Personal Wealth Management / Market Analysis

UK Election Results Surprise but Aren’t a Gamechanger

The UK election's outcome hasn't increased political risk for stocks.

In the wee hours of the morning last Friday, a sweeping tide swept over the UK-a tide of soul-searching pollsters and introspective politicians, all flummoxed by the Conservative Party's shock general election win. No hung Parliament. No coalition negotiating. No horse-trading. Scottish nationalists in 56 of their country's 59 seats. Frontline politicians from the Conservatives, Labour and Liberal Democrats out of a job. Three party leaders resigned. One later un-resigned. Two veteran pols reneged on pledges to eat items of clothing if early exit polls predicting a Conservative victory ended up correct.[i] Four days later, with the first Conservative cabinet in 18 years ensconced at Whitehall, the post-mortem isn't slowing down-including questions on what the outcome means for stocks. In our view, it doesn't mean terribly much, good or bad. While a majority government may loosen political gridlock somewhat, it seems premature to conclude sweeping, fast-moving legislative change looms. While some aspects of the outcome are worth watching, political risk for both UK and global stocks remains low for the foreseeable future.

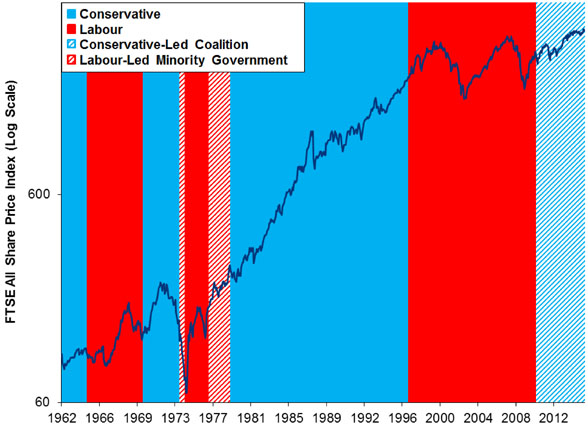

UK markets initially cheered the outcome, perhaps out of relief over a clean, concise result-hung parliament jitters had clearly dampened sentiment as the contest approached. Some have suggested stocks are also cheering the arrival of a pro-business government, but that's bias talking. No party is inherently good or bad for stocks. Nor is either party inherently pro- or anti-business. Perhaps stocks are relieved some of the iffier items on Labour's agenda-namely, heavier bank regulation and price controls-are now far less likely. But the last five years are riddled with evidence the Tories aren't innately business-friendly-like the bank balance sheet tax, the UK's version of the Volcker Rule, and several ineffectual public/private lending programs. Our advice: Set aside opinions for and against all parties, and always bear in mind both parties have presided over bull and bear markets alike (Exhibit 1). And look at the whole history-not just the big rise in the Thatcher/Major era or the twin boom/busts in the Blair/Brown years. All were global events, not driven solely by UK politics.

Exhibit 1: UK Stocks by Party

Source: Factset, as of 4/9/2015. FTSE All-Share Price Index, 4/30/1962 - 3/31/2015. Price returns used instead of total due to data availability.

Stocks don't care who's in charge. They care whether property rights, regulations and the distribution of resources and opportunity are likely to change-policies and downstream consequences. Hence why stocks are often happiest when governments are gridlocked, reducing legislative risk. Risk does technically get a wee bit higher now that the UK has a majority government. Yet hurdles to major legislative change remain. The majority is razor thin: 331 seats of 650, not exactly a mandate for extreme reform. A revolt from just seven backbenchers could thwart proposed legislation or force Prime Minister David Cameron to rely on support from smaller parties, like the unionist parties in Northern Ireland-a politically risky move, as John Major and Gordon Brown learned the hard way.

Cameron's majority could easily evaporate, too. Currently, he has a 12-seat lead on the combined opposition-16 if you include the four Northern Irish seats held by Sinn Féin, which abstains from Parliament on principle.[ii] John Major had a bigger margin, 21 seats, after his own shock win in 1992.[iii] Like Cameron, he had to deal with a ferocious euroskeptic backbench while negotiating Britain's relationship with the EU. Nor were they keen when he signed the Maastricht Treaty, even though he won exemptions, including keeping the UK permanently out of the euro. Between the defections and a wave of by-election defeats, his majority was gone by the end of his term. That doesn't mean Cameron's term necessarily goes the same way, but it speaks to the amount of political capital he will have to deploy over the next five years-particularly since defections and by-elections weren't kind to his party during the Coalition's tenure.

