Personal Wealth Management / Market Analysis

Sentiment Check-In: January Effect Edition

The lack of “January Effect” enthusiasm this year is telling.

Remember the days when everyone believed in the January Effect—the notion that January foretells the year’s stock returns? It wasn’t that long ago. Since this bull market began in 2009, any time stocks sank in January, calendar-watchers would fret a negative full year. So in the name of intellectual consistency, you might expect them to be similarly positive about 2018 returns as one of the best Januarys on record nears its close. However, you would be wrong. A Google News search on “January Effect” turns up precious few hits, and market luminaries warn the party won’t last. On the one hand, since we think seasonal patterns are hogwash, we find the lack of January Effect commentary refreshing—one less myth for us to debunk this year. But the void is also noteworthy, as it is a sign recent returns haven’t made investors euphoric—one indication, in our view, that stocks aren’t peaking as January closes.

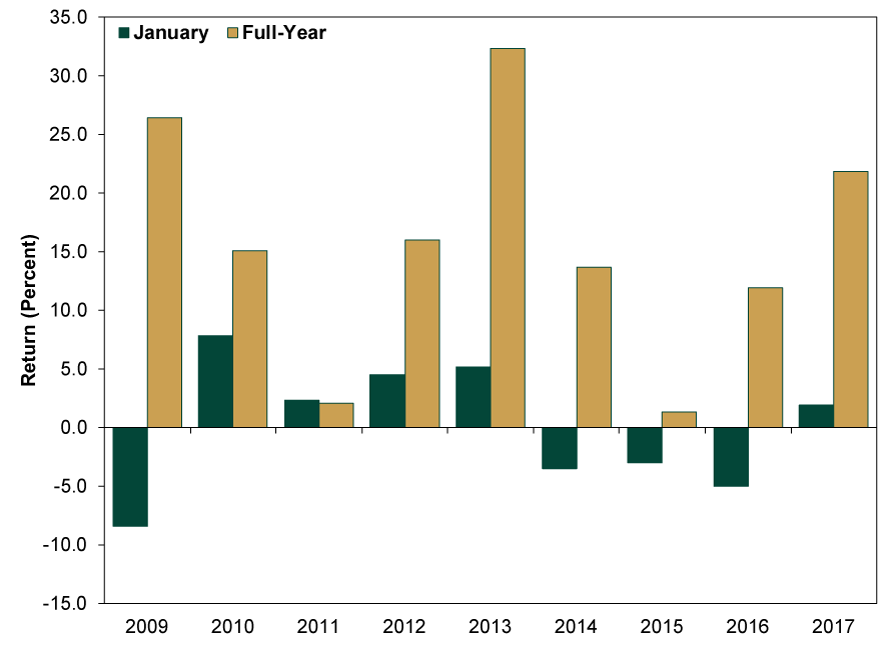

When looking for January Effect commentary this morning, we found only three notable recent mentions on mainstream websites. One, on Bloomberg, oddly described the January Effect as “a tendency to see gains early in the year.” Another, in Britain’s Telegraph, warned of reasons why investors shouldn’t rely on it this year—in other words, don’t expect a great 2018 just because January started with a bang. Commentary on The Motley Fool took a more measured approach with a rational debunking of the overall myth. No one, as far as we can see, extrapolated January forward as a preview of an awesome year. Which, as Exhibit 1 shows, is logical—there is no actual January Effect.

Exhibit 1: The January Ineffect During This Bull Market

Source: FactSet, as of 1/29/2018. S&P 500 total return in January and the full calendar year, 2009 – 2017.

We might not even have bothered writing this up if not for a semi-related article in Monday’s Wall Street Journal, which highlighted this strong January and showed how, instead of inciting joy, it fueled angst:

The gains have also put some investors on edge, intensifying analysts’ concerns about the rising price of buying into a bull market almost nine years old. The rallies have also drawn comparisons to the 2000 Nasdaq peak, when a mania for technology stocks drove the index to a level that it wouldn’t recapture for more than a dozen years.

Then it went on to cite some professional investors who are very worried about stocks rising too far, too fast, warning valuations and equity fund flows are too high. The Washington Post also got in on the fun Monday, with similar warnings about “stretched” valuations. We saw similar after the Dow crossed 26,000 halfway through the month. And not to be outdone, Barrons’s warned on Friday that the ongoing rally “makes the dot-com bubble look sane.”

