Personal Wealth Management / Market Analysis

Random Musings on Markets—Episode IV: A New Musing

This week’s roundup of randomness features fund flows, possible US legislation creating a “new” retirement savings vehicle, UK energy price caps and more.

Image created using StarWars.com Title Crawl Generator.

Don’t Go With the Fund Flows

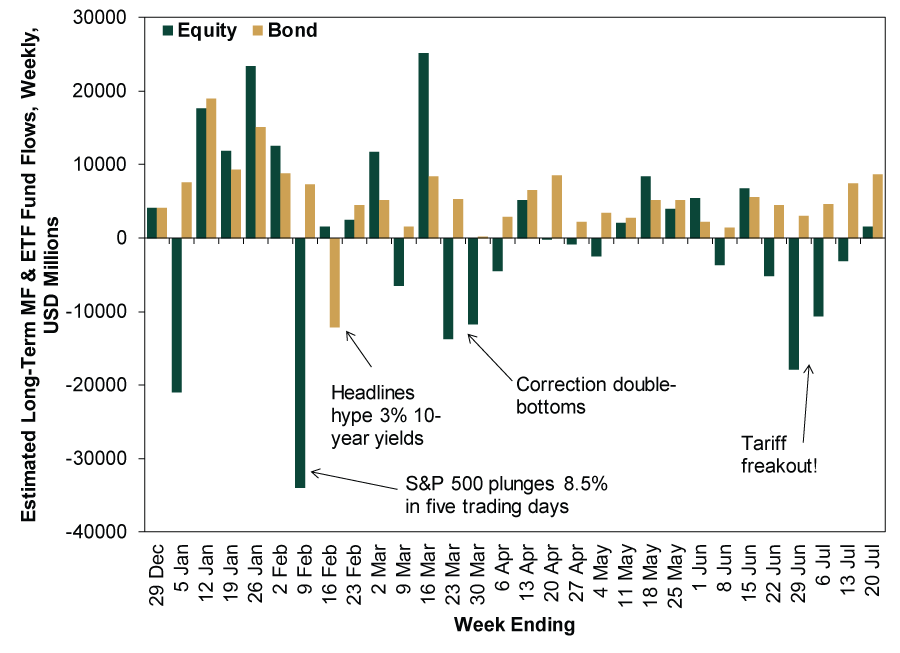

The S&P 500 Total Return Index hit a new all-time closing high Wednesday, making it official: US stocks’ correction is over. It bottomed on February 8, retested the low on March 23 and April 2, then churned back to breakeven in a little less than four months. To celebrate, and inspired by a Wall Street Journal article that caught our eye Thursday morning, we decided to take a peek at weekly fund flows for a quick and dirty look at how investors reacted to the market’s twists and turns. Turns out, folks did about what we’d expect: behaved badly. They reacted to short-term volatility and headline risks, fleeing in February’s first week, late March – early April and late June – early July as tariff chatter dominated. Bond investors weren’t much more disciplined, as the sole week of bond fund outflows occurred while headlines were warning of imminent danger if the 10-year yield hit 3% (at the time, it was around 2.9%). Granted, this isn’t an air tight indicator, as people could have swapped funds for individual stocks and bonds instead of parking in cash, but it is illustrative.[i]

Exhibit 1: Investors Get All Reactive

Source: FactSet, as of 7/26/2018. Estimated long-term mutual fund and exchange-traded fund flows, total bonds and total equities, weekly, 12/29/2017 – 7/20/2018.

We aren’t going to argue any of this is predictive. It isn’t! But it is telling about sentiment and how hard it is to stay disciplined when the going gets tough. Selling stocks in early February or late March/early April might have felt good. But it would have been a poor decision, locking in losses and raising the likelihood you missed the rebound. Same goes for selling during the Great Tariff Freakout of Mid-2018. Times may change, but classic investor behavior doesn’t. Remember this the next time markets fall fast and headlines warn they are circling the drain.

