fell below 50 in October 2015 and stayed there for five straight months, implying a five-month contraction.[iv] PMI are monthly surveys that measure economic activity across various sectors, and responding firms say whether activity rose or fell. As ISM explains, "A PMI reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally declining."[v] Combine weak manufacturing PMI readings with flagging industrial production-and all the market volatility at 2016's start-and US recession fears ran rampant.

However, with the benefit of hindsight, manufacturing PMI's weak stretch now looks quite temporary.

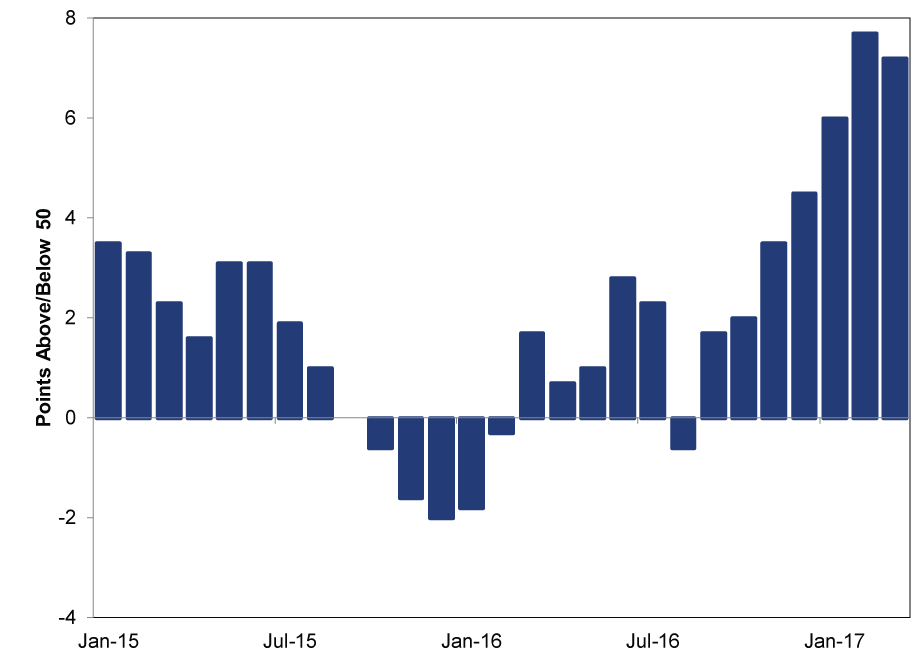

Exhibit 1: ISM Manufacturing PMI From January 2015 - March 2017

Source: FactSet, as of 4/4/2017. The ISM didn't skip September 2015-the reading was 50.0.

Since that contractionary streak ended, manufacturing PMI has exceeded 50 in 12 of 13 months, and the US economy grew 1.6% in 2016.[vi] Slower than recent years, yes, but not an outlier for this expansion. Those concerns about a manufacturing recession spilling into the broader economy were just a wee bit off.

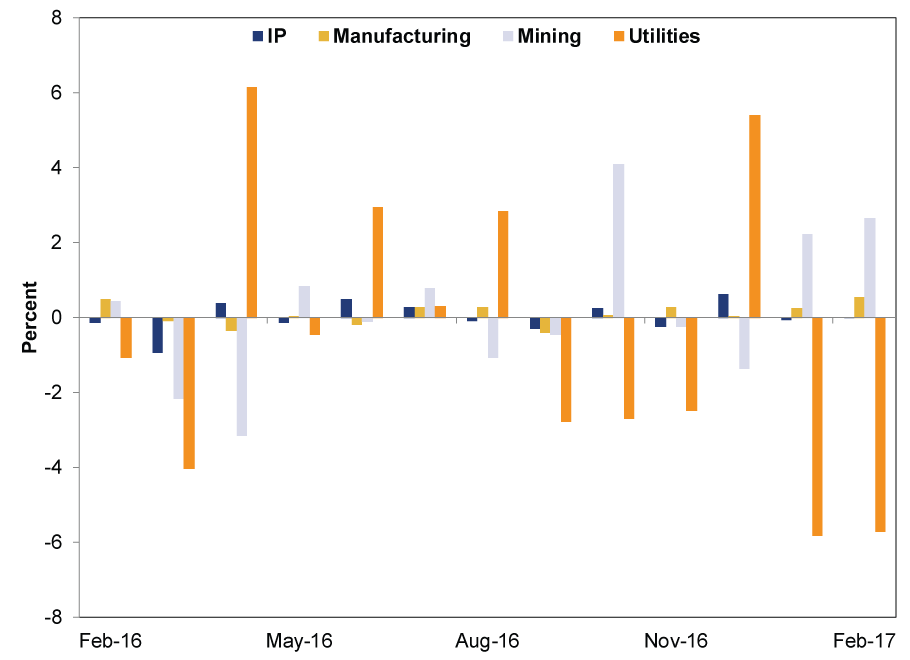

Admittedly, while manufacturing PMI has bounced back bigly, other heavy industry data haven't. For example, industrial production (IP) also fell on a monthly basis during manufacturing PMI's soft patch. But whereas PMI's weakness ended in early 2016, IP's struggles continued: up in six months, down in six months through February 2017. However, it isn't because IP has been broadly weak. Rather, one subsector has weighed on the headline number. (Exhibit 2)

Exhibit 2: Industrial Production and its Subsectors Over the Past 12 Months

Source: FactSet, as of 4/5/2017. Monthly growth rates from February 2016 - February 2017.

Utility output contracted in five of the past six months, and as the Federal Reserve notes, "continued unseasonably warm weather further reduced demand for heating."[vii] The manufacturing subsector-a pure measure of American factories-has been much steadier, and though not gangbusters, it isn't weak, either. Moreover, slow but steady manufacturing growth isn't in conflict with expansionary PMI. PMIs indicate the breadth of growth but not the magnitude-one of its limitations. Overall, both the "hard" and "soft" data show manufacturing is doing better than many may think.

However, this is just one month of one dataset in one part of the vast American economy-and manufacturing doesn't make up a majority of economic activity. But any positive economic surprise is good news. With more data rolling out-the non-manufacturing PMI signaled expansion for the 87th straight month in March and forward-looking new orders were up nicely-stocks have plenty of economic support. The US-and global for that matter-economy is chugging along.

[i] Payday if you're an optimist, bill paying if you're a pessimist.

[ii] True story. Ask my colleagues.

[iii] #ThrowbackThursday, anyone?

[iv] Here is where I quibble with using the term "recession." Recession is typically cited in regards to GDP, and under its technical definition, two consecutive contractionary quarters = recession. So while the manufacturing PMI contracted for one quarter (three months), it wasn't quite two. Maybe they used September as the starting point, since PMI was flat, exactly 50, then? But even so, flat ain't down.

[v] I don't want to get too deep in the weeds here (though that's what footnotes are for), but per the ISM's methodology, a PMI above 43.3 over a period of time generally means GDP is expanding. So just because a PMI is below 50-even for a couple months-doesn't mean broader economic contraction.

[vi] Source: FactSet, as of 4/5/2017.

[vii] The Fed clearly wasn't judging based on the West Coast this winter. It was chilly (relatively speaking) and wet in the Bay Area. Portland was a downright mess.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 1 - June 52026-06-08

-

Market Analysis Latest Tariff Threats Lack Terror for Markets2026-06-08

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, Global Trade, ECB Meeting

2026-06-08

2026-06-08 -

Expert Commentary This Week in Review | Upcoming IPOs, US Jobs Data, Credit Card Delinquencies

2026-06-05

2026-06-05

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today