Personal Wealth Management / Politics

On President Trump’s ‘Terrible Day’ and Impeachment Rumblings

Time will tell what this week’s events mean for impeachment, but whatever happens, history shows an actual impeachment needn’t be bearish.

Editors’ Note: Our political commentary is intentionally non-partisan and analyzes political developments solely for their potential economic and stock market impact. We favor no politician or party and believe political bias is an investing error.

For those who have been hiking in the wilderness or hiding under a rock this week, one former Trump associate was convicted on fraud charges Tuesday, while another pled guilty to charges of illegal campaign financing and subsequently implicated President Trump in illegal behavior. We have zero desire to wade into this salacious pool of hush money and clandestine encounters that read like a Black Mirror version of the dalliances of Clark Gable and Carole Lombard, but headlines are treating these events as a crucial turning point in the investigation into 2016’s election—potentially increasing the odds of a Trump impeachment. We have no way to know whether this is true, as we aren’t legal experts and don’t have inside information on the investigation—and neither do most of the pundits pontificating about this across the Internet. Basing portfolio decisions on speculation and hearsay is always an error, in our view. So, as we all wait and see how this shakes out, we think investors should keep some key things in mind. One, if President Trump is impeached, this doesn’t necessarily mean he would be removed from office. Two, while the history of impeachments and market returns is limited, there is no evidence impeachment is inherently negative for stocks.

Without knowing what facts will eventually emerge, it is impossible to know the scope of yesterday’s events. Whether the House votes to impeach Trump likely depends on whether Democrats take the chamber in November’s midterms. As our founder and Executive Chairman, Ken Fisher, wrote in USA Today this week, they must gain 23 seats to win, and only about 36 seats are truly toss-ups. They could take a small majority, or they could come up a bit short.

While the House can vote to impeach, the Senate is the jury in the subsequent trial. Conviction requires a two-thirds majority vote. Because the Republicans must defend fewer Senate seats in traditionally Democratic states than Democrats must defend in Republican states, we think they could gain one or two seats, preserving their small majority and likely making conviction difficult. Even if the Democrats gain a small edge instead, getting two-thirds of Senators to convict would be a tall order based on the information and facts known today. Perhaps this changes if more evidence emerges. But bear in mind, a Republican Senate voted to keep President Clinton in office after his 1998 impeachment. The barrier for removal is quite high.

If Trump were removed, it would be a media circus. But when it comes to politics, over any meaningful length of time, stocks ultimately move on policies, not personalities. On this front, we see little likelihood of sweeping change. His replacement would be Vice President Mike Pence, also a Republican. He would likely have either a split Congress, small Republican majority or small Democratic majority. All yield gridlock, keeping the risk of sweeping legislation low.

