Personal Wealth Management / Market Analysis

Sales, Not Surveys

July's UK retail sales report is yet more evidence sentiment surveys aren't as predictive as many think.

Something funny happened along the way from UK consumer confidence's post-Brexit plunge to the much-predicted consumer spending shock: Consumers spent. A lot. While it's just one month (and an incomplete look at total household spending), July's smashing retail sales are a sign the UK recession many predicted is, so far, nowhere to be seen.

UK July retail sales volumes jumped 1.4% m/m, smashing estimates of 0.2%. This echoes a similar British Retail Consortium-KPMG survey, released August 9, which estimated July retail sales climbed 1.9% y/y, the fastest rate in six months. Per the official report, demand for discretionary items was especially strong. Sales of footwear and leather surged 13.1% m/m, clothing rose 2.5%, and watches and jewelry rose 3.1%. Meanwhile, sales of household goods inched up just 0.4%-folks weren't just stocking up on paper towels and toothpaste. Some say shoppers merely responded to deep discounts, and maybe promotions did lure people to the shops. But they still spent more overall: Sales values rose 1.7%. Others say the weak pound likely drove foreign tourists to go on a shopping spree, artificially boosting sales. While this is true to some extent, it's a stretch to say foreign demand is the sole reason sales rose, and there is nothing "artificial" about a tourism boost.

July is just one month, and this doesn't necessarily mean Brexit dread won't kill the UK economy's animal spirits in the future, particularly if exit negotiations go south. But it does underscore a key point: Nothing fundamentally changed with the vote to make an economic slowdown necessary or automatic.

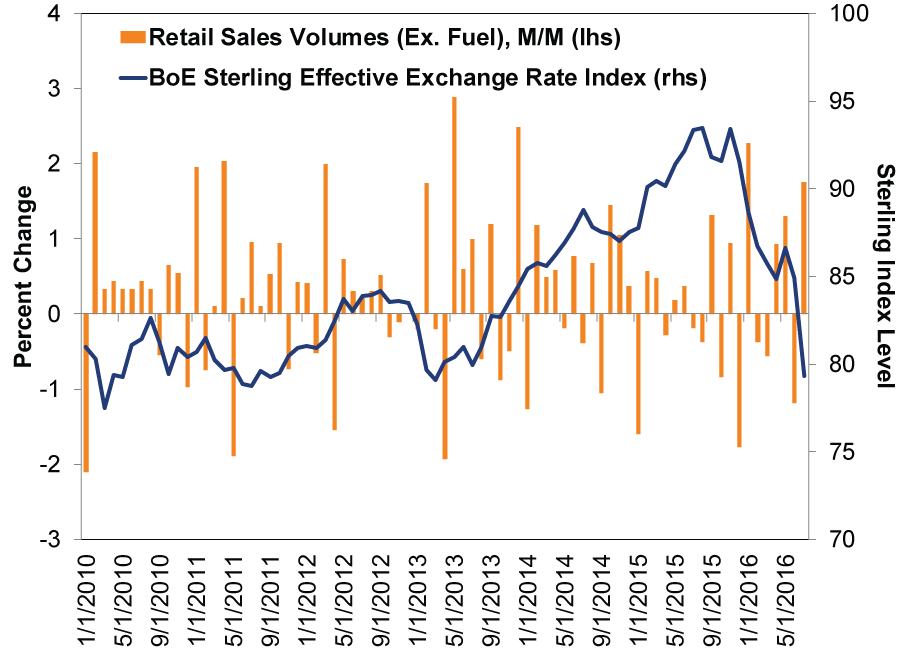

Some suggest spending was pulled forward because the weak pound will cause inflation to spike, encouraging consumers to snap up items before they become more expensive. But this is pure speculation. It's based on a slew of questionable assumptions, including that the pound will remain weak for some time. Maybe it will and maybe it won't. Currency markets are notoriously hard to forecast reliably. Even if Sterling does stay this weak, inflation won't necessarily rise, nor will shoppers automatically struggle. Against a broad basket of currencies, the pound was similarly weak in early 2013, while inflation stayed in check. Prices spiked in 2011, when Sterling was also around present levels, but a VAT hike bears most of the blame. Notably, on both occasions, sales didn't suffer-their choppy uptrend continued.

Exhibit 1: A Weak Pound Doesn't Crimp Retail Sales

Source: FactSet, as of 8/22/2016. Bank of England Sterling Effective Exchange Rate Index and Retail Sales (Excluding Fuel), January 2010 - July 2016.

