Personal Wealth Management / Economics

Sentiment’s Goldi-Lockdown

Global growth is accelerating, and inflation isn’t. Investors used to appreciate this, but today’s skeptical crowd sees low inflation as a grizzly prospect.

In days gone by, the following would be good news: Global economies are growing, if not accelerating, and inflation remains tame. In the 1990s, there was a name for this: a Goldilocks economy! Not too hot, not too slow—just right. But these days, dour sentiment has investors worried growth will fall if inflation doesn’t pick up, and soon. Seems like another episode of too-dour sentiment clouding investors’ perceptions—a scenario we think should set up powerful surprise down the road.

Even in far corners of the world, economic growth is spreading. The US has grown for 16 of 17 quarters, accelerating to a healthy 4.1% (seasonally adjusted annualized rate) in Q3. Business investment, construction and factory orders are increasing. Manufacturing and services PMIs, retail sales and corporate profits are also showing strength. The UK resumed growing in earnest last year, avoiding the double- (and triple-) dip recession many feared—and entered 2014 one of the developed world’s leading economies. The eurozone is growing, with even long-suffering Spain and Portugal contributing. China is still moving at a decent clip, and several Emerging Markets are beating expectations, too. Many of the world’s economists expect more to come in 2014, and most Leading Economic Indexes—supported by globally widening rate spreads—agree.

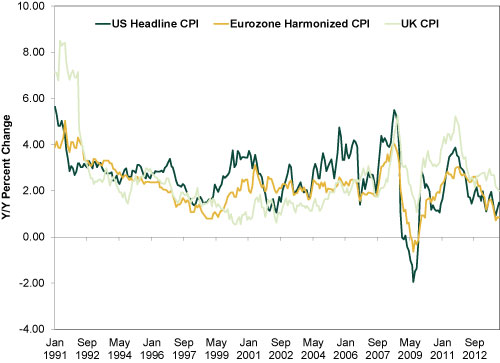

Inflation, meanwhile, is low and falling throughout the developed world. (Exhibit 1)

Exhibit 1: Global Inflation 1991 to 2013

Source: FactSet, as of 1/16/2013.

Ordinarily, folks would be happy to see consumer prices aren’t surging. But these days, folks fear low inflation is a risk to growth. That if it doesn’t rise faster or closer to the target rate, it will spur reduced consumption as consumers and businesses won’t have as much of an incentive to buy things (now!) before prices move up. Many seem to think reducing quantitative easing (QE) increases the risk of a deflationary spiral, based on the mistaken theory reducing the Fed’s bond buying will shrink the money supply.

However, this isn’t how QE and money supply work. Most think a central bank is the only institution that can create money—but that’s false! Central banks, like the Fed, only create M0—all notes, coins and reserves outstanding. This is a small fraction of the total money supply. Banks create the rest, lending off reserves and deposits many times over. In a fractional reserve banking system like ours, this is the source of the majority of the money circulating throughout the economy, measured by M2 (checking deposits, savings accounts, retail money market funds and the like) and M4 (M2 plus commercial paper, institutional money market funds and other highly liquid securities that substitute as money).

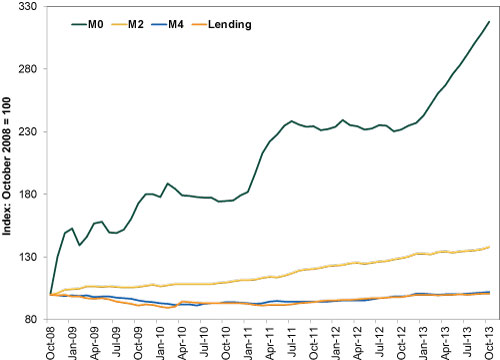

But this process hasn’t much happened in the age of QE. Contrary to popular belief, broad money supply hasn’t skyrocketed! If QE hugely increased the overall money supply, like many assume it has, then M2 and M4 would have grown at least as much as M0, if not exponentially more. But as you can see in Exhibit 2, that isn’t the case.

Exhibit 2: Cumulative M0, M2 and M4 Growth Since QE Began

Source: Federal Reserve Bank of St. Louis and Center for Financial Stability, as of 1/17/2013.

Why? Through QE, the Fed has only created M0 reserves. Bank are supposed to use these as collateral to lend more and boost M2 and M4, but banks aren’t charities—they won’t lend if the profit isn’t worth the risk. QE bond buying flattened long-term rates—banks’ lending revenues—depressing their profit margins on loans and discouraging loan growth. Hence, we’ve had mediocre M2 growth and the slowest M4 growth in modern history.

When QE ends, M0 will grow at a more normal, lower rate—the Fed isn’t yanking reserves, just not creating them at a torrid pace. More importantly, without Fed pressure on long rates, banks’ profitability should rise, encouraging them to lend more—resulting in more M2 and M4, not less. The UK demonstrated this last year, after QE ended there. After four years of weak M4 growth (including a two-year contraction) during QE, UK M4 accelerated. We believe the US likely follows suit.

There is roughly a century of theory and research stressing the growth-enhancing impact of a growing money supply. Yes, it’s inflationary, which should set to rest deflation fears to an extent. But getting inflation isn’t the aim—it’s a result of money supply growth, as, likely, is faster economic growth. And if the economy’s output rises sufficiently, inflation rates may not materially tick up despite a rising money supply.

Inflation is excess cash chasing a scarce goods and services. Putting inflation in the driver’s seat is backwards logic—money supply does much more of the driving, goosing growth and inflation. QE put the US and UK in the slow lane. When QE ended in the UK, growth accelerated. And that’s where we expect the US and world to be as QE ends, rate spreads widen globally and money supplies increase.

This is something folks should cheer, yet many are worried, wringing their hands over “lost decades” of falling prices and stagnating growth. This creates a nice wall of worry for stocks to climb. So let media and punditry wring their hands over such slowly increasing prices. Their dour take doesn’t change the fact a growing economy with slowly increasing prices is still just right.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today