Personal Wealth Management / Economics

Overseas Expansions Can Weather a Blip

Worries about weakening eurozone and UK economic growth seem overwrought, in our view.

April showers bring May flowers, but May’s economic data releases haven’t brought folks much joy. The latest numbers on the eurozone and UK largely show continued expansion, but some folks still have doubts. In their view, the trend is weakening, and the bad weather excuse is losing credibility. Could the global expansion be petering out—and does that spell trouble ahead? In our view, no—rather, the broad overthinking of short-term data volatility suggests sentiment overseas remains skeptical overall.

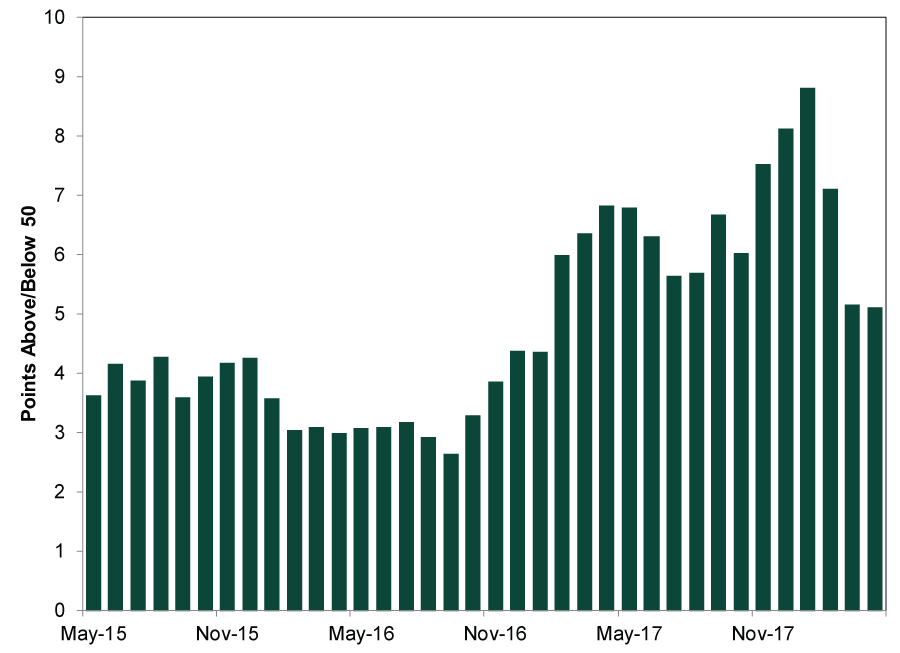

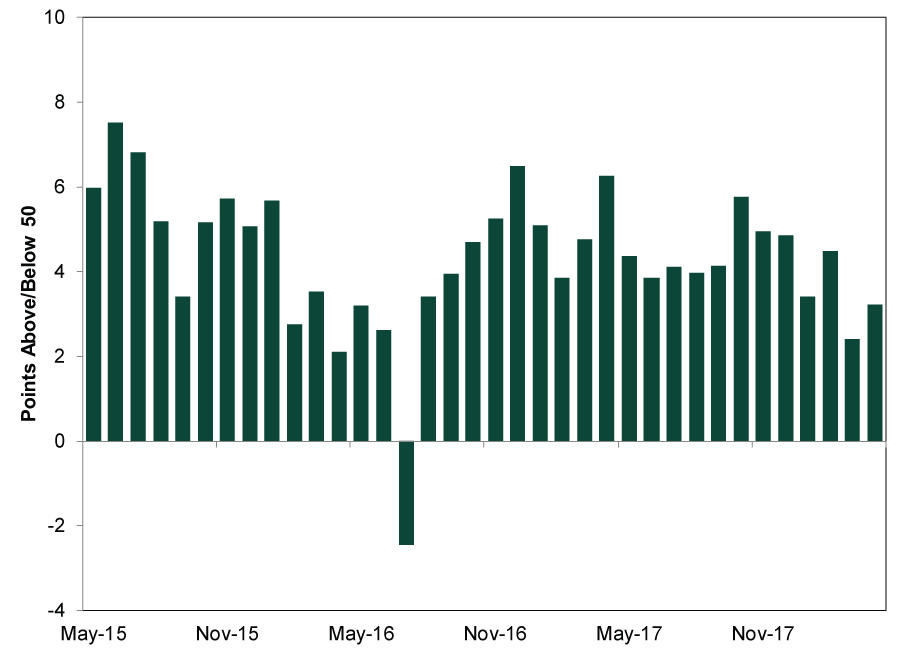

In May’s first week, IHS Markit announced April eurozone composite purchasing managers’ index (PMI) registered 55.1, a tick down from March’s 55.2. Eurozone Services PMI hit 54.7 and Manufacturing delivered 56.2, both also down from March (54.9 and 56.6, respectively). The Markit/CIPS folks said the UK posted similar April figures: Composite PMI rose to 53.2 from March’s 52.4; Services PMI improved to 52.8 from 51.7; and Manufacturing weakened to 53.9 from March’s 54.9. All exceed 50, indicating more surveyed firms reported growth than contraction.

However, the reaction to these growthy reports wasn’t very chipper. One headline noted that despite some bright spots, PMIs show “clouds form over euro zone growth.” As for the UK, the “Beast from the East’s” chill in business activity is wearing off, yet “… the underlying performance of the economy has continued to deteriorate.” This extends the “slowing growth” narrative that started with weak February German data. The underlying concern: After a strong 2017, the expansion across the Atlantic is slowing—allegedly indicating weaker growth (or worse) in the future.

We think this interpretation reads too much into a small sample size. A single report gets oodles of attention, but early 2018 data aren’t huge outliers. Beyond PMIs’ limitations—the surveys indicate only the breadth, not the magnitude, of growth—the eurozone and UK’s April reports aren’t drastically removed from the long-term growthy trend.

Exhibit 1: IHS Markit Eurozone Composite PMI Since May 2015

Source: FactSet, as of 5/8/2018.

Exhibit 2: IHS/CIPS UK Composite PMI Since May 2015

Source: FactSet, as of 5/8/2018.