Same goes for the period surrounding Black Wednesday. Sterling plunged, but so did inflation, and sales were overall fine.

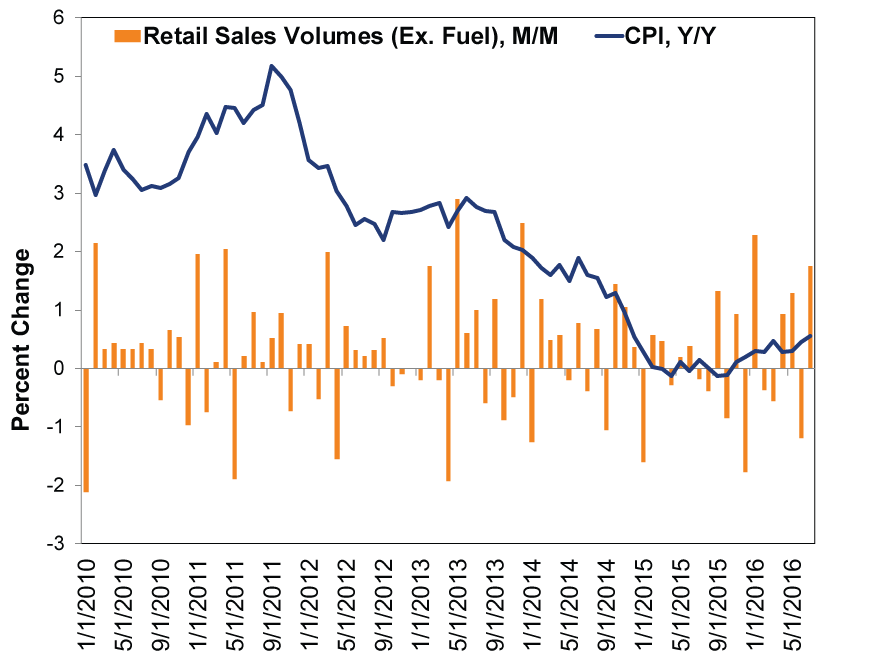

Exhibit 2: Nor Does Moderately Rising Inflation

Source: FactSet, as of 8/22/2016. Consumer Price Index and Retail Sales (Excluding Fuel), January 2010 - July 2016.

While the Brexit vote didn't alter Britain's economic fundamentals, some say the real risk was a sentiment-driven economic shock. Even if nothing fundamentally changed, folks feared, consumers would freeze, scared of the unknown, and save their pennies. The GfK Consumer Confidence Index plunged after the vote, supposedly confirming this risk. Yet as often happens, the survey wasn't predictive. Respondents said one thing, then did another. This isn't surprising to us. These surveys have never been predictive. They capture how folks feel at a given moment, which is often based on what they've read in their morning paper or seen on TV-not to mention their general mood, which has all manner of inputs. It's actually quite normal for people to tell pollsters they feel gloomy, then go out and lift their spirits with a little retail therapy. As Exhibit 3 shows, confidence surveys and actual sales often move in opposite directions in a given month.

Exhibit 3: UK Consumer Confidence and Retail Sales Often Don't Move in Lockstep

Source: FactSet and Office of National Statistics, as of 8/19/2016. GfK Consumer Confidence Index and Retail Sales Volumes, June 2009 - July 2016.

While it's entirely possible sentiment could take a toll later, you can't predict that. Emotions are too volatile. Fundamentals, however, don't indicate a recession looms. Money supply and bank lending are growing, and UK stocks are making new highs after briefly dipping immediately following the June 23 vote. Renewed quantitative easing and the flatter yield curve are headwinds, but the UK survived a much larger, longer round of QE from 2009 through 2012. The yield curve is flatter now than then, but flat yield curves aren't recessionary. Slow-growthy, perhaps, but an inverted yield curve is the true negative. The UK's yield curve is presently not inverted.

Whether the UK slows a bit or not, however, it shouldn't much matter to global markets-of which UK stocks comprise about 7.0%.[i] Japan, whose economy is larger and comprises 8.8% of global market capitalization, has endured three recessions (defined as two consecutive quarters of negative GDP) since this global bull market began on 3/9/2009.[ii] World stocks also survived some extra-choppy UK growth from 2010-2012. There are always pockets of strength and weakness, but on balance, the world is healthy and growing-good enough to surpass investors' low expectations.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

-

Expert Commentary Ken Fisher on Crypto, Inflation, AI Bubble and Annuities

2026-06-16

2026-06-16 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 8 - June 122026-06-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today