Personal Wealth Management / Market Analysis

Oil Well Supplied

Vaunted oil cartel production cuts have failed to stem global supply, keeping a lid on prices and Energy sector performance.

OPEC's production cuts haven't led to big output drops. (Photo by ahopueo/iStock.)

Last November, the media made much of the deal struck between the Organization of Petroleum Exporting Countries (OPEC) and several non-OPEC oil-exporting nations to cut production in 2017. After two years of huge output, the deal sought to ease the supply glut that crushed oil prices and Energy sector profits. Investors greeted the deal with optimism, presuming cuts would fuel further oil price gains-and bolster Energy firms' profits. However, thus far, enforcement has been lax and compliance spotty, particularly among non-OPEC producers. Meanwhile, US crude oil exports have surged, inventories are at record levels and, after a brief dip, production is rising anew. Globally, oil remains well supplied, likely keeping prices low and limiting Energy sector relative performance.

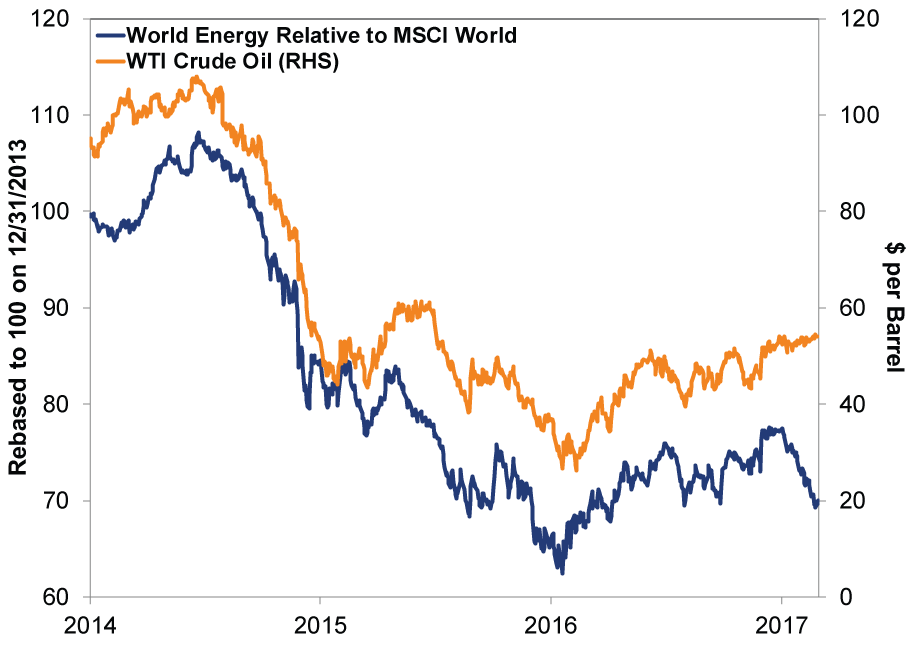

After falling fast from June 2014 through February 2016, crude oil prices rallied from a low of $26 per barrel to $51 by June.[i] This rebound coincided with Energy sector outperformance, which got many thinking the bottom was in and Energy stocks would continue surging. However, gains since then haven't impressed. Oil has mostly traded in a $50 to $55 per barrel range since December, and Energy stocks lagged bigtime. (Exhibit 1) Which isn't surprising to us. Energy stocks are highly oil-price sensitive, so continued outperformance would probably need one of two scenarios: Either oil prices rise with staying power, perhaps driven by major production cuts, or sentiment toward oil firms falls a lot-overshooting the outlook for oil production. With OPEC and non-OPEC nations cheating on quotas and the US happy to take market share, production isn't likely to fall. And it seems investors still haven't soured enough on the industry, given high Energy sector valuations and frequent media chatter.

Exhibit 1: Energy Sector Relative Performance vs. Crude Oil

Source: FactSet and Federal Reserve Bank of St. Louis, as of 3/2/2017. MSCI World Energy Index and MSCI World Index returns with net dividends, 12/31/2013 - 3/1/2017. WTI crude oil prices, 12/31/2013 - 3/1/2017.

OPEC Discipline Eroding

OPEC has achieved 90% compliance to reduce output by their 1.2 million barrels per day (bpd) goal, almost entirely from Saudi Arabia's efforts. That's pretty good by OPEC's historical standards, but the agreement only runs through June. Meanwhile, Libya, Nigeria and Iran, although OPEC members, were exempt from the deal-allowed to increase production-and have done their best to take advantage. Libya is set to raise production to 900,000 bpd from 200,000 last year. Nigeria's production fell to 1.1 million bpd in August last year, but January figures showed a rebound to 1.6 million bpd. Iran was averaging around 3.6 million bpd last year, but is now pumping 4 million bpd. All told, exempted OPEC nations have taken a bite out of the deal's cuts.

