Personal Wealth Management / Market Analysis

Random Musings on Markets XII: Musings of Boulder Pass

In which we offer you an eclectic menu of random financial news tidbits.

This week, our please-don’t-expect-this-every-week selection of random financial news includes snippets on new Fed friends—and what they say about the bank’s allegedly threatened independence, potential border trouble for pot investors, a look inside a bitmining firm, our working theory on trade wars and more.

New Fed Friends and Independence

Ever since President Trump allegedly “broke with decades of presidential precedent” and stated a preference for low interest rates, media has spilled billions of pixels about the implications of the White House encroaching on the ostensibly independent Fed’s territory.

Thursday was no exception, when one Bloomberg column documented a theory on Jerome Powell’s ever-so-fun approach to Winning Friends and Influencing People. The column asserts the folksy Powell is eschewing his predecessors’ ivory tower approach to the institution, gladly “pressing the flesh”[i] with lawmakers. Congressional support, the argument goes, is his insurance against an overactive White House, safeguarding Fed policy from interference.

We understand and agree politicized monetary policy could be very bad. Yet realistically, to the extent Fed independence is a thing, it is very odd to think glad-handing and schmoozing a bunch more politicians is the fix. Those were the people who just wanted to audit the Fed a couple years ago!

But also, the extent of Fed independence doesn’t seem to stretch real far. Presidents have frequently stated a preference for lower interest rates over the years. The Fed followed the Treasury’s lead during WWII, leading an effort to peg interest rates to facilitate wartime borrowing. And, as the article even notes, the whole “independent Fed” concept wasn’t a thing until the Clinton administration. We will also add the fact the Bernanke Fed and Paulson Treasury worked closely with each other in 2008, with Bernanke often following Paulson’s lead.

It doesn’t seem to us Trump’s statements are really encroaching on the Fed’s territory as much as some think. The latest evidence: Thursday night, Trump tapped Nellie Liang to fill the last open seat on the Fed’s Board of Governors. Liang is a former Fed economist and a senior fellow at the Brookings Institution (where, perhaps not coincidentally, Ben Bernanke now blogs, albeit really, really, really infrequently). Liang is also buddies with Powell! As Bloomberg reported separately, “Fed Chairman Jerome Powell has worked with Liang and held a party at his Maryland home last year when Liang departed the Fed.” As for her policy stance, there is no word on how long they left the punch bowl out.[ii]

This Is Not Investment Advice. Or Legal Advice.

Adding to our long list of reasons not to get too high on cannabis-related stocks in the wake of legalization in Canada and some US states, Politico reported last week that the US Customs and Border Protection agency will treat investors in marijuana companies as complicit in illicit drug trafficking, a violation of federal law and grounds for a lifetime travel ban. Now, this applies to Canadian travelers, not US citizens, but it does raise a few questions for Americans who want to invest in these buzzy companies. Such as:

Will owning stock in a Canadian cannabis company be grounds for prosecution?

Will said Canadian cannabis companies be able to issue ADRs, or will Americans have to buy foreign ordinaries (i.e., foreign stocks on a foreign exchange), with all the requisite hassle and extra costs?

Will owning stock in Heineken be a federal crime? After all, Heineken owns craft beer titan Lagunitas, which produces sparkling water infused with THC.

Will owning stock in Coca-Cola be a federal crime if it proceeds with plans to pursue wellness drinks infused with CBD (the other cannabinoid, the one that doesn’t make you high but is still a banned substance)?

Will owning stock in Molson Coors, which is developing cannabis-infused drinks for eventual sale in Canada, be a criminal act?

Will owning stock in Constellation Brands, which owns Corona as well as a 38% stake in a Canadian cannabis producer, get you in hot water?

We mean, probably not? At this late juncture, it would be ridiculous. If the feds haven’t prosecuted the good folks at Lagunitas or the top brass at Molson Coors and Constellation, it seems highly unlikely that they would go after Jim or Sally Shareholder. European authorities haven’t gone after Heineken, which is headquartered in the Netherlands, for drug trafficking. Moreover, the new regulatory guidance for Canadian travelers doesn’t even seem all that feasible to us. Customs and Border Patrol doesn’t seem to have the means or authority to demand Canadians entering the US disclose their brokerage statements. Further, will they judge this based on what share of a firm’s revenue is tied to cannabis? So many questions! Anyway, score a couple points for the battle against regulatory overreach. But this does highlight the haziness surrounding the budding industry and the potential for unexpected regulatory wrinkles.

