Personal Wealth Management / Economics

More on the Fed

Following more QE, it seems to us many in the media are worried about the Fed’s exit strategy when the entry strategy is actually more problematic.

In Thursday’s cover story, we broke down the Fed’s latest add-on to its “exceptionally accommodative” monetary policy, raising a few questions regarding the overall policy direction the US central bank is employing. (Though, at this point, calling the current policy “exceptional” seems like a bit of a stretch.) But the fun doesn’t stop there and, in reviewing media coverage of the announcement, we’re back with more, well, discussion.

For starters, the narrative that seems to be developing is that Fed Chairman Ben Bernanke is the last bulwark to attempt to defang the so-called “Fiscal Cliff.” (We’ll not get into the media’s fiscal cliff follies here, though we invite you to follow this link for a much more in-depth analysis.) But beyond the troubles with the common perceptions of the fiscal cliff, we struggle to see exactly how the Fed’s policies—which, by nature and if successful, would flatten the yield curve—are any sort of a help. It seems a bit illogical to suggest an overstated concern like the fiscal cliff could be mitigated by policy direction that is de facto contractionary.

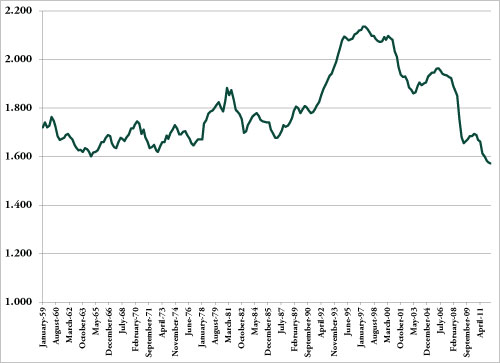

Then again, we’re also looking at an institution that seems committed to boosting lending by reducing the profitability of said lending. And then essentially paying banks to idly park excess reserves they would historically have had to lend to earn a return. The results of such seemingly backwards policy? M2 money velocity—a key metric showing how quickly money changes hands within the economy and a key determinant of inflation—is extraordinarily low.

Exhibit 1: M2 Velocity, Q1 1959 – Q3 2012

Source: Federal Reserve Bank of St. Louis.

Now, another common consideration as it pertains to Fed policy is folks fretting the Fed’s exit strategy. And that is one valid consideration—after all, the Fed has scant history of being effective inflation timers. They could miss it again. But this concern seems very untimely today.

Depressing money velocity in this way is essentially dis- or deflationary policy. Fretting over the exit strategy while the Fed is engaged in deflationary practices seems a bit odd to us. Now, to be sure, there will likely be a time when that’s appropriate. But that just doesn’t seem like an issue in the foreseeable future.

But the broader picture, illustrated today by a surge in industrial production and earlier this week by rising retail sales, is the economy has grown with or without the Fed’s aid. And it seems poised to continue, in our view.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 8 - June 122026-06-15

-

Market Analysis A Market Perspective on Iran Truce Whisperings2026-06-15

-

Expert Commentary This Week in Review | IPOs, US Inflation, ECB Rate Hike

2026-06-12

2026-06-12 -

Market Volatility By the Numbers: 2026’s ‘Volatility’2026-06-12

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today