Personal Wealth Management / Economics

Now Hiring: Reasons to Be Optimistic

The media seemed ecstatic about November's jobs report, but investors have better reasons to be optimistic about the US economy's prospects.

All eyeballs seemed glued on the US Bureau of Labor Statistics (BLS) last Friday, eagerly awaiting the November US Employment Situation Report, more commonly known as "The Unemployment Report." Financial media had countdown clocks ticking away the seconds to 8:30 a.m. (EST), when the data are publicly released. TV networks had a guessing game of folks staking out numbers, with most basing their guesses loosely on the consensus estimate that nonfarm payrolls would rise by 230,000 new jobs. But when the number hit, it blew them all away: 321,000 new jobs in November , the record 50th straight month of growth . The unemployment rate held steady at its postwar average, 5.8%. Media reaction was uncharacteristically sunny: The recovery is finally hitting home! Growth is finally showing up in the "real economy," a newfangled ray of sunshine for Main Street. And hey, it is positive news! But the cheery reaction seems to treat the good news as if it's, well, new. Yet these late-lagging data points merely confirm what we've long suggested: The US economy is far stronger than most folks appreciate. For investors, basing a rosier outlook on lagging indicators like job growth isn't so sensible, but more forward-looking and coincident data suggest a positive outlook is justified either way.