Bitmining

The shine is clearly off bitcoin and fellow cryptocurrencies in 2018. Since peaking on December 16, 2017, bitcoin is down 66.6% year to date.[iii] Bitcoin Cash, its spinoff, is worse, down 88.4% from its December 20 high.[iv]

We will admit our interest in this subject, as well as much of the media’s and general public’s, has waned alongside bitcoin’s price. It was, for a spell, a fascinating study in bubble behavior. But now? Not as much. And you can only read so many articles touting the blockchain as technology revolution 2.0 or pondering potential crypto securitization before you enter a near catatonic state of boredom. It is a lot like watching the Emmys or listening to Brexit chatter in that way.[v]

Yet somehow, Bloomberg’s Tim Culpan found a way to cut through all that and win our interest. This week, Culpan covered Bitmain, perhaps the most out-of-favor security offering in recent memory. Bitmain is a Chinese cryptocurrency mining-equipment firm slated to go public in the relatively near future. Not only is it engaged in out-of-favor bitcoin and domiciled in out-of-favor China, it gets worse: The firm takes payment only in cryptocurrencies—not cash—and shifted all its holdings into Bitcoin Cash early this year, amplifying the downside and complicating already dodgy financials. Not a good move. The IPO, we dunno, seems poorly timed? (If it happens any time soon.)

Anyway, what we loved about Culpan’s article is it refers to Bitmain as if it actually mines stuff. Not bitcoin, we mean, stuff. It references “shovels,” “rigs” and “drilling.” It dove into theories about whether Bitmain would suffer if the cryptocrash meant less mining activity, a la the 2014 – 2016 oil crash. It is crypto-as-commodity! Folks reacting to price signals! We loved it. It spurred a few weird questions in our nerd brains: Who tallies the crypto rig count? Are there cryptocartels like OPEC? Can you bitfrack?

Anyway, we have no takeaway for you here, we just recommend the article. Oh, and this isn’t investment advice, but maybe just maybe don’t buy Bitmain. Or bitcoin for that matter.

A Working Theory on Trade Wars

As the sub-header alludes, we have a new pet theory about trade wars: When it comes to stocks, trade wars (or skirmishes) are like actual wars (or skirmishes).

As we have written just about every time armed conflict has threatened to break out in the world over the last decade or so, markets usually see through regional skirmishes. You often get some volatility in the run-up to the conflict, as tensions flare and uncertainty spikes, but stocks usually move on shortly after bullets begin flying. Investors realize the conflict is localized, impacting a very small section of the global economy, while life and commerce go on as normal in the vast majority of the world. You can see this pattern in market returns surrounding the Korean War, 1967’s Six-Day War, the 1990s’ Bosnian War, both Iraq wars, 2006’s conflict between Israel and Hezbollah, the present Syrian conflict and many others. Since good stock market data begin in 1926, only one armed conflict has caused a bear market: World War II. It takes sweeping, global war to knock the global economy and markets off course.

Welp, we are seeing similar today with tariffs. As we have written numerous times this year, present tariffs don’t add up to a full-blown trade war. For an actual trade war, see the 1930s, when the global blowback to America’s sweeping Smoot-Hawley tariffs erected massive trade barriers worldwide, causing massive disruptions. Back then, the US’s total effective tariff rate on imports for consumption was 19.8%. Today, if President Trump were to go through with his latest threats to add tariffs to all Chinese imports, the total effective tariff rate would be a little more than one-fourth of that. All new tariffs enacted by the US this year—and retaliation—would be less than 0.2% of global GDP. In other words, we think you can call this a regional trade skirmish.