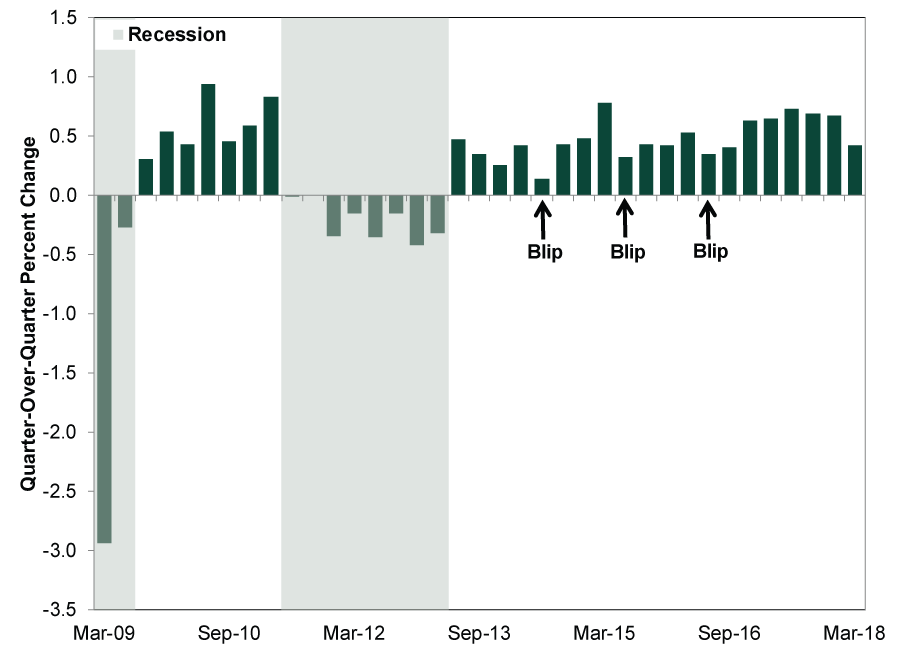

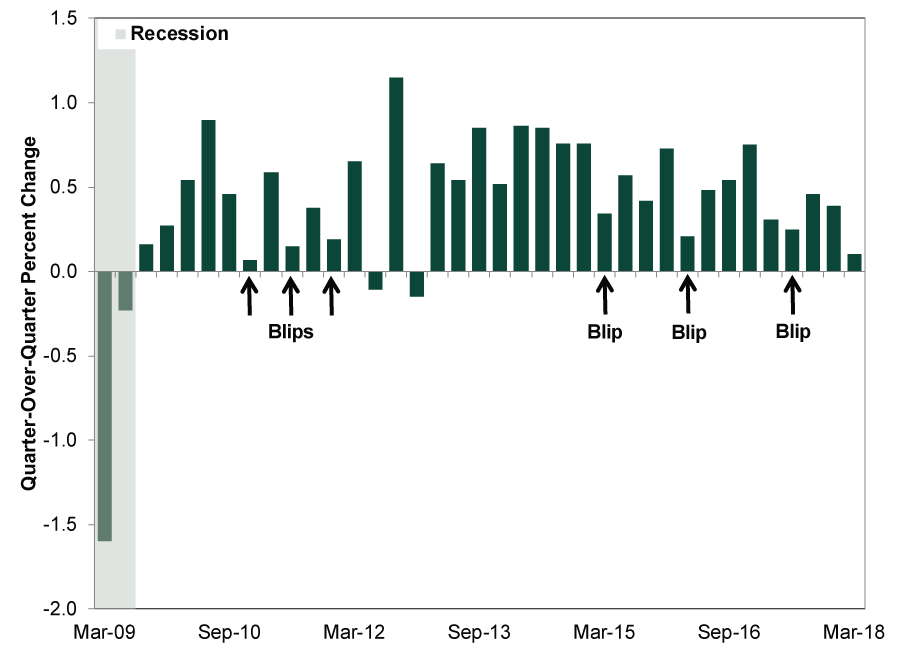

The same goes for broader readings like GDP. A slow quarter or two didn’t kill off the eurozone or UK expansions.

Exhibit 3: Eurozone GDP Since March 2009

Source: FactSet, as of 5/8/2018.

Exhibit 4: UK GDP Since March 2009

Source: FactSet, as of 5/9/2018.

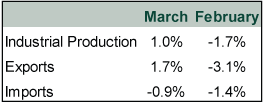

Even those supposedly worrisome German data have started bouncing back.

Exhibit 5: German Industrial Production, Exports and Imports (March vs. February)

Source: FactSet, as of 5/9/2018. Readings show month-over-month change.

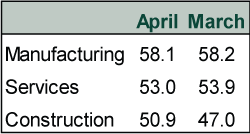

Exhibit 6: German PMIs

Source: IHS Markit, as of 5/9/2018.

Don’t forget to look ahead, not backwards—like stocks. Forward-looking markets have generally already moved on from March and April numbers. But the broad reaction to the early year slowdown indicates skepticism remains in the marketplace—potentially setting folks up for a surprise, if leading indicators are any indication.

To that end, PMIs’ New Orders subindexes for both the eurozone and UK slowed in April but remain expansionary—a positive since today’s orders are tomorrow’s production. The Conference Board’s Leading Economic Index (LEI) for the eurozone hit 0.6% m/m in March—its 19th straight positive month. In LEI’s history, no recession has started when the index was high and rising. While UK LEI has trended down for a while, a look under the hood suggests reality isn’t as bad as it seems. Sentiment-related components (e.g., consumer expectations) are dragging down the headline number—perhaps a sign of Brexit uncertainty’s impact. However, fundamental components—like the yield spread, a proxy for loan profitability—have remained positive.

Overall, the eurozone and UK’s economic soft patch to start the year doesn’t look like the start of something worse. However, many folks are quick to bemoan “peak growth” based on one report. In our view, this highlights the disconnect between sentiment and reality—a major reason we are bullish about growth in the UK and Europe this year.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Rate Decision, US-Iran, Inflation in Europe

2026-06-19

2026-06-19 -

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today