Personal Wealth Management / Market Analysis

Opinions Make Poor Standards

S&P thinks the US economy is doing fine, but we didn’t need an outlook upgrade to tell us that.

Credit ratings agencies have plenty of opinions and often change them—but their opinions rarely result in actual lasting market impact. So when S&P upgraded its US outlook on Monday, we thought the market’s yawn was pretty appropriate. Markets move on surprises. Yet S&P’s cited reasons behind its outlook upgrade (note, not rating upgrade) have been widely known by markets for a while. The US economy has expanded—sometimes faster, sometimes slower—since S&P’s 2011 downgrade, and stocks are much higher, too. That S&P’s just now responding illustrates how it (along with other credit ratings agencies) watches the rear-view mirror and overemphasizes politics when assessing economic health.

S&P’s previous US downgrade is a terrific example of this. In August 2011, S&P downgraded the US’s credit rating, from AAA to AA+, concerned US politicians couldn’t agree on a satisfactory debt solution. (Our view is America’s debt situation remains manageable—for more go here, here, here and here.) At the time, the debt ceiling debate was in full swing, and S&P seemed to think US partisan politicking—a very, very common occurrence with most often no economic impact—could derail the US economy. However, when Congress did finally agree and passed the Budget Control Act, S&P downgraded the US anyway—a rather retroactive response, in our view.

There was widespread concern, trumpeted throughout media, that the downgrade signaled big trouble ahead. Further, pundits and politicians alike threatened the downgrade would mean much higher debt yields as investors demanded higher rates to lend money to a less fiscally responsible US.

Yet the opposite actually occurred. Very shortly after the downgrade, interest rates fell on 10-year Treasurys and stayed exceptionally low for some time. Stocks climbed higher, too! The S&P 500 index now prettily sits above its 1600 mark, whereas it was under 1200 in August 2011. Bond yields have bounced around a fair bit—staying near historic lows for some time, and now are in the 2.2%-2.3% range—RIGHT where they were before the downgrade. Not what you’d expect if the market truly feared the US wasn’t fiscally sound.

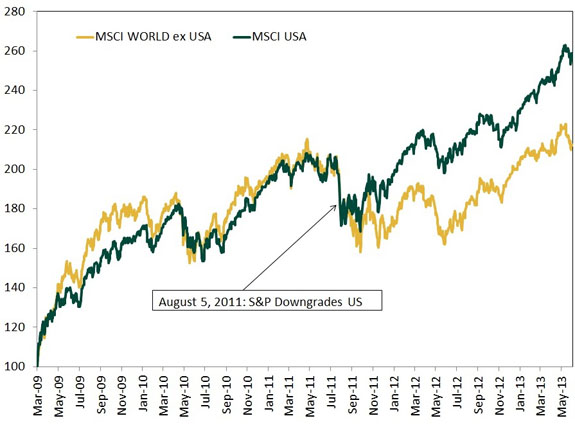

So it seems the US economy wasn’t in the dire straits many—thanks to S&P—feared. In fact, looking at the MSCI USA Index, a broader measurement of US stocks than the S&P 500, you’ll see those investing in US stocks since August 2011 would have seen some material gains. In fact, US stocks largely outpaced global stocks starting about when the downgrade occurred—for the initial stage of the bull market non-US stocks had led. Again—this isn’t what you’d expect if the market were truly concerned about the US.

Exhibit 1: US Stocks Outperform

Source: MSCI Inc., as of 06/12/2013. Graph shows MSCI USA Index and MSCI World ex-USA Index returns, indexed to 100, from 3/9/2009 to 6/11/2013.

Investors taking S&P’s advice would have missed out. Hence, we generally warn against taking credit ratings agencies’ opinions as anything other than that—an opinion. One to be weighed against other factors and analyzed to see if it’s mostly backward- or forward-looking.

And the 2011 US downgrade is just one example (of afairfew) of a credit ratings agency reacting mostly to past political fodder. And most of the time, despite whatever near-term reaction they provoke, credit ratings agencies’ opinions rarely (if ever) become longer-term market movers. More often, they confirm what most folks already know: Greece was downgraded after everyone knew it was a disaster and bond yields had already fallen. And the US was downgraded in large part because politicians couldn’t agree—something that’s been true since the dawn of modern society. And now, it seems S&P is jumping on board with overall improving sentiment on the US. Pretty much par for the course.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Pump Won’t Hurt the Global Economy2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today