The House Proposes Legislation to Change Retirement Savings … Branding

Tuesday, House Republicans including Ways and Means Chairman Kevin Brady (R-Texas) introduced a bare-bones plan they seem to have colloquially dubbed, “Tax Cut 2.0.” This timely[ii] plan aims to make 2017’s (presently temporary) individual tax cuts permanent. Included within it is a provision seeking to create a new tax-favored retirement savings account called a Universal Savings Account (a USA!). We were curious and thought you’d be too, so we did some digging.

The details on this are truly lacking, considering there isn’t even legislation to read. But our research revealed a very similar vehicle of the same name—and acronym!—proposed in legislation last year by Rep. Dave Brat (R-Virginia). This vehicle would allow investors to plow after-tax funds into their USA and choose from a wide range of investments, like a Roth IRA. Withdrawals would be tax-free, like a Roth IRA. Contributions—under Brat’s plan—would have been capped at $5,500. Which … is … the … Roth IRA limit?

The discerning reader may now be wondering: Is the plan to re-brand the Roth? But it seems a little bit more than that. At least under Brat’s idea, there are few limits on withdrawals, so the funds could be used for lots of non-retirement expenses. (Cue behavioral finance debate over the wisdom of this.) Still, we wonder why they don’t just propose amending Roth IRAs legislatively, as it would be easier. Or, if the intent is to boost savings, just double the darn limit and keep giving late Delaware Senator William Roth his due.

Now, as noted, we are piecing together what this thing is. It may be totally different! But either way, Tax Cut 2.0 seems mostly like midterm electioneering and faces difficult odds of passing. So this is likely both a random and irrelevant musing.

UK Parliament Pauses Gridlock, Passes Most Feckless Energy Price Caps Imaginable

Alas, we can no longer quip that the most noteworthy non-Brexit-related bill passed by Britain’s parliament this year is the measure to add a third runway at Heathrow: Last week, the governing Conservatives and opposition Labour went all bipartisan and passed a bill to cap some home fuel prices. But before you worry the UK is going the way of Venezuela, Cristina Kirchner’s Argentina or Nixon’s America, take heart—these caps target a limited number of households and should have minimal economic impact.

We say this not knowing what the actual caps are, as regulators have a few months to hash out the final details. However, we do know they will run through 2020 and apply only to households on a “standard variable tariff.” These, rather than “fixed-rate tariffs,” are the source of politicians’ ire, as they are less economical but often used by lower-income households. Most folks on these plans don’t shop around each year in search of a better deal, instead just going with whatever new rate their current provider adopts. So for the next couple years, regulators will cap the price and see if households are better off.

Only 12 million UK households currently use standard variable tariffs—fewer than half of total UK households. So this isn’t hugely far reaching. Moreover, unlike the price controls mentioned earlier, which were sweeping, these apply to only one tiny niche of the UK economy. Therefore, their total impact should be minimal. Some UK energy providers took a hit as the bill percolated through Parliament, but UK stocks overall have fared fine. Those energy providers will probably be fine, too, as they are simply rushing to hike prices before the cap takes effect.

While this is a notable break from gridlock, we think it is the exception—not the rule. This was a rare area where Labour and the Conservatives have agreed for a while, as we noted after last year’s snap election. Former Labour leader Ed “I Know, I’ll Carve My Manifesto on a Stone Tablet” Miliband ran on them in 2015’s election, and May adopted them for her 2017 campaign. Yet despite the parties’ philosophical agreement, even this small compromise took over a year to reach as Labour kept trying to toughen the bill and pilloried May for not going far enough. If Labour and the Conservatives can barely even agree when they agree, we suspect little else will get done from here.

A Totally Speculative Theory About the BoJ

Last Friday, Reuters reported BoJ policymakers are considering “tweaks” to the central bank’s massive quantitative easing (QE) program and its cousin, yield curve control, in which the bank targets a 0% 10-year bond yield. The ever-reliable unnamed sources familiar with the bank’s thinking said a policy shift toward higher long rates could be in the offing. Japanese 10-year bond (JGB) yields “soared” as “high” as 0.09% in response, leading the bank to offer to buy an “unlimited” amount of bonds on Monday and leaving investors rather confused about what could happen at the bank’s July 31 meeting.