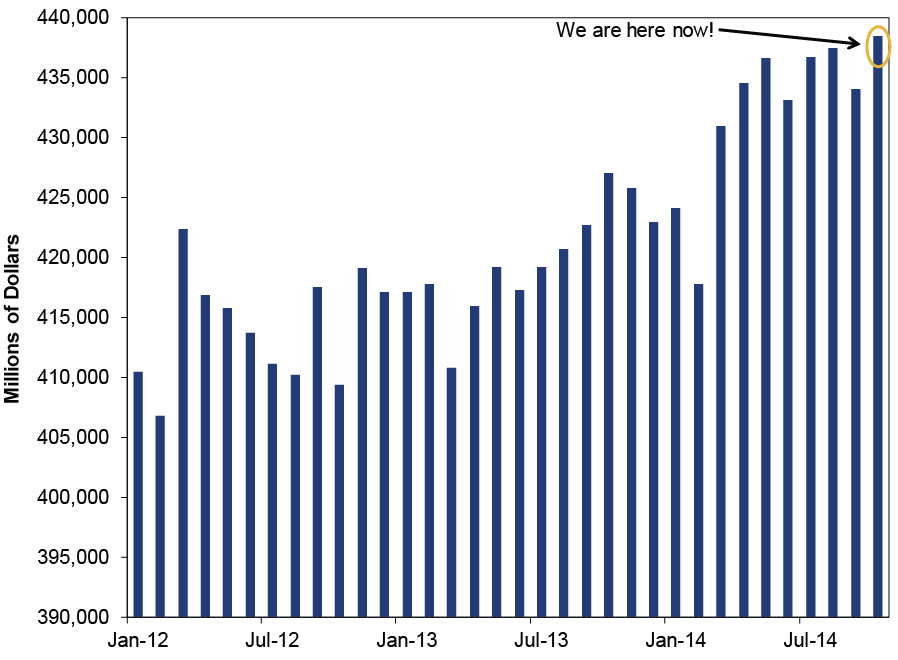

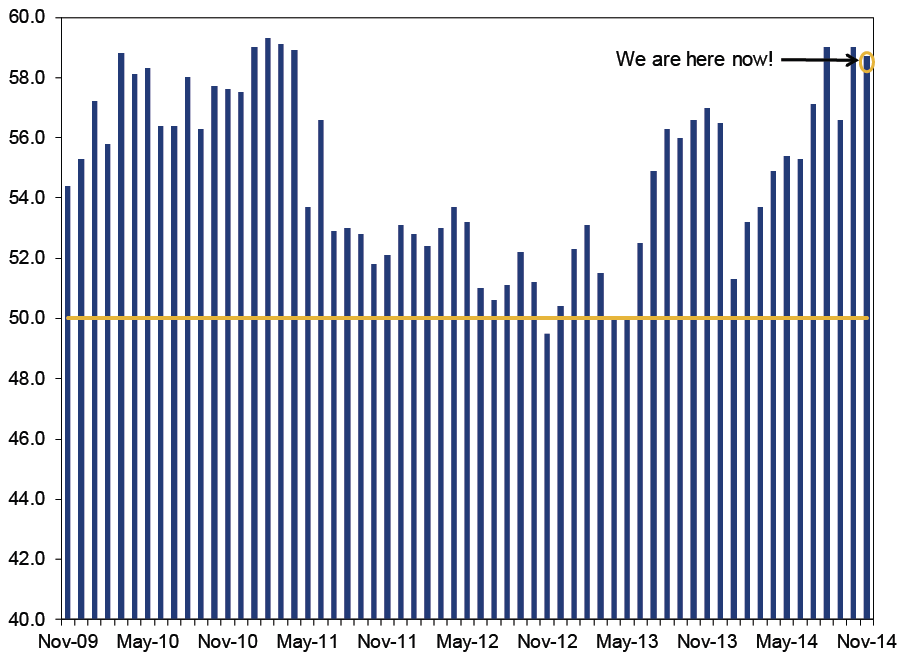

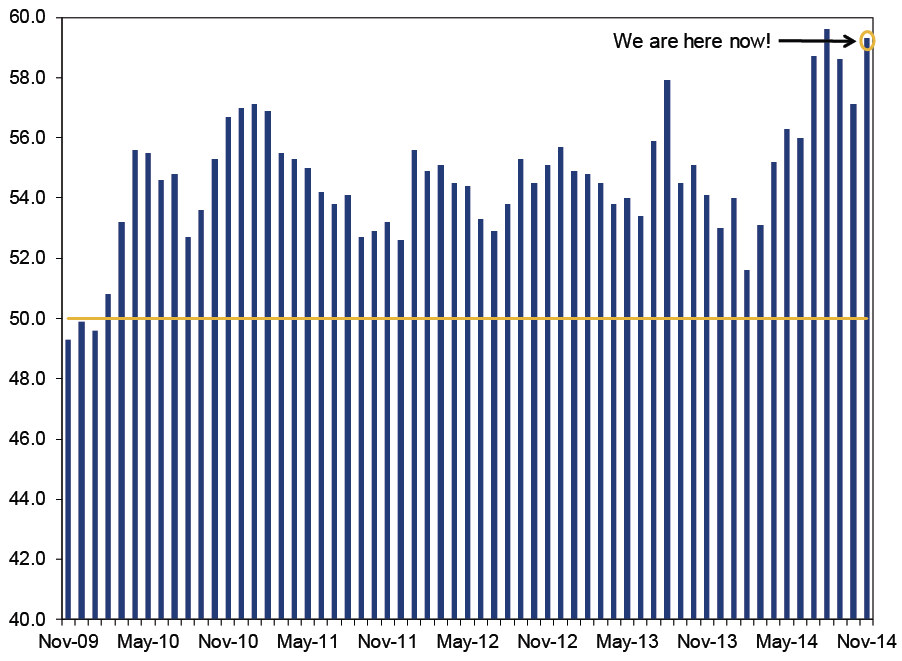

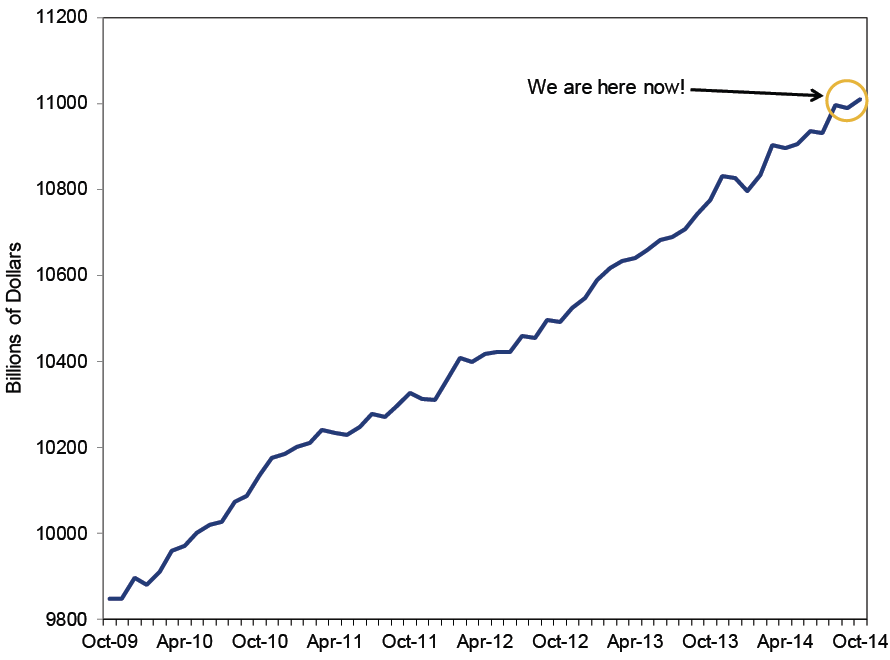

As we've said before, employment tends to lag broader economic growth -in some cases by many months . It can be dangerous for investors to track the labor market closely. Stocks look forward, and if your outlook hinges on lagging indicators, you could miss cyclical changes. But beyond the jobs report, other recent data support the notion the US is growing nicely. See both exports and imports rising (1.2% m/m and 0.9% m/m, respectively) in October. Headlines cheered a falling trade deficit (something that isn't a threat), but we'd suggest the real applause should be for rising total trade (exports plus imports). Rising total trade shows healthy demand for our exports abroad, and healthy demand in general at home. Elsewhere, the Institute for Supply Management's (ISM) November purchasing managers' indexes (PMI) for manufacturing and services showed continued expansion. Manufacturing hit 58.7, a bit lower from October's 59 reading but still well above 50[i]. Services rose to 59.3, above the prior month's level of 57.1. October consumer spending ticked up 0.2% m/m, extending its long-term rise. And none of this is new, as Exhibits 1 through 5 show.

