Personal Wealth Management / Market Analysis

No Easy Bull, Reprise

There are a lot more toeholds up the Wall of Worry.

It hasn't been easy staying on. (Photo by BradWolfe/iStock.)

Days ago, this bull market turned eight. Now history's second-longest-trailing only the 1990s bull market-many investors wonder just how long the party can last. It's disappointing, but no one can pinpoint exactly when the bull market will end. However, in general, a peak doesn't seem close. It isn't scientific, but in Sir John Templeton's succinct market cycle encapsulation-"Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria"-we're probably somewhere between "grow on skepticism" and "mature on optimism." In our view, the process Templeton described is far from complete, suggesting spreading optimism-and fading fears-could boost stocks significantly before the bull peaks in euphoria.

While uncertainty has fallen over last year's major fears, Brexit and the US presidential election, there is still some residual pessimism over policy implementation (or lack thereof). On the docket: Affordable Care Act (potential) repeal and replacement, tax reform, trade renegotiations, infrastructure spending, revising Dodd-Frank financial reform, debt ceiling debates and Fed appointments. Those lingering fears pale in comparison to last year, showing warming sentiment, but some uncertainty lingers-particularly across the pond. Fears remain over European elections, the potential for trade wars and general skittishness about President Trump's unpredictability. The list goes on.[i]

Outside the political circus, some worry about Fed monetary tightening and inflation (whether too much or too little). Many pundits also trumpet lofty valuations, arguing these set stocks up for a fall. Yet for all the attention these fears garner, the likelihood they upset the bull is way overrated.

Anatomy of a Bull

Fears are ever present, but widely known fears are unlikely to impact markets. Instead, they dampen sentiment and reduce expectations-lowering the bar reality must clear to positively surprise. This is why bull markets are said to climb a wall of worry.

Bulls die one of two ways. Sometimes, they're walloped by a widely unseen negative carrying trillions worth of economic impact-FAS 157[ii] and the US government's bizarre actions in response to the panic in 2008 and the Fed massively increasing reserve requirements for banks in 1937 are two examples. We don't see a similar wallop lurking presently, but watch constantly. More likely, this bull dies as Templeton explained-in euphoria, as most do. However, wanton disregard for risk is hardly evident at the moment.

Sentiment is warming, but this isn't euphoria. To see true euphoria, think back to the late 1990s when anything dot-com-related could go public (and subsequently soar in the secondary market), echoing the early 1980s Energy sector bubble. Or, consider the early 1970's "Nifty Fifty" craze, when shares of 50 American firms were dubbed "one-decision" stocks. The "one decision" was: buy. Growth at any price! Disregard for economic fundamentals that characterize market peaks-inverted yield curves and other forward-looking indicators showing weakness-went hand-in-hand with those euphoric stretches.

Today, not only is euphoria missing, but forward indicators are positive and yield curves adequately steep. Overly aggressive Fed moves to rein in rampant inflation or "animal spirits" could be years away. Headlines shriek of high valuation measures-even broken ones like the CAPE. The time to worry is when the getting's so good that a "new paradigm" rationalizes any valuation, and most everyone believes it. While investors aren't as skeptically skittish as they have been in recent years, they aren't obliviously throwing caution to the wind. As time goes on, they should get there. But they need to see more false fears sunset first.

Fears of Losing Outweigh Fears of Losing Out

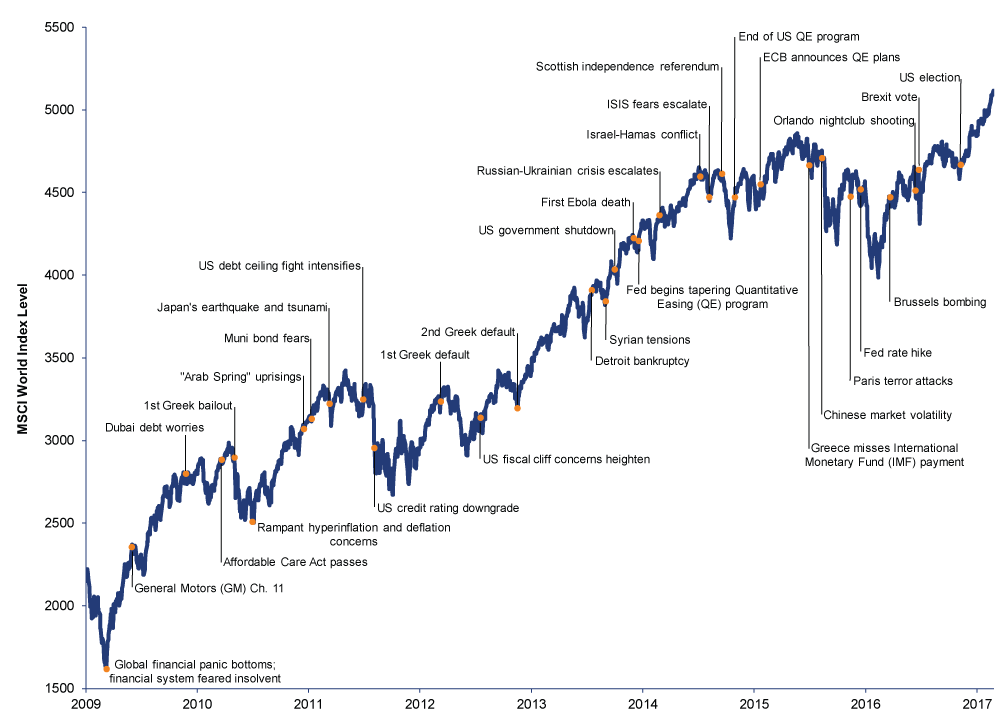

Exhibit 1 shows fears the bull market has weathered so far this cycle, spooking investors around every corner. It hasn't been an easy journey; every step felt like walking through a veritable minefield. But all those fears proved to be toeholds in climbing the wall of worry. The hard part for investors is scaling them. If you did, you've been rewarded in spades.

Exhibit 1: Look Back at the Wall of Worry and Rejoice!

Source: FactSet, as of 2/27/17. MSCI World returns with net dividends, 12/31/2008 - 2/24/2017.

Markets tend to evolve in cycles because humans shun regret. Prospect Theory shows folks hate losing-in fact, two and a half times more than they enjoy winning on average. All along the Wall of Worry from 2009, many investors were so afraid of losing-traumatized by the financial panic-they sat out a historic bull market. Now after eight years, markets have dispelled many of the fears media trumpeted, gradually causing skepticism to shift from stocks to the pundits themselves.

But humans are naturally risk averse, so it takes a lot of time and evidence to cause the masses to overcome their worries. Only then does fear of losing out take over. It's when herding kicks in-the fear of getting left behind-that the bull stampede starts. The media develops (or trots out pundits offering) ad hoc rationalizations about why the bull is unstoppable,[iii] which are just as absurd as the permabears, but in the opposite direction.

When everyone's bullish with nary a care, there are no more skeptics to flip. No more newly bullish converts. No more desire to bid up stocks. Sitting atop a Wall of Worry is precarious. But until then, there is room aplenty for optimism to mature, which is historically when markets have seen some of their best returns.

[i] Geopolitical conflicts, natural disasters, humanitarian catastrophes, pandemics, etc.

[ii] Forcing write downs and fire sales by requiring mark-to-market accounting and needlessly vaporizing trillions from perfectly sound assets.

[iii] Like Dow 36,000.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today