Naturally, this made us want to dig up some actual stories from January 2000, a few months before the Tech Bubble peaked, to see just how insane it was and whether today really dwarfs that. Most people today remember the dot-com frenzy in abstract terms and soundbites like Alan Greenspan’s infamous “irrational exuberance” speech (actually from December 1996, over three years before the peak and well before euphoria arrived). The infamous BusinessWeek “The New Economy” issue also leaps to mind, as does CNN’s debate on whether “boom and bust” had been replaced by a new era of “boom without end.” But those are mere snapshots of the day’s euphoria. Smaller examples peppered financial media daily, and we uncovered several when searching for mentions of “stock market” in The New York Times during January 2000. Not every single article was over-the-top bullish. But the coverage often captured the mood of the day. One of columnist Gretchen Morgenson’s pieces is a great example, highlighting participants in an investing online chat room who advocated piling into bankrupt companies like Loehmann’s and Fruit of the Loom:

Inexplicably, the chatterers seem to view these companies’ depressed shares as bets worth taking. One Fruit of the Loom fan posted this message on a Yahoo board last week: “FTL's earnings were upgraded by First Call to less of a loss, this makes me believe that we have nowhere to go but up from here.” …

In a typical revamping, stockholders wind up with nothing. Only the creditors -- the banks, bondholders, preferred stockholders and so on -- get anything back.

The Internet chat reveals that some of the investors buying into these companies know little about the reorganization process. A message posted on Yahoo's Fruit of the Loom board said: “A company has value until they tell the public there's no value.” Another stated flatly that a bankruptcy judge could wipe out a company's debt and leave the equity alone, a ruling that would be as likely as a snowball surviving Dante's Inferno.

And then there was the matter of the AOL/Time Warner merger, which prompted illogical cheer. Also from The New York Times:

This being the Internet age, most analysts think that the new company's benefits to shareholders will be immediate and that the deal will justify even higher valuations among already manic Web stocks.

“Just as Home Box Office redefined the cable industry and provided the catalyst that made cable companies go out and offer new services, the combination of Time Warner and AOL should act as a stimulus of the broadband adoption of Internet experiences,” Christopher Dixon, an analyst at Paine Webber in New York, said. “Should that take place, then all the business models of Internet start-ups become accelerated. That results in higher valuations as a whole.” …

So, to Internet enthusiasts, the merger of the nation's leading Internet company with a top media group, which will have a market value of $350 billion, is epochal. It opens wide the door to the Web; many more people will become users at a much faster rate than had previously been estimated. And it places sky-high Internet valuations on what had been an earthbound media company.

Other headlines from the Times machine include “If History Is Any Guide, the Party May Continue,” from January 23, 2000, which argued 1999’s strong Q4 presaged a dynamite 2000. “Surging Profits May Indicate a Longer Life for the Bull Market,” published the day prior, highlighted expectations for 63% growth in Nasdaq stocks’ corporate earnings that year—allegedly justifying the index’s P/E of 125. And “Dot-coms in an Alien Universe,” a rational look at the indiscriminate IPO frenzy, captured just how bizarre the landscape had become:

Once upon a time, fledgling companies relied upon bankers for start-up loans until they had booked enough earnings to justify stock listings. Now, in a superheated investment environment, companies can bypass the banking system altogether, advancing swiftly from conception to a billion-dollar initial public offering in less than a year. These companies then exploit their wildly appreciating shares as currency to take over other companies. At the same time, by dangling stock options, they can lure talented managers from the old economy without paying hefty salaries.

We have leaned heavily on The New York Times because of their user-friendly search engine and robust online archive, but it was like this all over the financial media. And it bears little resemblance to what we see today.

Experience tells us that when euphoria is truly here, few will be worried about high valuations or markets’ reaching milestones with breakneck speed. They will probably also cheer large stock-based mergers like the AOL/Time Warner boondoggle. And they will concoct outlandish reasons stocks can keep rising, maybe forever. Most investors will fear missing out on gains instead of fearing a potential downturn. About the only time investors don’t have fear of heights is when they are happily sitting atop the proverbial wall of worry. Today, folks are still climbing that wall and trembling any time they look down.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today