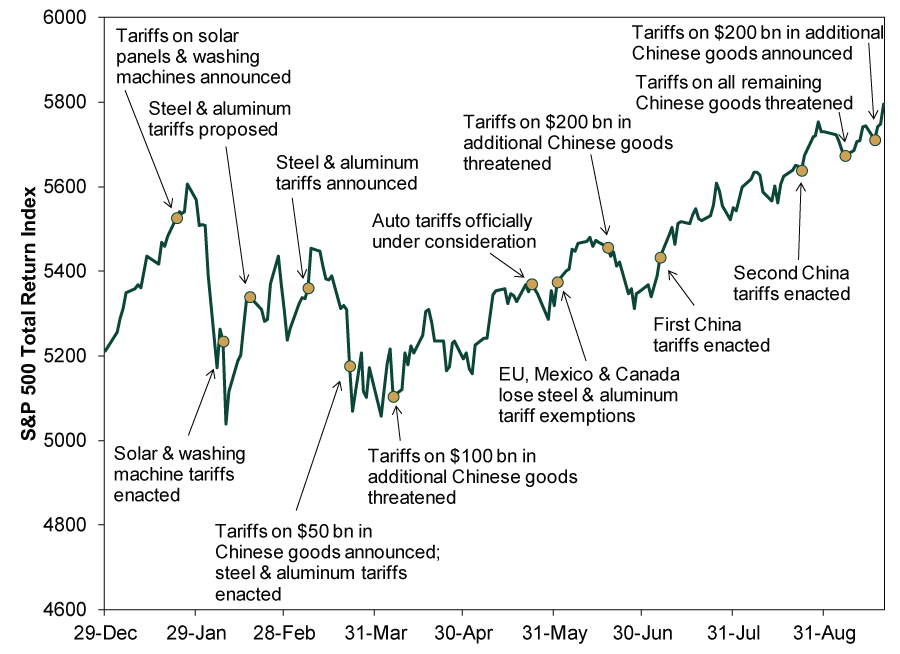

Markets seem to be reacting to this as they typically do to actual geopolitical skirmishes: rocky in the run-up as uncertainty flares, followed by a recovery as the small scope becomes apparent. You might have seen the S&P 500 hit an all-time high yesterday, just three days after Trump announced a new round of Chinese tariffs (this time on an additional $200 billion in goods). Exhibit 1 shows the index year to date, with major tariff-related developments highlighted.

Exhibit 1: Sell the Rumor, Buy the News?

Source: FactSet and a Google News search, as of 9/20/2018. S&P 500 Total Return Index, 12/29/2017 – 9/20/2018.

Just as we wouldn’t say bullets are bullish, neither are tariffs—that isn’t the point. Rather, markets move before widely expected events. When investors talk about a potential thing for months, it is probably priced in by the time it actually happens. So we think reacting to tariffs now, when markets have seemingly moved on, would be a backward-looking move.

Public Service Announcement

From today forward, it is no longer correct to call the FANG stocks “tech titans,” “tech giants” or anything else with “tech” in the title. Such taglines were only ever half-true, as the A (Amazon) and N (Netflix) were Consumer Discretionary stocks, not Tech. But now none of them are, as the F (Facebook) and G (Alphabet, née Google) are joining the N in the brand-new Communication Services sector. So none of these huge supposedly tech-ish stocks are actually Tech. And only half of them are technically ex-Tech, so that won’t fly, either.

So what can you call them? Well, we’d rather people just get over the whole business of snappy acronyms and arbitrarily lumping things together, because lumping FANGs makes about as much sense as lumping the BRICS together. Brazil isn’t Russia isn’t India isn’t China isn’t South Africa. But if you simply must keep the FANG moniker alive, we guess you could refer to them as really big companies that do things on the Internet? Online places where you can watch, buy and look for things? Big companies that love your data? Four non-Techs?

Life Imitates Star Trek: Discovery

Yesterday, Vodafone conducted the UK’s first live holographic phone call to much fanfare, enabling ace footballer Steph Houghton to virtually high-five one of her fans, an 11-year-old girl named Iris—who happened to be on a stage 186 miles away. The English Women’s Team captain showed off some moves, and the wonders of 5G wireless technology bowled the crowd over. This isn’t the world’s first holographic call—that happened a few months ago—but it strikes us as a pretty great sign of things to come. Those controversial hologram calls in Star Trek: Discovery suddenly seem a lot less fanciful.[vi]

This technology probably won’t be broadly available for several years. Telecom bigwigs made a big splash with the first cell phone calls in the early 1970s, but they were still a little-used luxury by the time Cher and Dionne used them to comic effect in 1995’s Clueless. They didn’t become ubiquitous until around 2000 or so. But, the demo does highlight how much untapped potential there is in the tech world. Faster, better and clearer communication is one of the biggest drivers of long-term advancement, along with Moore’s Law, energy efficiency and exponentially growing data storage. We can’t even begin to imagine what creative users could do with holograms and the other fruits of 5G, which reduce network latency and improve rural reach, among other things. If you doubt how far this could spread, just think about how many objects in your home include computer chips—and how many could connect to your Internet.

So chalk this up as yet another reason we don’t think the global economy has come anywhere near a limit to growth—and a reason stocks have as much long-term potential as they always did. Just as cell phones have come a long way since Motorola engineer Martin Cooper first phoned his rival, Bell Labs’ Joel Engel, with a brick-sized handset in 1973, so, too, can holograms and 5G mushroom over the next few decades. To keep with the Star Trek theme and paraphrase Wil Wheaton, ain’t it cool to live in the future?

Enjoy your weekend!

[i] We believe this awkward term refers to shaking hands.

[ii] {rimshot} This is a joke based on the famous William McChesney Martin quip that the Fed’s economic role is to serve as “a chaperone who has ordered the punch bowl removed just when the party was really warming up,” an analogy claiming the Fed’s role is, in part, to prevent economic overheating. Have we over-explained this enough?

[iii] Source: CoinMarketCap.com, as of 9/21/2018. Bitcoin return, 12/16/2017 – 9/20/2018.

[iv] Ibid. Bitcoin Cash return, 12/20/2017 – 9/20/2018.

[v] Yup. We said it.

[vi] The producers got some flak for including tech that was clearly more advanced than the original Star Trek, which some consider a continuity violation since Discovery takes place 10 years earlier. Elisabeth, our resident Trekker, is over it and waiting to see how they render the Enterprise’s interior in Season 2.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today