Personal Wealth Management / Market Analysis

Mnuchin Mnipulating the Dollar? We Don't Think So

The real takeaway from our Treasury Secretary’s infamous comment about the dollar.

Steve Mnuchin did not tear this dollar bill with mere words. It was already like that. Photo by Elisabeth Dellinger.

Spare a thought for poor Steve Mnuchin, our beleaguered Treasury Secretary who can’t just catch a break. First, he gets pilloried for posing with the first sheet of dollar bills bearing his signature, with the Internet likening him and his wife to movie villains. Then he makes a run-of-the-mill comment about currencies at Davos, reporters choose to hear only one sentence fragment, and suddenly the financial media is full of Mnuchin champions weaker dollar! Then came the knee-jerk trades sending the dollar to its lowest level in 10 months, followed by all the associated think-pieces and rebukes. Even ECB chief Mario Draghi got in on the fun, implying Mnuchin was violating earlier agreements not to start a currency war. We see two lessons here for investors. One: Don’t take headlines and hype at face value. Two: Neither a weak currency or strong currency is inherently best—which is basically what Mnuchin was trying to say.

Here, in full, is the statement that caused the maelstrom:

The dollar is one of the most liquid markets. Where it is in the short term is not a concern of ours at all. Obviously a weaker dollar is good for us as it relates to trade and opportunities. But again, longer term, the strength of the dollar is a reflection of the strength of the US economy and the fact that it is and will continue to be the primary currency, in terms of the reserve currency.

Now, we’d quibble with a few parts of that, since the trade impact is negligible-to-mixed. We have been waiting for Japanese goods to get cheaper over here since the yen weakened five years ago—they largely haven’t. To the extent currency moves do impact import and export prices, they usually offset each other. Also, the US doesn’t really get anything from the dollar being the world’s reserve currency. But the spirit of these comments—short-term currency fluctuations don’t really matter, and the weak dollar isn’t some huge negative—is spot-on.

Trouble is, nuance doesn’t make good headlines. Nor does good news. “Treasury Secretary Says Smart Thing About Weak Dollar Not Being Awful” doesn’t sell papers or attract clicks. So instead, we got the hype. From The Wall Street Journal: “The man whose signature is on the greenback tells the world he wants its value to be lower so the US can beggar its neighbors on trade.” From an economic research shop: “A cheapening dollar does not help sell US securities to people who have to finance the fundamental dissaving of the US economy.” From a market strategist: “The first serious economic misstep by the Trump Administration is the inexplicable decision to talk the dollar even lower.” From a prominent hedge fund manager: “Regarding Treasury Secretary Mnuchin’s comments about the administration’s weak dollar policy, I want to make sure that you understand what having currency weakness means—most importantly, it is a hidden tax on people who are holding dollar-denominated assets and a benefit to those who have dollar-denominated liabilities.”

Flummoxed by the backlash, Mnuchin tried again Thursday in an interview with Maria Bartiromo:

I thought my comment on the dollar was actually quite clear yesterday. I thought it was actually balanced and consistent with what I’ve said before, which is we’re not concerned with where the dollar is in the short term, it’s a very, very liquid market and we believe in free currencies. And that there’s both advantages and disadvantages of where the dollar is in the short term. Let me say I thought that was clear.

Fox Business’s recap adds this gem: “If you look at my full transcript from yesterday it was incredibly balanced, it was consistent with what I’ve said over the last year and it wasn’t news.” (Boldface ours, obviously, because you can’t boldface spoken words.)

That is all pretty innocuous! A Treasury Secretary talking up free currency markets and non-intervention seems like good news to us. A reminder that liquid markets are volatile is always timely. And an observation that the dollar’s short-term movements always bring plusses and minuses? So true! This is the same reason why the dollar and stocks aren’t linked. A strong dollar isn’t bad or good. A weak dollar isn’t bad or good. We have had bull markets and expansions alongside weak and strong dollars. We have also had bear markets and recessions alongside weak and strong dollars. Currencies always trade in pairs, and over time (provided we aren’t talking about banana republics), the movement is usually zero sum. The dollar stays in the same range where it has traded for decades because there is strong demand for American assets. This is generally true regardless of how relative interest rates and sentiment impact the dollar in the short term.

