Personal Wealth Management / Market Analysis

Some Solace From a Quantum of Fear

Some say the stronger dollar will cause big problems for Emerging Markets. Are they right?

The most powerful, destructive piece of paper in the world? Photo by Elisabeth Dellinger. And that is her money, so keep your grubby mitts off it.

Here is example #3934823895 of why jargon is evil: "This suggests that more than a quantum of fragility underlies the current elevated mood in financial markets." We pulled the sentence from the Bank for International Settlements' latest quarterly report, where it was tucked at the end of a passage droning on about monetary policy, volatile markets and the strengthening dollar. These all imply "more than a quantum of fragility" in markets today. And we don't know what that means! Because definitions of "quantum" as a noun include all of the following:

- A quantity or amount

- A specified portion

- Something that can be counted or measured

- The smallest amount of a physical quantity that can exist independently, especially a discrete quantity of electromagnetic radiation

- A large quantity

So is there more than a measurable amount of fragility? More than the smallest amount of fragility? More than a large amount of fragility? Who knows! The media all seemed to assume the latter though.[i] They say Emerging Markets are extra-vulnerable and extra-fragile and endanger the world with rapidly rising default risk as the rising dollar makes their foreign currency debt cripplingly expensive. Just like 1997![ii] It's a scary narrative, but one the facts easily disprove. 2014 is not 1997, and the stronger dollar shouldn't take down the world.

For those who aren't familiar with the Asian Currency Crisis of 1997/1998, here is an overly simplified synopsis. Then, most Emerging Markets pegged their currencies to the dollar. With foreign exchange markets relatively stable, their governments and companies were able to borrow heavily and cheaply in dollars, easily financing growth throughout the 1990s. This was called the "Asian miracle," and it was smashing. Until! The yen started weakening against the dollar, making these pegs expensive to maintain. Speculators figured this out, as they usually do[iii], and bet Thailand's central bank wouldn't be able to back the baht. They were right. Thailand tried to defend the peg, using up much of their foreign exchange reserves, but was forced to drop it, devalue, and get an IMF bailout. Indonesia and South Korea suffered similar runs, nearly going bankrupt and requiring a nearly $100 billion IMF bailout. The trauma drove a correction in global stocks from 10/7/1997 to 11/12/1997-and an even bigger one in 1998 as Russia fell.

That, in a nutshell, is what folks fear today. They say low rates drove heavy foreign currency borrowing throughout Emerging Asia and Latin America, and the rising dollar-coupled with slowing growth-could squeeze government and corporate borrowers, putting nearly $10 trillion of external debt[iv] at greater risk of default. And when the Fed hikes rates, hoo boy, look out!

Thing is, there is a big difference[v] between today and 1997. Actually, several big differences. One, most Emerging Markets today have floating currencies. They aren't trying to defend pegs, so in countries whose economies are not one-trick-pony kleptocracies dependent on high oil prices, the risk of sudden devaluation having a crippling impact on foreign debt is small. Two, should countries feel the need to defend their currencies at any time, they have way more firepower today than 17 years ago. Then, countries classified by the IMF as "emerging and developing economies" had a measly $605.2 billion in foreign exchange reserves. Today, they have nearly $8.1 trillion. One of those numbers is over 13 times bigger than the other. To scale that, reserves then were 9.6% of GDP vs. 27.8% today. Countries have largely learned from history and are far more insulated.

Here's another difference:

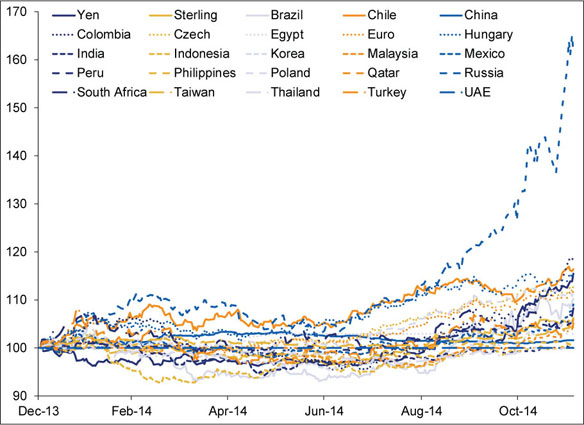

Exhibit 1: Emerging Markets Currencies[vi], Yen and Sterling Vs. the Dollar in 2014

Source: FactSet, as of 12/8/2014. Rising lines means weakening currencies.

