Personal Wealth Management / Market Analysis

Scary Stories That Weren’t

The media skipped plenty of opportunities to spread fear and gloom Monday-a telling sign of sentiment.

Here is a question we get all the time: How do you measure investor sentiment? After all, we don't have much use for consumer confidence surveys or polls, and we aren't shy about this. They can help, along with valuations and ETF and mutual fund flows, but feelings are squishy and qualitative-by definition difficult to quantify. So we make qualitative assessments, too, and studying the media's reaction to certain events is a great way to do this. Why media? They both reflect and influence mass sentiment. And if Monday's headlines are any indication, sentiment is getting warmer, because headlines greeted a slew of "bad" news in (rationally) optimistic fashion. Here is a roundup of all the things people aren't panicking about.[i]

Black Friday Was a Dud

Yes, Thanksgiving weekend retail sales fell 11% from 2013, and the average shopper spent 6.4% less. If this were 2009, 2010, 2011 or even 2012, we suspect headlines would have warned of crashing holiday sales and a consumer spending implosion. Instead, most outlets pointed out the obvious: Most "Black Friday" deals started in early November, lessening the door-buster urgency among turkey-filled shoppers at 4 AM on Friday.[ii] Consumers aren't tapped-retailers just started competing on timing. Industry groups aren't rushing to lower their holiday or full-year retail sales forecasts. No myopic pessimism. Seems about right to us.

Japan Gets Downgraded. World Yawns.

True confession: We are sort of weird, so the media's big "so what" to news of Japan's downgrade makes us long for the days when a lower credit rating in the world's number three economy would have really meant something-we had some great puns all ready to go.[iii] Alas, however, this isn't January 2012, when S&P's downgrading France and Austria meant the eurozone crisis "returned with a vengeance." Or February 2013, when Moody's UK downgrade was a "serious blow" and a "stark reminder" of Britain's "debt problems." Japan is bigger than all of them, and its debt is 245% of GDP.[iv] Really, this is ripe for some irrational debt crisis panic. And yet, crickets. Most realize Japan's long-term interest rates are basically the world's lowest (and likely to stay there for the foreseeable future, thanks to the BoJ)-folks are looking past (backward-looking) ratings agency decisions and leaning on the market to weigh things. Rational! Japan can afford its debt, and rates would need to rise to nosebleed levels and stay there before things start going Greek. With demand high and inflation still at rock-bottom levels (despite the BoJ's many efforts), rates don't seem set to rise any time soon.

Russia's Currency Non-Crisis

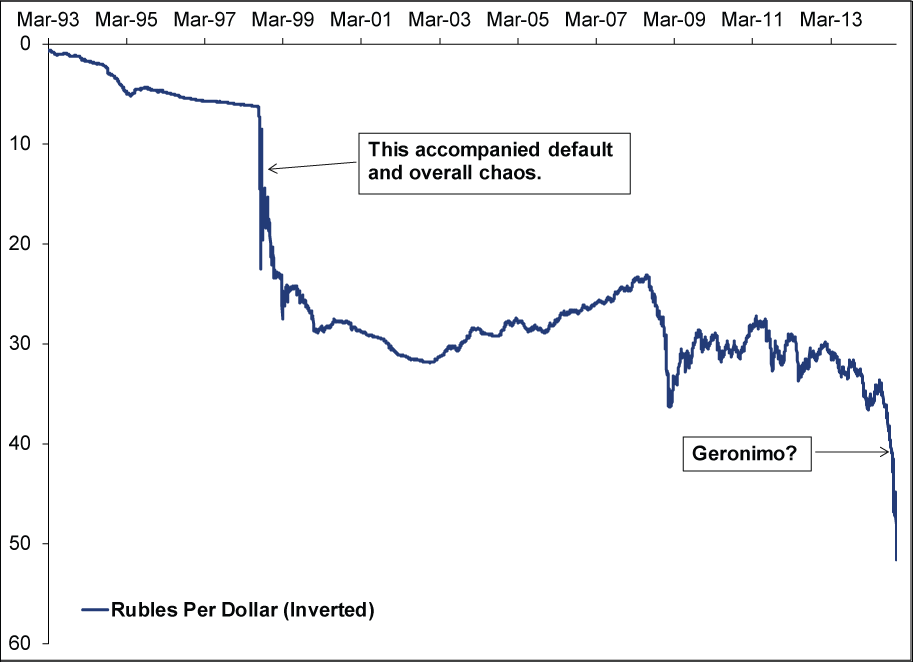

The Russian ruble took its biggest one-day slide since 1998 on Monday, losing 6.5% vs. the dollar intraday, piling on last week's 9.3% decline. The last time the ruble went into freefall, the Motherland had a full-blown currency crisis and default. A hedge fund called Long-Term Capital Management imploded and got a bailout. Global markets had a steep correction. So we thought for sure we'd see some "Uh-Oh Get Ready for Russian Ruble Crisis 2.0" fear-mongering. Especially with oil prices tanking, threatening the last functioning leg of Russia's economy, the energy sector. Yet, nobody went there! We couldn't find anyone publishing charts like this:

Exhibit 1: The Ruble Turns to Rubble

Source: FactSet, as of 12/1/2014. RUB/USD Spot Exchange Rate (Mid), 3/31/1993 - 12/1/2014.