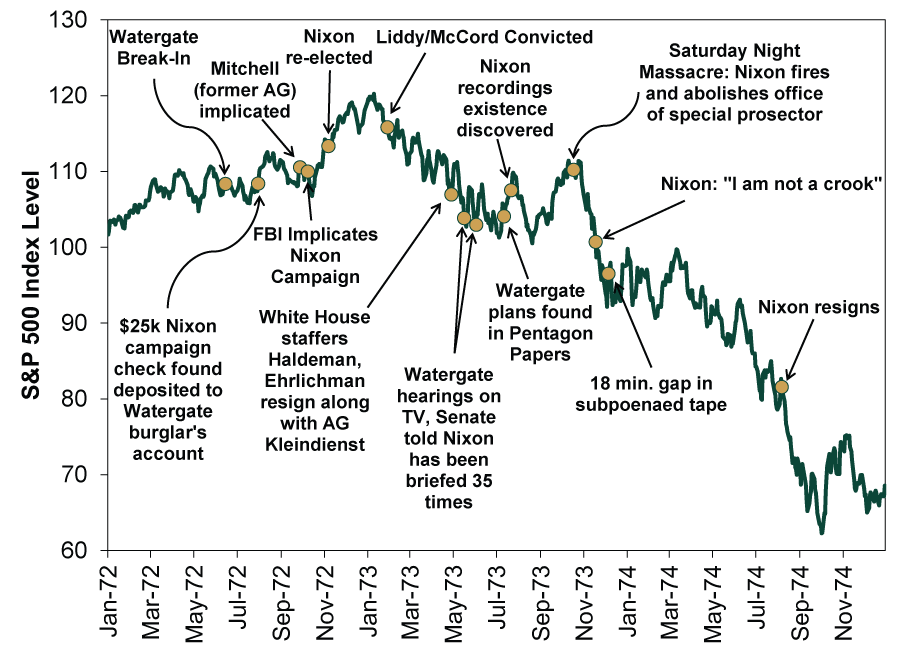

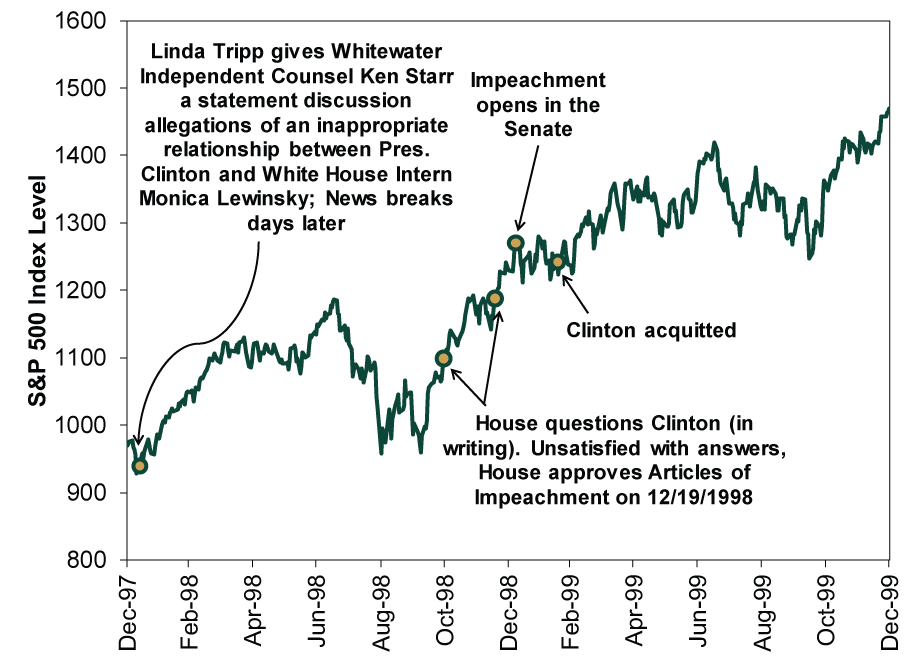

Plus, despite common media presumptions, impeachment isn’t inherently bearish. We have two historical data points to study: Presidents Clinton and Nixon. Though Nixon resigned before impeachment was initiated, markets had plenty of impeachment chatter to price in throughout two years of Watergate investigations. As Exhibit 1 shows, US stocks rose through the early months, even after the FBI implicated the Nixon campaign, before peaking in early 1973. That era’s political events loom large in history, but it is important to remember markets were also dealing with a host of economic issues, including the aftermath of Nixon’s price controls and the oil shock. The bear market began long before Nixon’s tapes and Pentagon Papers surfaced. It escalated after the Saturday Night Massacre, making it fair to say the uncertainty exacerbated the downturn, but it wasn’t the sole culprit. However, stocks seemed not to mind Clinton’s impeachment at all. As Exhibit 2 shows, the moment the scandal broke through Clinton’s 2/12/1999 acquittal, the S&P 500 price index gained 28%.[i] 1998’s correction occurred during this stretch but was tied to the Russian Ruble Crisis and Asian Financial Crisis, not the Lewinsky affair.

Exhibit 1: S&P 500 During the Watergate Scandal

Source: Global Financial Data, Inc., as of 5/10/2017. Daily S&P 500 Price Index, 1/3/1972 – 12/31/1974.

Exhibit 2: S&P 500 During the Lewinsky Scandal

Source: Global Financial Data, Inc., as of 5/10/2017. Daily S&P 500 Price Index, 12/31/1997 – 12/31/1998.

Moreover, most pundits presuming a Trump impeachment would be bad for stocks seem to operate on the assumption Trump administration policy was uniformly bullish and behind stocks’ rise. That was a common (and incorrect, in our view) argument last year. Yet this year pundits have spilled trillions of pixels arguing his trade policy and tariffs are dangerous, geopolitical approach unsettling and more. To us, that is all overstated. But the logical disconnect is worth noting.

An impeachment trial—or a prolonged will-they-or-won’t-they—could raise uncertainty, which could in turn impact investor sentiment and short-term returns. But this is only one possibility, and as always, short-term volatility is impossible to predict. Moreover, it is highly unlikely elevated uncertainty alone would cause a bear market. An actual change in fundamental conditions—large enough to cause a recession in an $80 trillion-plus global economy—is typically necessary to cause a bear market. The US is only 60% of developed world global market cap, and it is difficult to see how heightened political uncertainty here would cause severe economic problems in, say, Germany. More likely, US political theatrics are just another brick in this bull market’s proverbial wall of worry.

[i] Source: Global Financial Data, Inc., as of 5/10/2017. S&P 500 price return, 1/12/1998 – 2/12/1999.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-07-07

2026-07-07 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 29 - July 32026-07-07

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today