Personal Wealth Management / Economics

Perspective on China’s Historic Q1 GDP Report

GDP reporting methods vary—an important fact investors shouldn’t overlook.

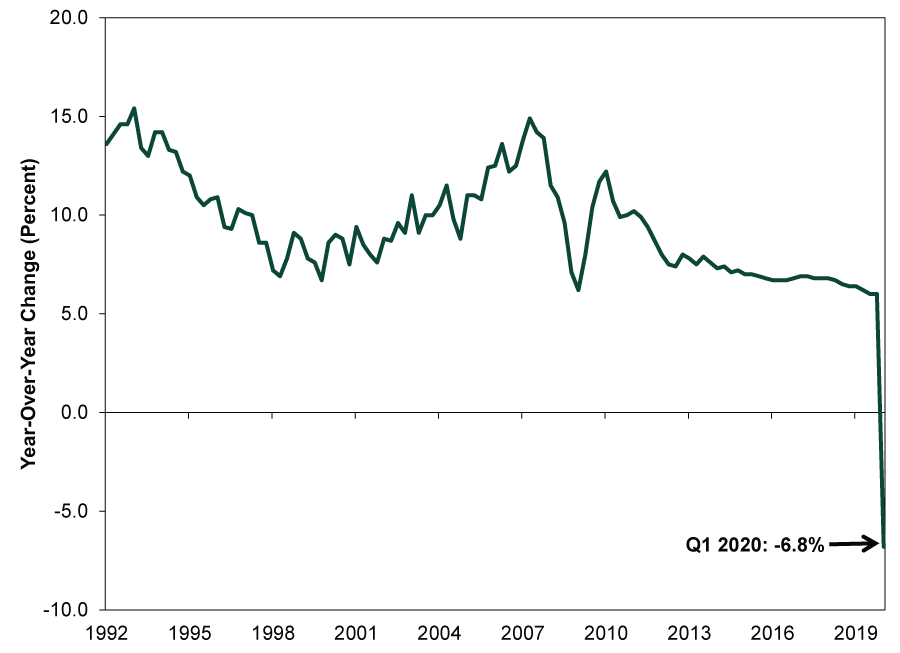

Last Friday, China reported Q1 2020 GDP fell -6.8% y/y, its first contraction since the country began reporting quarterly GDP in 1992. While this is no doubt a landmark event, it didn’t shock many. Analysts and economists widely expected a decline, to varying degrees, given the government essentially shut down the economy from late January through February to try to contain COVID-19. Some pointed out the drop was bigger than analysts anticipated, but those estimates were more like hugely disparate guesses, so we doubt that means much. Economists are now debating China’s growth prospects for the rest of the year, with most outlooks pessimistic. As many rightly point out, other major economies have virus-related restrictions in place now, and until eased, growth globally likely suffers—weighing on demand for Chinese goods. But besides the underlying details, we believe investors should also keep in mind how China reports GDP—methods vary, and comparing different countries’ headline numbers won’t always be apples-to-apples.

For historical context, here is a chart showing Chinese GDP growth since 1992.

Exhibit 1: Chinese GDP Quarterly Growth Rate Since 1992

Source: FactSet, as of 4/17/2020. Chinese GDP year-over-year growth rate, quarterly, Q1 1992 – Q1 2020.

All three major economic sectors—agriculture, heavy industry and services—contracted on a year-over-year basis (-3.2%, -9.6% and -5.2%, respectively).[i] Of 11 reporting subsectors, just 2 (Finance and Technology) grew.[ii] Any way you slice it, China’s six-week shutdown roiled the economy.

But China began easing restrictions in March, and some widely watched monthly gauges suggest certain parts of the economy were improving on a relative basis. (Note: China routinely combines many January/February monthly data points due to the shifting timing of the Lunar New Year.) March retail sales fell -15.8% y/y after plunging -20.5% in January-February, but beneath the headline figure, online sales rose, and spending on communication devices turned positive.[iii] After contracting -13.5% y/y in January-February, industrial production slipped -1.1% y/y in March—still contractionary, though a much slower pace of decline.[iv] Factories catching up on export orders boosted the gauge, though this recovery may be fleeting since foreign demand has dried up due to coronavirus restrictions. Fixed asset investment—a measure of construction and development activity—contracted -16.1% year to date (YTD) through March versus 2019’s first three months.[v] This, too, is a slower rate of contraction given the measure fell -24.5% YTD y/y in the January-February period, another signal of recovering economic activity as domestic restrictions eased.

Yet these relative improvements may not last, since major Western economies followed China’s lead in March with their own virus-containment policies. Both China’s official and the Caixin purchasing managers’ indexes (PMIs) show export orders dropped far into contractionary territory in February and March, a sign of flagging overseas demand. As many observers have noted, this development will likely weigh on Chinese output in Q2 and potentially beyond.

Looking ahead, we don’t expect a huge rebound in Q2 GDP—perhaps not even Q3. But this isn’t saying anything about the state of China’s recovery—it stems from the GDP calculation method most reports for China cite. China started reporting seasonally adjusted quarterly GDP only in 2011, and many observers are skeptical this methodology works well. Hence, pundits usually report China’s GDP growth rate on a year-over-year basis—that is to say, the current report compares Q1 2020 to Q1 2019; next quarter’s will compare Q2 2020 to Q2 2019. If Q2 2020 output rebounds rapidly, the change would be very apparent when compared to Q1 2020, when GDP fell swiftly. Yet that improvement will be nearly invisible in a Q2 2020 - Q2 2019 comparison, as the GDP base in calculation was higher in the latter. That math could obscure even a strong rebound.

Keep these reporting differences in mind as other major economies announce Q1 GDP in the coming weeks. Besides the year-over-year comparison, countries may also report GDP changes on a quarter-over-quarter basis (seasonally adjusted GDP in the current quarter versus the prior). Some also announce annualized growth rates—what the quarter-over-quarter growth rate, compounded, would equate to if it persisted for a full year. The UK and many economies in Europe primarily cite quarter-over-quarter growth while the US and Japan use annualized growth rates as their standard. (Hence, European Q1 or Q2 GDP drops may look far smaller than American or Japanese, although they may not be.) Some methods provide more granular detail, but no single reporting method is inherently better than the other. Instead, they tell you different information. But those nuances may get lost in headlines, so prepare yourself now and don’t base country-to-country comparisons on mismatched growth rates.

[i] Source: National Bureau of Statistics of China, as of 4/20/2020.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid.

[v] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today