As for the handwringing about beggar-thy-neighbor currency policies, it is pretty clear from Mnuchin’s actual comments that this is nothing of the sort. A beggar-thy-neighbor-ist would advocate policy to manipulate the currency lower in an effort to boost exports. The Treasury would be goading the Fed into dumping its dollar reserves and snapping up foreign currencies. Saying the currency should continue trading freely because short-term levels don’t matter is anathema to a currency-focused protectionist. Needless to say, advocating a free-floating currency also doesn’t violate G-20 agreements not to artificially weaken currencies in order to gain a mythological trade advantage.

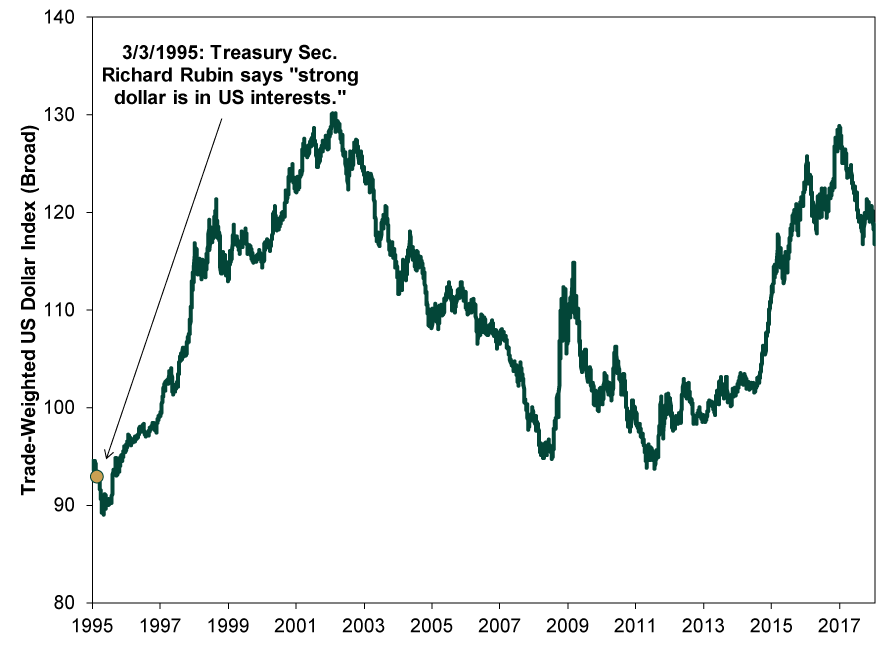

Besides, Treasury secretaries have stuck to this “strong dollar policy” for more than 20 years. In that time, the dollar has done this:

Exhibit 1: Not Always Strong, Despite the Sales Pitch

Source: Federal Reserve Bank of St. Louis, as of 1/25/2018. Trade-Weighted US Dollar Index, 1/4/1995 – 1/19/2018.

Treasury secretaries have talked up the strong dollar throughout the period that chart depicts. Now, perhaps they weren’t serious about those statements. Or perhaps they just can’t control currency markets to the extent commentators seem to presume. Considering currency traders often follow expected relative yields, we would humbly suggest the latter is more likely at play. Hence, whether you believe the selected quote or the full quote in context isn’t the only thing that matters.

So we suggest investors do their best to tune out currency noise and stay above the fray. By all means, watch what public officials say (and much more closely watch what they do), but make sure you get the whole story. Soundbites aren’t helpful. Analysis requires full sentences, paragraphs and context. A bullet point or snappy phrase isn’t sufficient. That, folks, is the boring truth. Have fun.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 6 - July 102026-07-13

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today