Personal Wealth Management / Economics

Nine Straight Quarters of Eurozone Growth

Despite rampant fretting, the eurozone has now grown for over two straight years.

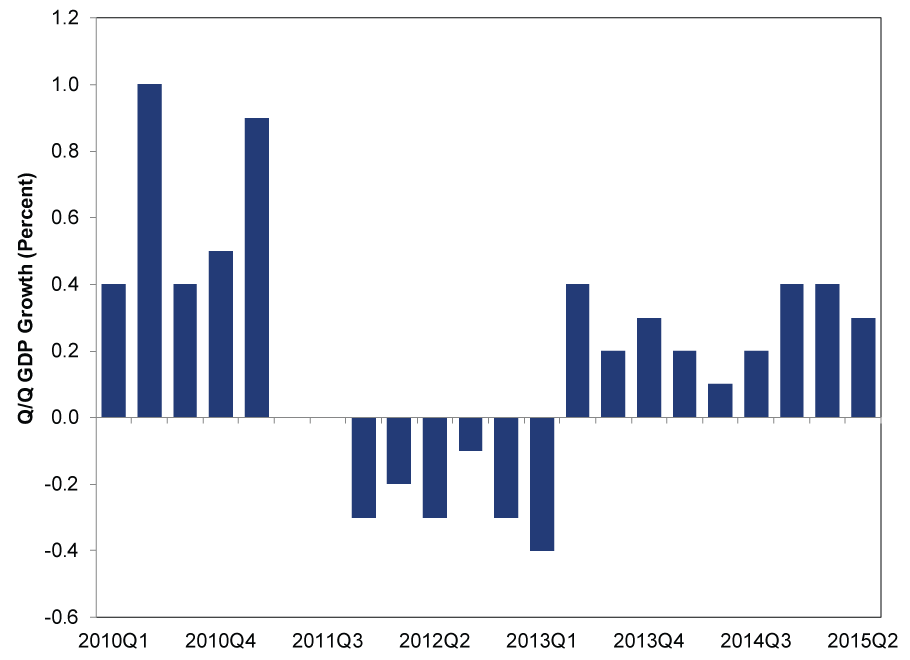

The eurozone grew at a seasonally adjusted rate of 0.3% q/q in Q2-its ninth straight quarter of growth. However, many expressed disappointment since the reading slowed from Q1's 0.4% and missed expectations for a repeat. Some focused on France's flat reading and diverging growth rates as signs of the region's "deep-rooted fragility." In our view, this highlights how skeptical sentiment towards the 19-member bloc remains, suggesting the eurozone's continued uneven, choppy growth likely exceeds low expectations-a bullish scenario.

Despite the dour reaction, the eurozone grew at around the same rate it has over the past two years. (Exhibit 1)

Exhibit 1: Eurozone GDP Growth Since 2010

Source: Eurostat, as of 8/14/2015. Real eurozone GDP (seasonally adjusted), Q1 2010 - Q2 2015.

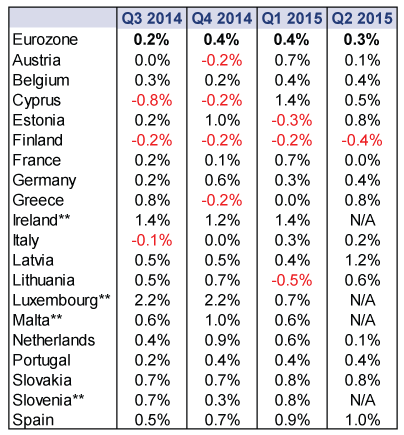

None of the big four economies-Germany, France, Italy and Spain-contracted. Spain led and met expectations of 1.0% q/q, followed by Germany (0.4% q/q) and Italy (0.2% q/q). France trailed with its flat reading, a slowdown from Q1's 0.7% q/q rise and below expectations of 0.2%. German and French exports rose, while Italian exports dragged. On the flipside, while investment and household spending boosted Italian growth, they struggled in France as consumer spending slowed from Q1's 0.9% rise to just 0.1%. Yet nothing in these preliminary data indicates major changes in the eurozone's current economic reality. Uneven as it may be, the region's broad-based recovery remains intact. (Exhibit 2)

Exhibit 2: Eurozone GDP Growth (Q/Q, Seasonally Adjusted)[i]

Source: Eurostat, as of 8/18/2015. **These countries haven't reported Q2 GDP yet.

Other recent data support this, too. June eurozone industrial production continued its choppy streak, falling -0.4% m/m (1.2% y/y) after May's -0.2% m/m (1.6% y/y). While this bumpiness may seem concerning, eurozone growth doesn't depended on heavy industry. Services comprise a larger part of most euro members' economies, and these grew nicely over the past nine quarters. Inflation also remains stable. July's annual inflation rate matched June's 0.2% y/y, while core CPI (excluding energy and unprocessed food) ticked up to 0.9% y/y from June's 0.8% y/y-all in line with a steadily expanding economy, growing money supply and cheap energy.

The media and punditry seem to consistently miss the fact the eurozone is growing and has been growing for some time. They instead focus on backward-looking factors: still-lofty unemployment in the periphery; that GDP is below pre-recession levels; allegedly high debt levels. Yet these tidbits reflect events that already happened-they don't indicate where stocks will head next. However, we think the region's growth should accelerate modestly as credit becomes increasingly available, and forward-looking data support this. The Conference Board's Leading Economic Index (LEI) for the eurozone rose 0.4% m/m in June-its ninth consecutive monthly rise-led by the interest rate spread. Don't buy the negativity rooted in events long in the past. The eurozone's current reality and outlook are brighter than sentiment, and that gap is bullish.

[i] No, that isn't a typo-Greece did grow. However, as we wrote in the "Headlines" section last week for this story: "First, GDP actually contracted in nominal terms-the growth that's grabbing headlines is partly due to deflation adjustments. Second, part of this growth is likely attributable to fear over Grexit pulling forward demand in late Q2, as Greek citizens reacted to the increasing probability capital controls would be installed. We suspect Q3 data, especially early Q3, will be awful. And third, these data are preliminary. But other than those things, yay growth! There is a term for this in investing, and it rhymes with Red Bat Pounce."

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today