Personal Wealth Management / Economics

Read Past the Headline

December's eurozone prices posted their first annual decline since 2009. But this deflation doesn't look like bad deflation when you look beneath the surface.

Wednesday, European media took a bit of a breather from hyperventilating over political strife in Greece to hyperventilate over deflation, which by one measure, the eurozone is now in. Cue the calls for QE (quantitative easing). Thing is, this is an overblown fear-the eurozone's deflation exists only by one heavily skewed measure, and it's about as mild as mild can be. There is little evidence this is at all problematic, and in some ways, it should be positive for the eurozone.

While not all the media is fearful, suffice it to say a common theme presumes a deflationary spiral looms for the eurozone.[i] Low inflationary and occasionally disinflationary readings have often been interpreted as skating on thin ice. So when the eurozone's headline December Harmonized Index of Consumer Prices (HICP) revealed a -0.2% y/y decline-the first negative year-over-year read since 2009-folks fretted the ice had cracked. Now some fret consumers will hold off on purchases, awaiting cheaper prices. Others worry deflation weighs on borrowers, since funds used to repay are worth more in purchasing power terms than the principal they borrowed.

But one month's headline data showing falling prices does not a deflation doom make. December's read was heavily skewed by falling energy prices. Energy alone fell -6.3% y/y in the month, a far deeper dip than November's -2.6%.

And here is the thing about the prior paragraph: Is anyone surprised? There have quite literally been thousands of articles documenting declining energy prices of late. Brent crude, a global benchmark, fell -49% in 2014. Around the world, folks have kind of noticed.

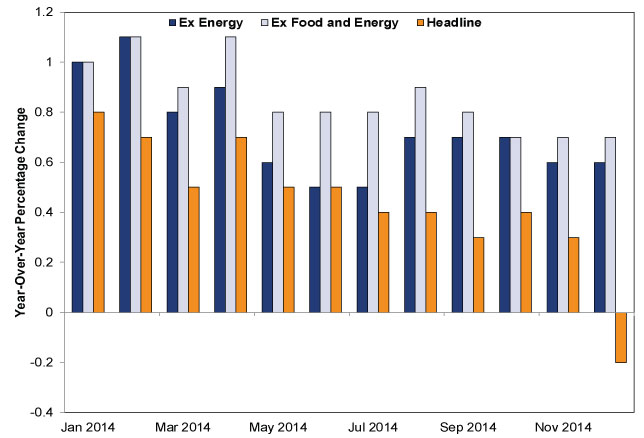

Excluding Energy, prices rose 0.6% y/y, the same pace as in November. The only other major bucket of falling prices? Unprocessed food, which is also a historically volatile category subject to lots of non-monetary factors, like weather. Exhibit 1 shows HICP, HICP ex. Energy and core HICP.

Exhibit 1: Negative Eurozone Inflation Is Limited to Volatile Categories

Source: FactSet, eurozone Harmonized Index of Consumer Prices, January 2014 - December 2014.

The biggest single component in the eurozone CPI gauge? Services, which rose 1.2%-the same rate as in the past two months and virtually unchanged since July.

Here is another thing about those falling energy prices: They are not a broad negative monetary policy needs to counter. Falling energy prices create winners and losers. Firms in the 19 eurozone members[ii] likely benefit from falling input costs. In addition, consumers likely gain leeway to spend on other goods and services. They gain room to save or deleverage. None of these square with the theory this deflation is bad deflation. That point was echoed recently when the ECB announced money supply grew at a fine, if unspectacular, clip recently.

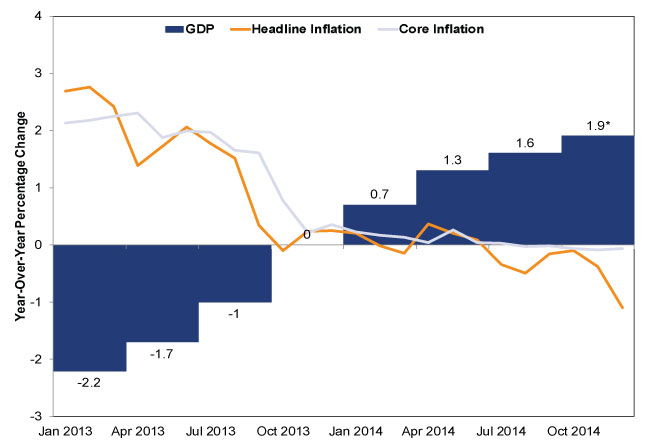

In general, the notion mild deflation is so terrible is actually a wee bit wide of the mark. The cause matters. Consider Exhibit 2: Spanish GDP, headline and core HICP. As inflation fell into deflation, GDP went from contraction to expansion. The cause of this deflation? Partly energy prices, partly falling labor costs due to reforms. The Conference Board's Leading Economic Index for Spain suggests growth will continue, too. Where is the sign this deflation is bad?

Exhibit 2: Spanish GDP, Headline and Core HICP

Source: FactSet, Bank of Spain. Real GDP (y/y), Q1 2013 - Q4 2014 (*Q4 GDP figure cited (1.9%) is the Bank of Spain's estimate as of 12/23/2014). Spain Headline Consumer Price Index (CPI) and CPI Ex. Energy and Fresh Food, January 2013 - December 2014.

Yes, if deflation results from a bank panic or major monetary error (think: the Great Depression, in which money supply and prices cratered), then it is probably bad. But deflation may be good if it's the result of innovation spurring fast-rising supply. That's what happened in the Industrial Revolution, when prices mildly dipped and languished as supply growth outstripped demand. If that sounds familiar to you recently, it's because that is the exact factor weighing on energy prices today.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] If you follow that link, you'll find that eurozone deflation fears are more than a year old.

[ii] Lithuania just joined January 1. The others are Belgium, Germany, Estonia, Ireland, Greece, Spain, France, Italy, Cyprus, Latvia, Luxembourg, Malta, the Netherlands, Austria, Portugal, Slovenia, Slovakia and Finland.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today