This, of course, raises one of the two big question marks surrounding Cameron's government: Europe. To quell euroskeptic rebels in 2013, Cameron pledged to renegotiate Britain's relationship with the EU and hold a referendum on membership, under those revised terms, by 2017. This has raised fears of "Brexit," which most of the business community fears-despite Brussels' penchant for red tape, the EU's single market is a free-trade marvel. While anything is possible, it seems awfully premature to fear stock market fallout at this point. For one, neither Cameron nor EU officials want the UK to leave, giving both sides an incentive to negotiate. European Commission President Jean Claude Juncker has already indicated a willingness to make concessions. If Cameron gets most of what he wants, the changes (which include repatriating judiciary and police powers, curbing "benefits tourism" and regaining some financial regulation autonomy), that could well appease the euroskeptics. Either way, this is an issue that will play out glacially, in public, giving markets lots of time to discover and discount any potential changes. The EU is notoriously slow-moving, and if any of this ends up requiring treaty revisions, it could take years.

The other question lies on the home front: Scotland. With the Scottish National Party (SNP) taking 95% of Scotland's seats-but having no representation in government-questions of legitimacy and accountability will undoubtedly arise. Cameron is already trying to head this off by pledging to pass the reforms agreed-to by all major parties after last year's independence referendum, which would transfer mineral and land-use rights and oil and gas extraction licensing from the Crown to the Scottish Parliament, give the Scottish Parliament more autonomy over benefits, and grant more autonomy over taxation. Yet the SNP, a party to the original agreement, says this doesn't go far enough-in light of their electoral triumph, they're now pushing for full fiscal autonomy.

This debate seems unlikely to splinter the UK within the foreseeable future, given exit polls suggest the SNP's victory had more to do with their claim as the sole anti-austerity party, which outflanked Labour, and don't suggest a surge of nationalism in Scotland. That, plus the fact she has an election to fight in Scotland next year, explains why SNP leader Nicola Sturgeon is pressing for devolution, not independence (for now). However, whether or not Parliament maximizes devolution above and beyond the initial agreement, questions remain. After the independence referendum, Cameron implied Wales would get more powers, too.[iv]Ditto for England, where the concept of "English votes for English laws" is gaining traction. It wouldn't surprise us if the UK inched ever-closer to federalism, though this, too, likely plays out slowly and publicly, with lots of horse-trading among major parties. Devolution is simply too politically sensitive an issue to pass along party lines-particularly when Labour holds 25 of Wales' 40 seats.

As these issues play out, pundits will likely whip up a frenzy with phrases like "Constitutional Crisis," and it will sound scary. But the devolution and European questions don't represent huge, sudden shifts in how the UK is governed and where it stands in international markets. These are slow-moving, long-term issues-the sort of things stocks tend to price gradually as new information emerges. That's true whether they're pricing in positive changes or negatives. Slow-moving processes that play out in the public eye give investors time to digest the implications, good and bad, making a surprising jolt (good or bad) to markets unlikely.

Stocks move on probabilities, not possibilities, and it's impossible to assign probabilities to either of these issues this far in advance. So we suggest you not speculate too hard, and look instead where stocks are looking: at what's likeliest over the foreseeable future. That list includes continued economic growth, improving fundamentals in the banking sector, low-ish legislative risk, and a reality that overall beats expectations. Don't get hung up on scary unknowns: The nearer-term outlook for UK stocks looks plenty bright.

[i] Former Liberal Democrat leader Paddy Ashdown said he'd eat his hat. Tony Blair's old spin doctor, Alastair Campbell, said he'd eat his kilt. They eventually settled on eating chocolate versions of said clothing on a post-election Question Time special on the BBC. Quite sporting, gents.

[ii] Sinn Féin is the political wing of the former IRA, and their chief aim is a united, republican Ireland. They control Northern Ireland's devolved legislature in a coalition with the two main unionist parties and a handful of others, and they do show up for the Assembly sessions.

[iii] The parallels between these contests are striking if you're a political nerd like us. For instance, Google "Neil Kinnock, we're alright" and "Ed Miliband, stone tablet." It's all sociology, which stocks don't care about, but fascinating.

[iv] Wales merits a post-election article of its own. For all the talk of a rising tide of nationalism. Wales' nationalist party, Plaid Cymru, gained no seats last week. The Conservatives even stole three seats, both in North Wales (which is less anglicized and more supportive of home rule) and South Wales (a traditional Labour stronghold). Voters there, as in England, lacked a strong anti-austerity alternative, leaving them to choose based on much different issues and leading to different, less nationalist results.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today