Personal Wealth Management / Economics

PMIs, Supply Hiccups and Stocks

July Manufacturing PMIs confirm what stocks already knew.

Is the party ending? That is the question pundits asked as manufacturing purchasing managers’ indexes (PMIs) rolled in Monday. They showed continued growth on both sides of the Atlantic, with some nations even accelerating a tick. But they also showed the strain of severe supply shortages, prompting pundits to warn the economic recoveries from lockdowns are about to hit a harsh speedbump—particularly in Britain and manufacturing powerhouse Germany. We don’t doubt some businesses will have problems fulfilling orders in the near future, and that will weigh on output. But derailing the recovery seems a stretch, and markets have already signaled as much, in our view.

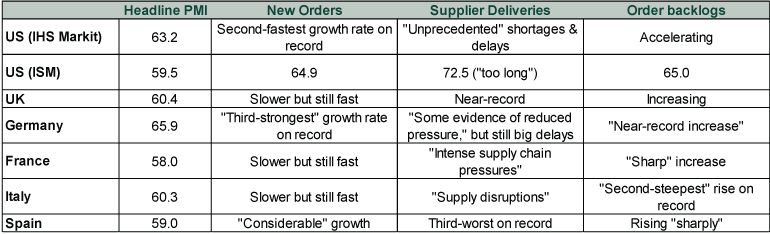

Overall, July PMIs were strong. As Exhibit 1 shows, the headline results clustered around 60—well above 50, the line between growth and contraction. New orders also grew at a fast clip, based on the commentary in IHS Markit’s press releases. That is ordinarily a great sign, as today’s orders are tomorrow’s production. But these days, rip-roaring new orders can be a headache. Supplier deliveries are on par with lockdown-era disruptions, complicating manufacturers’ ability to keep up with demand. Many are hoarding resources and components, fearing even greater supply disruptions later, and instead fulfilling orders by drawing down stockpiles of finished goods. Even so, order backlogs are growing at or near record rates in most major nations.

Exhibit 1: Dissecting July’s PMIs

Source: FactSet, ISM and IHS Markit, as of 8/2/2021. Quotes pulled from official press releases.

In some respects, this all falls into the nice problem to have, in our view. Even if factories can’t meet it right away, high demand is a hallmark of a strong economy. Plus, supply chains won’t be this stressed forever. Logistics experts quoted in much of today’s coverage anticipate a lot of the kinks will be evened out by yearend. New semiconductor foundries will take longer to come on line, but producers are basically running 24/7 to raise output in the meantime. China’s COVID containment policies do add a wildcard, as they can trigger port closures without warning, but those setbacks are fleeting. Most important, stocks have been dealing with all of these issues for months now. PMIs seemingly confirm what stocks already knew—and priced in. As we have noted before, stocks didn’t anticipate a perfectly smooth reopening—and this seems like just another facet of that.

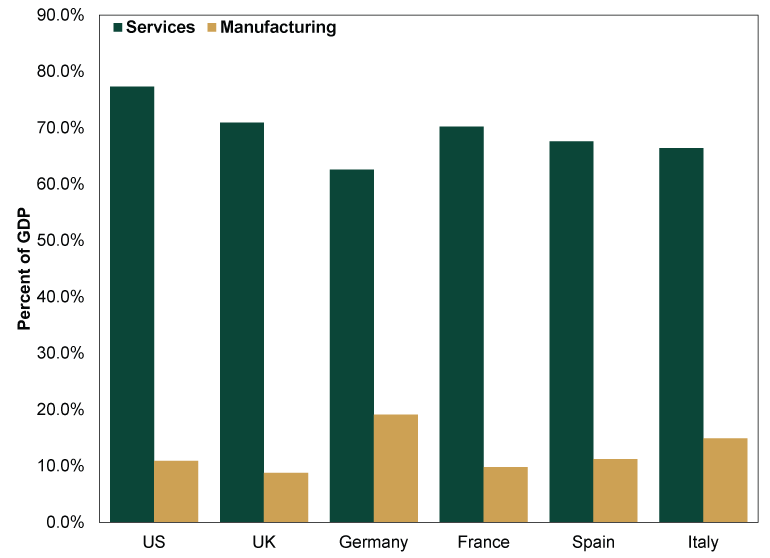

As for the broader recoveries, don’t overrate manufacturing’s influence. As Exhibit 2 shows, services—not manufacturing—comprises the lion’s share of major Western economies. Even in Germany, with its supposedly huge industrial sector and excessive vulnerability on this front.

Exhibit 2: Services Is Bigger Than Manufacturing

Source: World Bank, as of 8/2/2021. Services and Manufacturing Gross Value Added as Percentages of GDP in 2019, to avoid pandemic-related skew. World Bank figures may differ from national statistics agencies due to differing methodology.

Services firms are much more insulated from shortages of semiconductors, lumber, industrial metals and all the rest. Retailers are logically worried about holiday inventory not getting here in time, but that was also supposedly going to be an issue last year. Fear proved overwrought then, and society is overall much more adept at living with the virus now than it was then. So, it seems unlikely that retailers can’t count on Santa and the Holiday Armadillo to get presents where they need to go again this year.

In our view, the most meaningful takeaway from manufacturing PMIs probably has to do with sentiment. Judging from how most coverage presented these reports, runaway optimism hasn’t set in. If sentiment now were at dot-com bubble heights, pundits would be hyping those high headline results and gangbusters new orders, not casting supplier delivery times as a big threat. As long as pundits can still dwell on the negatives now and then, it is a sign irrational exuberance is at bay, and it adds another brick to the bull market’s wall of worry.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today