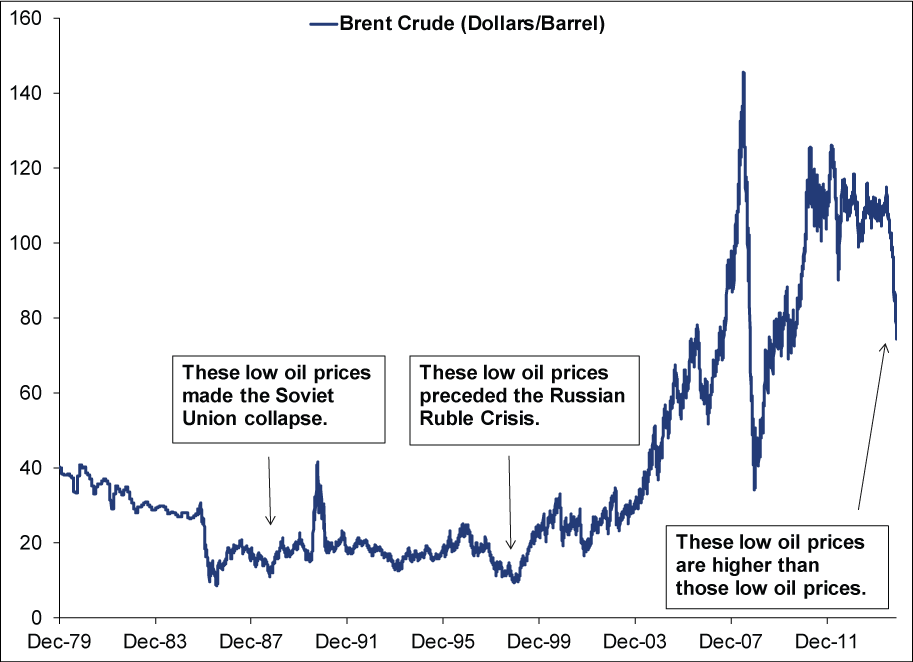

Which means there was really no need for us to counter with charts like this to ease fears about a country whose energy sector generates a big chunk of state revenues:

Exhibit 2: A Brief Look at Russian History and Oil Prices

Source: FactSet, as of 12/1/2014. Brent Crude oil prices (USD/Barrel), 12/31/1979 - 11/30/2014. Data are monthly through 9/30/1985, daily thereafter.

Exhibit 2 largely shows why the lack of Russian doomsday fears is rational. Also helping is the fact Russia had $428.6 billion in foreign exchange reserves at last count, which exceeds the $132 billion in foreign debt (public and private) due by the end of 2015, perhaps helping blunt the impact of sanctions.[v] Russia probably has a rough time for the foreseeable future, but its economic troubles are widely known, and headlines have long since realized the world can cope just fine.

Some Manufacturing Numbers Went Down

Finally, a number of manufacturing purchasing managers' indexes (PMI) hit Monday, showing how many businesses in a given area reported rising activity. Some of them weakened but remained above 50 (considered the dividing line between contraction and growth), which headlines sensibly noticed. The US ISM PMI's fall from 59 to 58.7 in November was "still healthy." China's official PMI slowed from 50.8 and 50.3 and the HSBC PMI hit an eight-month low of 50, but hard-landing fears didn't resurge-most acknowledged a big pickup was unlikely so soon after last month's rate cut, and most full-year GDP forecasts remain above 7%. Folks seem to have accepted a gradual slowdown. Just as they've accepted the weaker PMIs in the eurozone, which many claim signal more sluggish GDP growth in Q4-yes, still growth! Not a triple dip recession. It seems folks are finally hip to the fact contracting PMIs don't necessarily mean contracting GDP-a point we've often made, considering PMIs tell you the broad percentage of firms growing, but not the magnitude of that growth. (See France with any questions.)

Parting Thoughts

So yes, sentiment is decidedly brighter today than it was a few months ago, a sign this bull market is moving right along. We often quote Sir John Templeton's famous line about how bull markets start when sentiment is in the dumps, grow and thrive as sentiment gradually improves, then roll over when folks are bouncing off the walls and dancing on the ceiling.[vi] We're in the gradual improvement stage and quite a ways off from party like it's 1999-a sweet spot where ever-more optimistic investors become steadily more willing to bid stocks up. Add in a global economy that's poised to keep growing and a benign political environment, and stocks should have plenty going for them. Enjoy the ride (and your break from media fear-mongering).

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] We are sorry this thesis isn't more exciting.

[ii] Also people just got tired of risking getting trampled to death.

[iii] And we have decided to save them.

[iv] Gross public debt. Net debt-debt owned by the government-is lower. It's lower still once you factor out the massive holdings of the BoJ and state-owned Japan Post bank.

[v] Most big Russian banks and energy firms remain barred from global capital markets.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History Six Years On, Lessons From the COVID-Lockdown Low Endure2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today