Personal Wealth Management / Financial Planning

Money Market Reforms, Libor and You

Looming rule changes for money market funds likely won't imperil credit markets.

Money market funds typically get little coverage in the financial press because, except under extreme circumstances, they don't rise or fall in value. Boring! But that's about to change, as new rules will soon require institutional prime money market funds to report their real-time market value and hold more liquid assets. Many worry this will dry up short-term funding markets, as money market funds are one of the primary investors in commercial paper. Sure enough, Libor rates have risen lately, driving fears of "stealth tightening" in credit markets. While the nervousness is understandable, it's unlikely major turmoil lies ahead.

The London Interbank Offered Rate, better known as Libor, is the average rate banks pay to borrow from each other over short time periods. It is also the reference rate for many bank loans-hence why people are worried about the apparent spike. The volatility is quite simple to trace to the money market fund reforms, which take effect on October 14. Money market funds have long invested in commercial paper for its yield (which exceeds T-bills), offering investors a way to hold "cash" with a higher return than a plain old bank deposit. But the looming rule changes will require prime institutional money market funds to have floating net asset values instead of being fixed at $1 / share-regulators' attempt to prevent a repeat of the panic that ensued when one huge money market fund "broke the buck" in 2008, triggering a run on money market funds.[i] The rules also impose liquidity requirements and tighter restrictions on portfolio holdings, and many fund providers have decided to switch from prime funds to funds that invest primarily in government debt, which regulators treat with more leniency. As a result, banks and other firms that issue commercial paper have had to raise rates a tad to attract buyers.

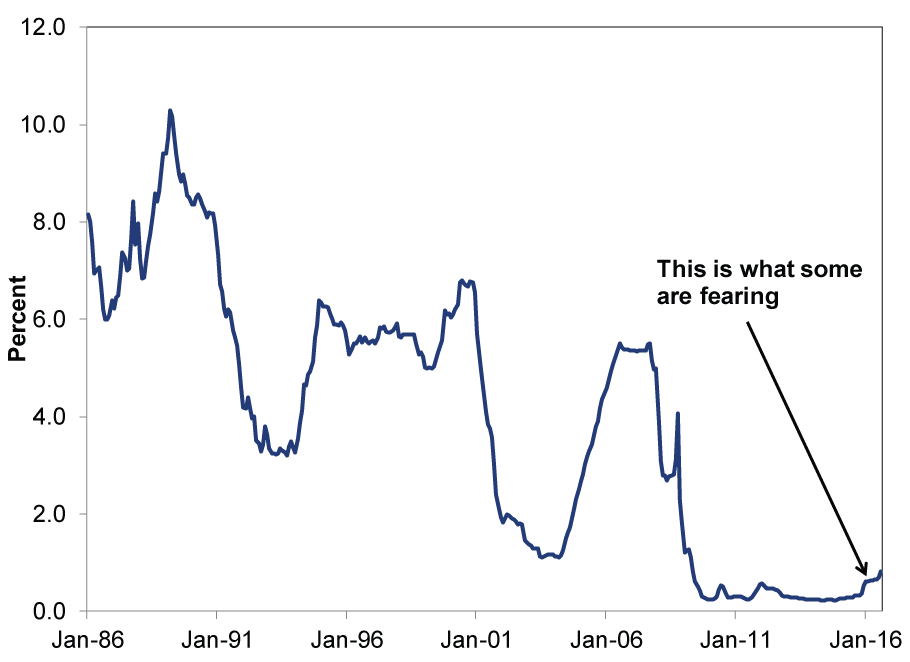

Yet there is a large gap between incrementally higher funding costs due to a structural change in the marketplace and an actual, acute funding squeeze. For one thing, despite the clamor, Libor remains low by historical standards. (Exhibit 1)

Exhibit 1: 3-Month Libor, 1986 - 2016

Source: Federal Reserve Bank of Saint Louis, as of 9/13/2016. 3-Month Libor based on US dollars, January 1986 - August 2016.

Rates were much higher from the mid-1980s through 2007, both during good times and bad. Libor routinely topped 5% in the mid- and late-1990s, when credit was plentiful. Rates rose quite a bit in the few years leading up to 2008's financial crisis, but this is coincidental, not causal, as the crisis had a completely unrelated culprit. Short rates, whether Libor or otherwise, are only one input into credit supply. Long rates matter too, and all banks really need is a sufficient spread between the two.

Jitters about demand for commercial paper are also a bit myopic. For one, they overlook that supply has also plunged-these rules were a long time coming, and firms adapted.

Exhibit 2: Commercial Paper Outstanding

Source: Federal Reserve Bank of Saint Louis, as of 9/13/2016. Commercial paper outstanding, seasonally adjusted, January 2001 - August 2016.