Compliance among the 11 non-OPEC countries, which agreed to cut by 600,000 bpd, has been woeful. Russia has cut production by only one-third of its pledged 300,000 bpd. Others, like Mexico and Azerbaijan, promised to cut, but the words rang hollow-production fell by what was already expected. Should compliance continue breaking down, any effort at discipline in the second half of 2017 after the current agreement expires will be that much more difficult to maintain. Everyone got together for some nice group photos and cheery words promising solidarity on Tuesday, but history suggests this talk is exceptionally cheap.

US Production Ramping Up

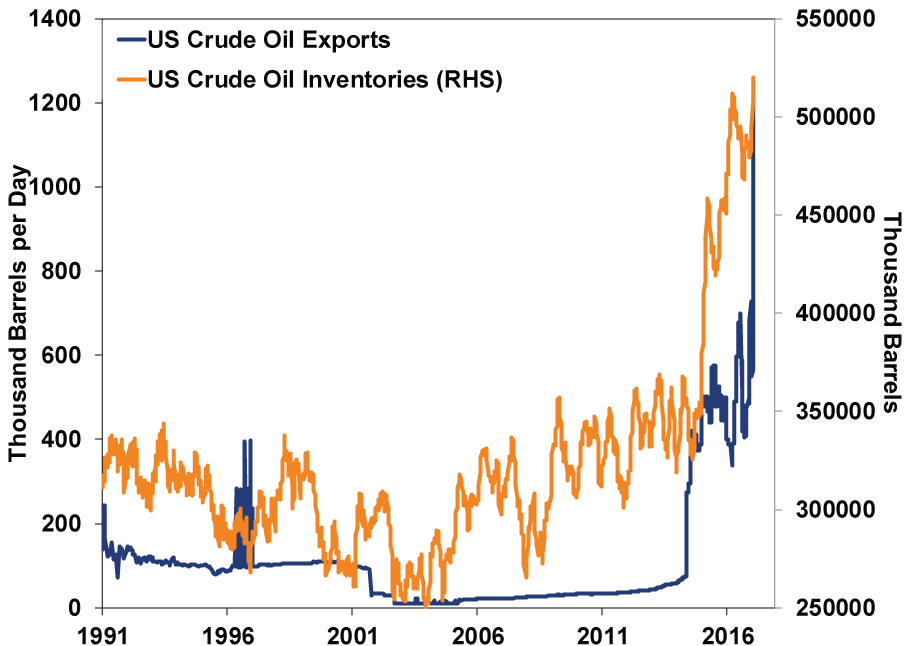

Thanks to advances in shale drilling technology, US crude oil production is back near levels last seen during the late-1960s' and early-1970s' oil embargos, but with a fraction of the rigs. While OPEC's 2014 move to maintain production certainly impacted America's output and drilling activity, the effect wasn't huge and looks fleeting. After all, OPEC (and non-OPEC) intended to drain an inventory glut. Yet US crude oil inventories last week reached record levels at 520 million barrels, up from 350 million two years ago. And it's not being kept off the market: US crude oil exports have doubled in the past few months to a record 1.2 million bpd, offsetting a large share of OPEC's cuts. (Exhibit 2)

Exhibit 2: Record US Crude Oil Exports and Inventories

Source: US Energy Information Administration, as of 3/6/2017. Weekly US Exports of Crude Oil (Thousand Barrels per Day) and Weekly US Ending Stocks excluding Strategic Petroleum Reserves of Crude Oil (Thousand Barrels), 2/8/1991 - 2/24/2017.