Exhibit 1: US Total Trade

Source: Bureau of Economic Analysis. From January 2012 - October 2014.

Exhibit 2: ISM Manufacturing

Source: St. Louis Fed. From 11/1/2009 - 11/1/2014. 50 denotes the dividing line at which more or less than half of survey respondents reported growth.

Exhibit 3: ISM Services

Source: St. Louis Fed. From 11/1/2009 - 11/1/2014. 50 denotes the dividing line at which more or less than half of survey respondents reported growth.

Exhibit 4: Real Personal Consumption Expenditures

Source: St. Louis Fed. In billions of chained 2009 dollars. From 10/1/2009 - 10/1/2014.

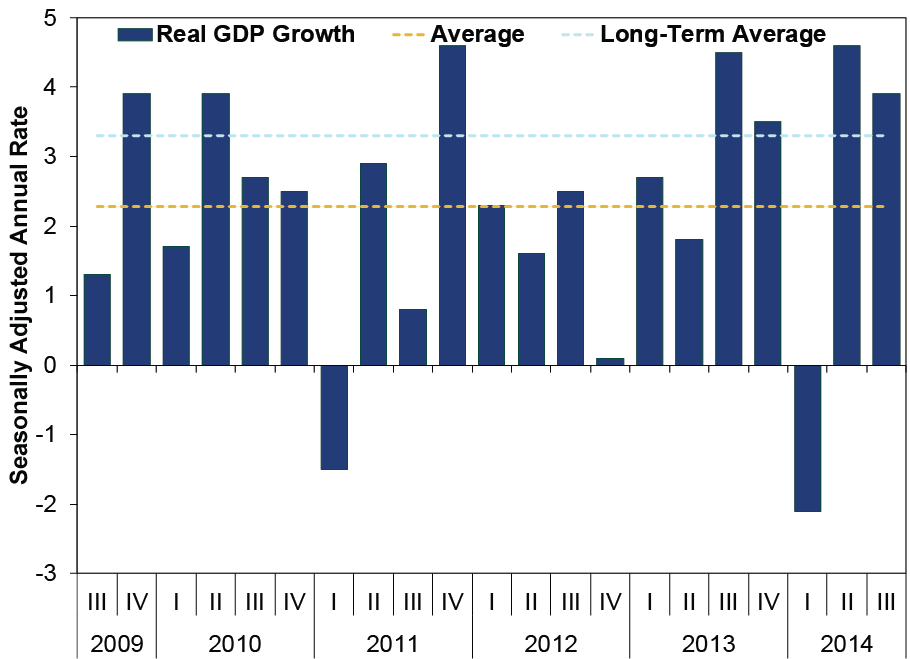

Exhibit 5: US GDP Growth

Source: US Bureau of Economic Analysis, as of 11/26/2014. US real GDP growth Q3 2009 - Q3 2014. Long-term average, Q2 1947 - Q3 2014.

Recent US economic strength isn't an anomaly. It isn't new. It isn't a sudden shift. The US economy hasbeen strong for a while. Folks turning optimistic now are late to this party.

But they aren't so late as to be irrationally optimistic. Forward-looking economic indicators suggest the expansion will continue looking ahead. Consider: The Conference Board's Leading Economic Index (LEI) rose 0.9% in October-the eighth rise in the past 10 months. In its 50-plus-year history, no US recession started while LEI was rising. The ISM Services New Orders index (Exhibit 6) also showed expansion throughout the year. Unlike the Manufacturing New Orders Index, the Services New Orders Index isn't included in LEI. Combining the largest segment of the US economy with LEI is powerful evidence of future growth.

Exhibit 6: 2014 ISM Services New Orders Index

Source: St. Louis Fed. 50 denotes the dividing line at which more or less than half of survey respondents reported growth.

Corporate America in particular looks healthy and able to continue powering the expansion too. After falling in Q4 2013 and Q1 2014, after-tax corporate profits rebounded to set two consecutive all-time highs in Q2 and Q3 2014. This replenishes US companies' cash-money for future investment driving growth. With roughly $1.9 trillion in cash on nonfinancial corporate balance sheets , the US private sector has ample fuel to invest in expansionary endeavors like R&D, equipment, buildings, new technology upgrades, M&A and jobs.

In our view, the punditry's newfound optimism is pointing in the correct direction, even if the proximate cause for the more cheery outlook (jobs) is somewhat off base. But with other data showing it isn't irrational to feel good about the US economy's prospects now and in the near future, investors have plenty of reasons to smile.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i]PMIs are surveys, and 50 is the point at which more or less than half of respondents reported growth in a month.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today