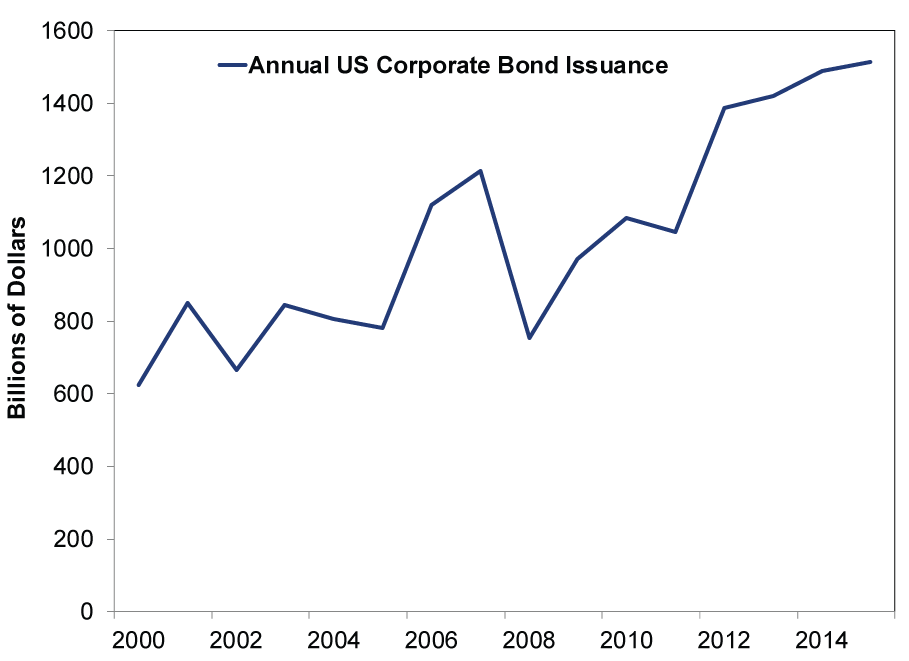

Firms have other ways of funding cash needs, and they've already been doing this in greater numbers since the global financial crisis. For one, they can issue more bonds.

Exhibit 3: Bond Issuance Is Up

Source: Securities Industry and Financial Markets Association, as of 9/13/2016. Total US corporate bond issuance, annually, 2000 - 2015.

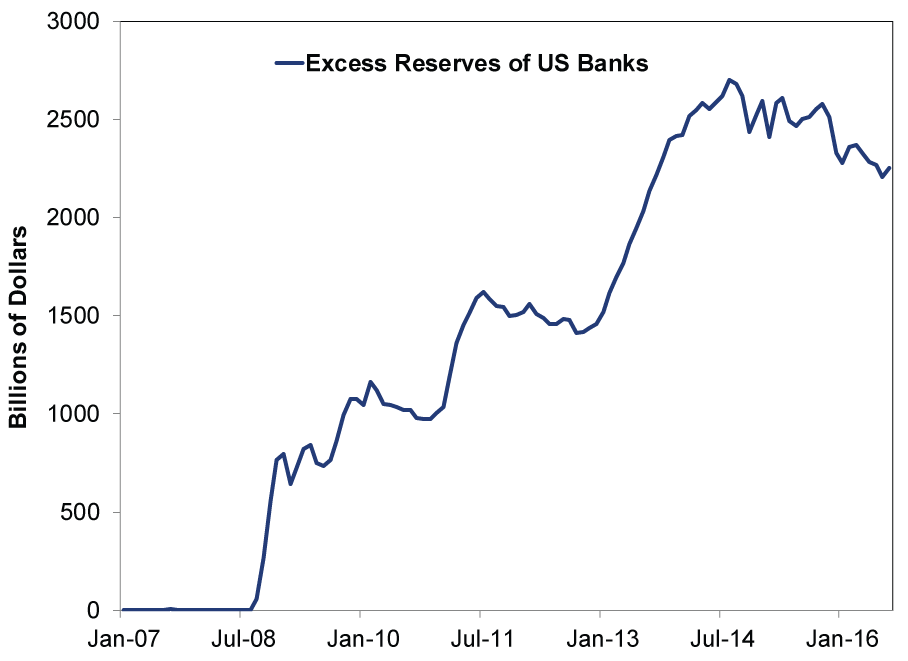

They can also hold more cash, which they've also been doing more of in recent years. According to the Federal Reserve, non-financial corporations held a record $1.9 trillion in cash in 2015. Additionally, since the financial crisis, regulators have nudged banks to rely less on wholesale funding (which includes commercial paper), perceiving traditional deposits as more stable-further limiting supply. Banks have also amassed piles of excess reserves since 2008 as the Fed injected trillions into the banking system. (Exhibit 4).

Exhibit 4: Banks' Excess Reserves Have Risen Dramatically

Source: Federal Reserve Bank of Saint Louis, as of 9/13/2016. Excess reserves of depository institutions in billions of dollars, January 2007 - August 2016.

All that said, there are implications for investors. In advance of the new rules, many fund companies closed prime funds or switched the default cash reserves fund to government money market funds, which have lower yields. It's possible more changes lie ahead, so you may want to check with your broker-dealer to see if your options have changed. Also, investors in institutional prime money market funds-which include many 401(k) participants-will soon see these funds fluctuate in price. At times the price may dip below $1 / share (and at times it might go a wee bit higher). Money market funds should remain a perfectly viable cash-like option-just as they have since that one isolated issue in 2008. People are already aware money markets can go below $1 and haven't stayed away.

[i] The irony here is that the big fund that broke the buck in 2008 was a retail fund, not an institutional fund, and its NAV therefore floated, which is how it broke the buck. And people panicked. So we mostly fail to see how requiring everyone to float would make these securities somehow less prone to a run. But it does level the playing field and add transparency, forcing these funds to own up to the fact that they are all short-term debt funds.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today