Personal Wealth Management / Politics

SCOTUS Rules

The Supreme Court declared 2010’s health care reform bill constitutional on Thursday—what does the decision mean for stocks?

On Thursday, in a widely watched decision regarding 2010’s health care reform bill, the Supreme Court affirmed the constitutionality of the Affordable Care Act (ACA), including the most contentious component—the requirement for all citizens to maintain health insurance (the so-called individual mandate). While this ruling no doubt rekindles some political angst, we doubt it has any immediate major market or economic fallout.

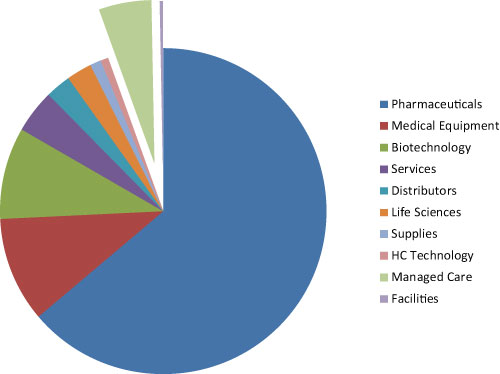

As with any new legislation, both winners and losers are created under the ACA. And in our view, the bill impacts most a relatively small portion of the Health Care sector. Nearly 85% of the sector (as measured by market capitalization of the MSCI World Health Care Index) is Pharmaceuticals, Biotechnology and Medical Equipment firms (see Exhibit 1). These firms will indeed be faced with additional taxes or fees. However, for Pharmaceuticals firms (the largest part of the sector by far), the fee is relatively small—well under 1% industry revenue.

Pharmaceutical firms will no doubt attempt to safeguard profitability by passing increased costs along to consumers, since demand for their goods is overall fairly inelastic. Consumers may not cheer that news, but, on the flip side, it’s an open question how effectively firms can pass along those costs, considering there’s typically a third-party—the insurance firm—between consumers and producers. Still, in our view, it’s a relatively small fee that gets shared roughly by firms and their customers. It’s not ideal, but it’s not disaster.

Exhibit 1: MSCI World Health Care Sector Sub-Industries

Source: Thomson Reuters.

Industries that seem most impacted by the legislation—Hospitals and Managed Care—are a much smaller portion of the sector. What’s more, for these industries, positive and negative impacts may well largely counterbalance. Managed Care firms may benefit from insurance expansion, but it’s likely these potential gains are mostly offset by regulation, like bans on lifetime limits and pre-existing conditions, industry fees and mandated profit margins. Facilities (Hospitals)—a typically low-margin industry—will seemingly benefit more: Patient volume could very well rise, but fewer uninsured patients could also mean reduced unpaid expenses.

A key factor many overlook is the impact of ACA is mostly limited to the US. The fastest growing market for Health Care is Emerging Markets. Expansion in those markets likely doesn’t benefit US-based Facilities and Managed Care firms, but it does provide huge opportunities for Pharmaceuticals, Biotechnology and Equipment firms.

What’s more, this law has been openly and hotly debated since it passed in 2010 and even before—which likely means decisions investors might make regarding the sector based on this law have already largely been made. We caution against putting too much credence in a single day’s market action—but it’s worth noting that following the decision, stocks eventually rallied significantly (over a full percent) to end the day down slightly.

Ultimately, in our view, market impact will likely be more muted than widely feared. But we do anticipate heated rhetoric—from the media and politicians. (And the implications outside Health Care will also undoubtedly be hotly debated.) Politicians—on both sides—will campaign hard on the bill, and Republicans have already indicated they’ll vote on a full repeal in just a few weeks. A full repeal won’t pass the Senate, but the composition of Congress likely changes some in November. A full repeal even then is unlikely—Republicans must take the White House and get a filibuster-proof Senate majority. The White House is a possibility, but a 60-seat majority is a major stretch. Still, it’s certainly possible some portions of the bill are altered down the road as power keeps shifting in Congress—creating more winners and losers.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today