As ever, we wouldn’t expend much energy trying to figure out the BoJ’s next move. Central bankers are inherently unpredictable. While the BoJ seems more or less aware QE isn’t helping Japan reach its inflation target and has no doubt heard banks’ many complaints about negligible profit margins stemming from that 0%-ish 10-year yield, that doesn’t automatically mean QE’s end is near. They could easily cook up something kooky. Plus, we have long theorized that all this QE nonsense in the Western world was about rebuilding bank balance sheets, not actually stimulating the economy. And there is one particular Japanese bank that has long seemed to need some balance sheet help: Japan Post, which The Wall Street Journal once dubbed “the bank that ate Japan” because of its massive JGB holdings. Shedding JGBs has been on the bank’s to-do list since it was partially privatized in 2015. According to its latest report, JGBs have dwindled from 51.8% of Japan Post’s total investment portfolio on 3/31/2015 to 30.2% on 3/31/2018.[iii] In the last two years alone, it has shed ¥19.5 trillion ($175.3 billion) worth of JGBs.[iv]

Now, none of this necessarily means Japan Post has been selling JGBs to the BoJ—whenever Japan Post releases its results, its own unnamed sources frequently try to assure reporters that it simply let maturing JGBs roll off its balance sheet. But considering Japan Post has long been one of the Japanese government’s biggest funders, it would have a hard time letting its massive holdings roll off if the central bank weren’t ready and willing to pick up the slack. Hence, we have a totally speculative hypothesis: Japanese QE will end once Japan Post decides its JGB holdings are at an acceptable level. If we are wrong, we will metaphorically eat crow—and if we are right, we will pat ourselves on the back. Watch this space.

FBI’s Carter Page Documents Show Investors [REDACTED]

To start the week, the never-ending media firestorm that is Donald Trump’s presidency stoked bipartisan animosity once again. Following Congressional pressure, the FBI released the documents (see them here) it submitted to a Foreign Intelligence Surveillance Court to obtain a warrant on Trump campaign official Carter Page. Congress wanted to know: Was there more justifying this surveillance than the discredited Steele Dossier (as some call it)? If it was the sole evidence, were the motivations actually political?

Trouble is, we in the public learn nothing from this. The document was heavily redacted! Blacked out! No conclusions could possibly be drawn, though that didn’t stop media from trying. (Predictably, left-leaning media argue it vindicates the FBI; right-leaning media say it is damning evidence of political motives within the so-called “deep state.”

For investors, the real conclusion you ought to draw from this is simple. We know many investors, particularly those with strong emotions, are watching the Russia investigation—and all its angles—with bated breath. Our advice here is simple: Whatever you think the situation actually is, don’t let it weigh on your market views. And, until there is evidence you suspect the Senate will vote to convict Trump in an impeachment hearing upon, this is noise. And, crucially, even then it may still be, given there isn’t history suggesting impeachment or ouster of a president is bearish. As ever, we urge investors to leave politics out of portfolio decisions. End.

Also in political news, Senator Orrin Hatch rose from the dead. Not really, of course. He isn’t a politico-zombie! Hatch is very much alive, as his social media team hilariously demonstrated. But Google’s instant answers claimed for a short time that the Senator had passed on September 11, 2017. Nobody is perfect, we guess. That said, we wonder if Sen. Hatch has a thing or two to say about the notion big Tech should be fact-checking the entire internet?

All jokes aside, we see this as a humorous reminder that the onus to judge factual accuracy on the internet lands squarely on consumers. Skepticism is your best weapon.

Enjoy your weekend!

[i] Always be skeptical of a dataset that ignores the counterfactual!

[ii] Just before midterms!

[iii] Source: Japan Post Bank, as of 7/26/2018. Results for the Fiscal Year Ended March 2018.

[iv] Ibid. Results for the Fiscal Years Ended March 2017 and March 2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today