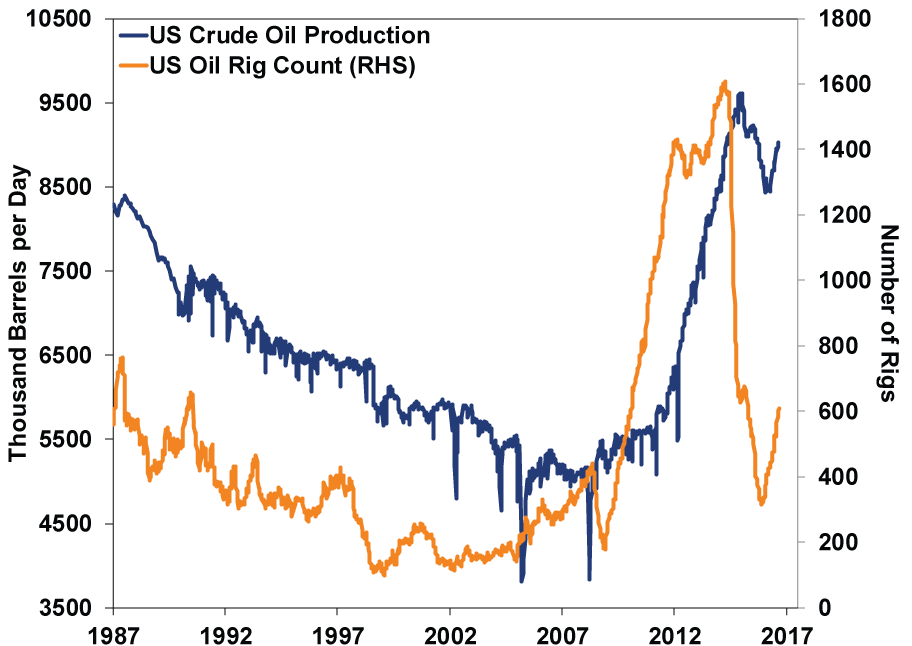

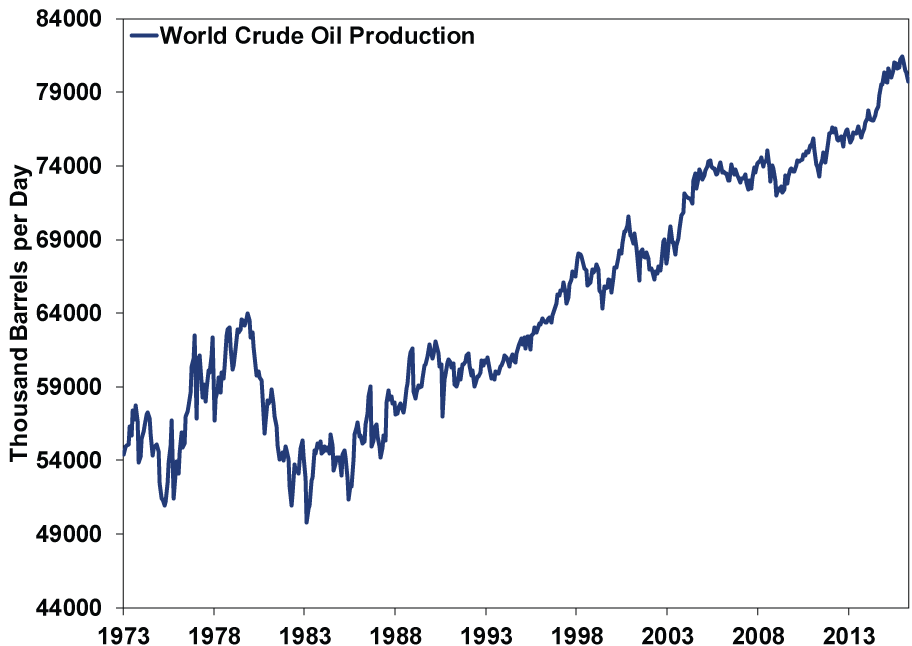

The more oil export-dependent nations try to comply with self-imposed quotas, the more market share US producers should take. With shale breakeven production costs falling, firms can profitably ramp up production even at today's prices. They have already begun boosting output, and rising US drilling activity suggests more lies ahead. (Exhibit 3 shows US oil production and Baker Hughes' tally of actively drilling rigs in the US.) Global oil production has been making new highs since 2010 and the US Energy Information Administration forecasts it hitting another record this year, OPEC deal or no. (Exhibit 4) World demand is well supplied, arguing against higher oil prices, which likely weighs on Energy performance.

Exhibit 3: Baker Hughes' Rig Count and US Oil Production Are Rebounding

Source: US Energy Information Administration and Baker Hughes' North America Rig Count, as of 3/7/2017. Weekly US Field Production of Crude Oil (Thousand Barrels per Day), 7/17/1987 - 2/24/2017, and Weekly US Oil Rig Count, 7/17/1987 - 3/3/2017.

Exhibit 4: World Oil Production

Source: US Energy Information Administration, as of 3/6/2017. Monthly World Crude Oil Production, thousand barrels per day, 1/31/1973 - 11/30/2016.

[i] Source: Federal Reserve Bank of St. Louis, as of 3/8/2017. WTI crude oil prices, 6/20/2014 - 6/8/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Crypto, Inflation, Annuities and More - June 20262026-06-30

-

Market Analysis Investors Are (Still) Fighting the Last War on Inflation2026-06-30

-

Market Analysis Reader Mailbag: June 20262026-06-30

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-06-29

2026-06-29

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today