Personal Wealth Management / Market Analysis

Record Speed to Record Highs

With the S&P 500 hitting a new all-time high including dividends and global stocks not far behind, what should investors make of markets’ fast recovery?

On Monday, the S&P 500 Total Return Index closed at 6895. For those scoring at home, that is a new all-time high for the S&P 500 when including reinvested dividends—officially rendering the rise since March 23 a new bull market. It is a notable milestone with much for market historians to mull over, but for investors, it likely means little for stocks going forward.

Official back-to-breakeven dating will use the S&P 500 price index, whose daily dataset stretches back more than 60 years before daily total return data begin. Since that index doesn’t include dividends, we don’t think it represents investors’ full experience—hence why we are focusing on the total return index. But the price index isn’t far from breakeven. As of Tuesday’s close, it was just -1.5% below its prior bull market high.[i] Looking globally, the MSCI World is about -2.1% off its February 19 high.[ii]

Now, we aren’t predicting when the S&P 500 price index will hit its prior peak, although it is flirting with it on an intraday basis as we finalize this Wednesday morning. For all we know, a correction (sharp, sentiment-driven drop of -10% to -20% or so) could start tomorrow. Those start at any time, for any or no reason, and if one started this week, it would be the sort of quirky timing stocks enjoy—the Great Humiliator at work. But that is unknowable, in our view. Even then, with only four and a half(ish) months elapsed since the low, there is plenty of room for this to be the fastest return to breakeven ever—fitting for the fastest, shortest bear market ever.

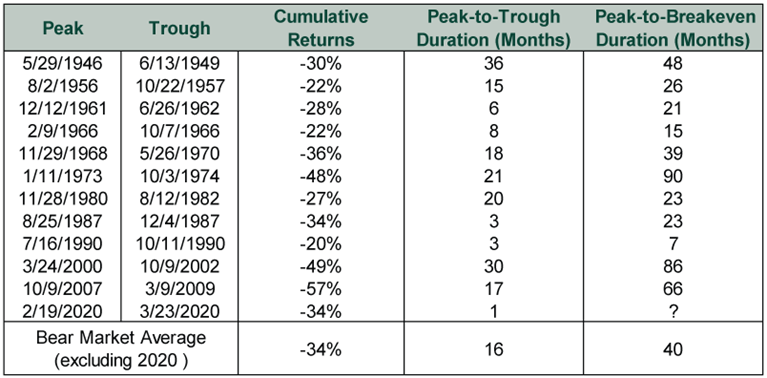

Exhibit 1: S&P 500 Bear Markets in Postwar Era

Source: Global Financial Data and FactSet, as of 8/11/2020. S&P 500 Index Price Level from 5/29/1946 – 8/10/2020.

This speaks to a point we have frequently made about 2020’s bear market and what it means for sector and style leadership in a new bull market. In our view, this past bear market behaved much more like a correction than a typical bear market. It was a full-fledged bear market in magnitude and had a fundamental cause, but it was short and sharp. It lacked a slow-rolling top, and—crucially—it didn’t last long enough for value stocks to get their typical panicky pounding. That means they weren’t set up to bounce disproportionately in the new bull market—and they haven’t. Sector leadership hasn’t changed, either. The sectors and styles leading into a correction typically continue doing so when the correction ends—and, a few brief blips aside, large, growth-oriented companies haven’t relinquished their leadership. Tech and Tech-like companies led as the last bull market matured, led during the bear market, and have outperformed handsomely during the recovery. We doubt these trends change in the foreseeable future.

While we think the recovery’s speed and other characteristics are noteworthy from a style and portfolio construction standpoint, we don’t think they predict returns from here—for better or worse. Though we believe the most likely scenario is that global stocks end the year positive, this doesn’t mean returns will continue at a similar pace as the past four months for the rest of 2020. Bull markets usually slow down after the initial burst, and it isn’t unusual to get a correction early on. But a sharp return to new lows seems unlikely and, indeed, would be unprecedented. Moreover, that kind of downturn wouldn’t happen for any old reason. In our view, it would require some new, huge negative that stocks haven’t yet reckoned with. While possible, successful long-term investing is based on probabilities, not possibilities.

Absent a wallop, sentiment suggests to us this bull market has a long way to run, as we seem something like 10,000 miles from euphoria. Investors remain broadly pessimistic. Headlines warn stocks have come too far, too fast and are disconnected from reality in a “false recovery.” Worries about a “second shoe to drop”—e.g., a new COVID outbreak leading to another global economic shutdown—persist. Not to mention other big fears, including inflation, bankruptcies, high unemployment, and all the other hallmark worries as stocks recover.

When these worries linger as stocks approach breakeven, it usually triggers a condition we call breakevenitis—investors’ urge to sell when stocks approach pre-bear market levels out of fear of a renewed drop and losses. Selling at the prior peak seems like a sensible way to avoid locking in past bear market declines and avoid a second round of pain: a win-win! However, we think this is a mistake, and history shows it can be a costly one.

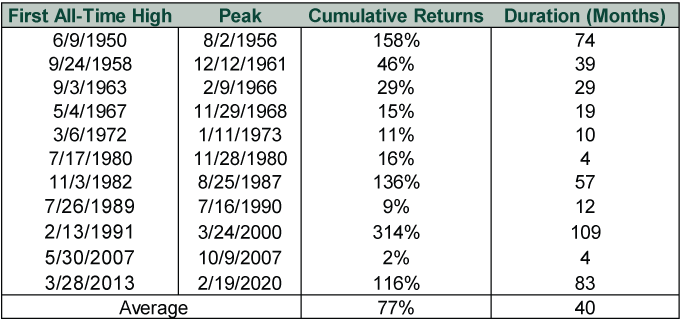

Exhibit 2: S&P 500 Returns From First All-Time High to Next Peak, 1950 – 2020

Source: Global Financial Data and FactSet, as of 8/12/2020. S&P 500 Index Price Level from 5/29/1946 – 8/11/2020.

There is nothing magical about breakeven. The first all-time high in a bull market is usually one of many before the eventual peak. The fears splashed across headlines daily aren’t reasons to sell, in our view—they are all too widely discussed. Investors have been mulling over them for weeks or months. We strongly suspect they will go down in history as the foundational bricks in this bull market’s proverbial wall of worry. So if you have hung on so far, through the big drop and fast bounce, you have done the hardest part. Now it is time to stay cool and let a new bull market reward you.

[i] Source: FactSet, as of 8/12/2020. S&P 500 Price Index, 2/19/2020 – 8/11/2020.

[ii] Source: Ibid. MSCI World Index return with net dividends, 2/19/2020 – 8/11/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08 -

Market Analysis On the Iran Flare Up2026-07-08

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-07-07

2026-07-07 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 29 - July 32026-07-07

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today