Personal Wealth Management / Market Analysis

Resetting Expectations

There are two ways to think about recent market negativity—forward or backward. Let’s consider both.

A bullish camp expecting above-average returns in 2011. A bearish camp expecting the exact opposite. Few in the middle.

That was the sentiment landscape as 2011 began, and we felt a tug-of-war between bulls and bears would likely result in a volatile year lacking big directional moves by year end—with a possible correction along the way.

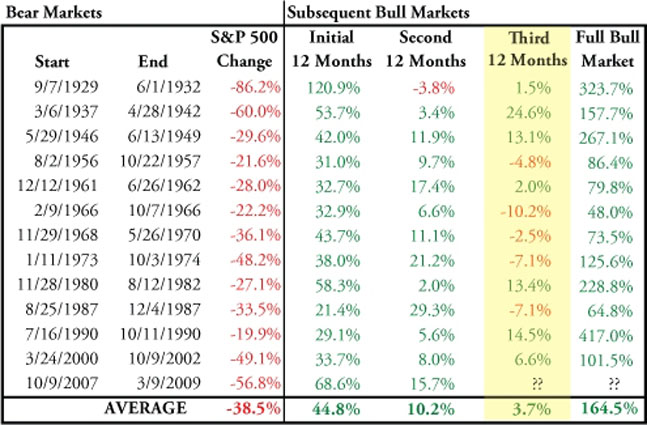

What we’ve seen thus far fits that description relatively well. And historically, that’s not unusual in the third 12 months from a bull market’s start—as shown in the table.

Bull Market Third Years Are Typically Not Extreme

Source: Global Financial Data, Inc. S&P 500 Index Price Returns.

Corrections (which we feel recent market negativity likely represents) can be very painful to live through. But you do have a choice of how you view them: With an eye to the future or the recent past. Many think corrections are uniformly bad, but the fact is if you look ahead, corrections can be seen as a healthy feature of a bull market—shifting sentiment downward. Remember: It isn’t just what reality is that matters in investing. How widely reality is appreciated by investors is also important. Given current dour correction sentiment and some recent economic data missing expectations, many economists and analystshave lowered their estimates of future economic growth—essentially extrapolating recent economic data trends forward.

Many seemingly take this as a negative—and if you’re focusing exclusively in the now or recent past, it’s easy to see it that way. But if you cast your eyes to the future, lowered expectations represent an easier hurdle for data to clear—a potential bullish driver for stocks. After all, if every investor expected exactly what data ultimately showed, there’d be little surprise (positive or negative) and investors would likely already be perfectly positioned. These lowered expectations and dour sentiment could mean stocks are underpriced based on views today, which are heavily influenced by the very recent past. While we continue to believe 2011 is unlikely to show big up or down returns, and we’re not yet ready to make a 2012 forecast, ratcheting down of sentiment is an incremental positive driver for the next 12 to 18 months or so.

Other positive fundamental drivers that can impact stocks over the next 12 months? We’ve discussed Q2 2011’s earnings season before, like here. But beyond the fact rising revenues and earnings are unlikely to signal an economy in poor health, when you combine the results with recent share price weakness, you get another effect: Valuation compression. Essentially, in recent weeks, stocks have gotten cheaper from both price movement and quarterly results. And while recession fears have grown in recent weeks, economic data show continuing growth—albeit at a moderate rate. (Examples from this week include better-than-expected US durable goods data, increased US rail freight trafficand eurozone PMIthat beat estimates.) 2012 also marks an election year—generally speaking, good for stocks. Combine that with extant political gridlock in the US and elsewhere, and the likelihood of radical legislative change seems low. All strong positives, on top of many others, indicating a likely continuation of bull market ahead. Current correction sentiment just doesn’t seem to appreciate that much, which is what you want—unless you’re planning to be short equities in 2012.

Of course, it’s still early and much could change between now and when our 2012 forecast is made. Importantly, these positives must be weighed against other materially new negative drivers as they crop up. And yes, you can bet fears of last year, which followed us into this year, will probably continue haunting investors next year—PIIGS, hyperbolic election claptrap and proclamations about some version of economic woe. There are existing negatives today, but they’re mostly neither new nor powerful enough (absent some major change) to derail the current bull market. Even older ghosts, like inflation, could crop up. But as we write this, the current dour sentiment and potentially muted full-year 2011 returns don’t appear to bode ill for 2012.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, US Q2 GDP, Eurozone Inflation

2026-07-27

2026-07-27 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 20 - July 242026-07-27

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today