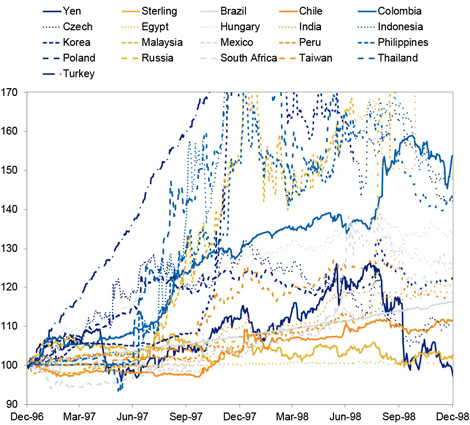

Exhibit 2: Emerging Markets Currencies, Yen and Sterling Vs. the Dollar in 1997 and 1998

Source: FactSet, as of 12/8/2014. Rising lines mean weakening currencies. We cut the Y-axis off at 170 so the scale would match Exhibit 1. Some of these go well over 300.

The point of these mostly isn't to see who's doing what. Rather, it's to see the sheer volume of noise in the 1990s, relative to the largely benign movements today (in places not named Russia). The dollar has risen less than 10% against 15 of 24 EM currencies this year. Most are fairly close to ye olde British pound, and you don't hear anyone warning of a British foreign debt crisis.[vii] The euro is a bit weaker, but you don't hear anyone warning of huge fallout there-heck, most argue a weaker currency would benefit euroland.[viii] Some Latin American nations have weakened more, but they're far from levels of weakness that broke Thailand, Korea and Indonesia in the 1990s. A slow, quite possibly temporary, drift weaker isn't going to break anyone. Currencies would have to plummet to rock-bottom levels and stay there. With growth overall continuing and inbound investment still strong, that is an exceedingly unlikely outcome.

Except in Russia! We wrote about that last week. Here. Nothing has changed. None of this is any good for Russia. But Russia isn't the world. It's 2.8% of global GDP at last count, and other Emerging Markets are in far better shape-more diversified, less Putinized.

If the widely feared foreign debt implosion were a significant risk, we'd expect to have seen vultures circling foreign debt whenever the dollar strengthened. After all, external debt has been rising a heck of a long time! Brazil's has more than doubled since 2001! Korea's, relative to GDP, is about where it was in 1997! We could add a dozen more anecdotal examples! Yet, everyone has largely been fine. It all goes back to floating currencies. Markets know these countries don't depend on artificial exchange rates and central bank intervention. That removes a huge question about long-term viability and source of uncertainty. When markets, not central banks, determine exchange rates, the question of "is this level right" is gone.[ix] Volatility isn't a trigger for a forex reserve bloodbath. Volatility is just volatility.

To us, the biggest lesson here is how pundits continually try to have currency moves both ways. For nearly two years now, we've been told Emerging Asia needs weak currencies to compete with Japan. Welllllll, they have them! Theoretically, they're all winning a currency war! If we could time travel and let folks know this would happen, most would celebrate! Export boost-o-rama! Now pundits have gotten what they wanted and decided it's bad after all. We don't think either point of view is right, and history (and economic results over time) strongly support our beliefs. Truth is, currency moves up or down just don't mean all that much. But that is a boring truth, and who likes boring! So sensational narratives abound, and few spy the contradiction.[x]

Anyway, that's just an observation-we get that the media business is for-profit, and bad news sells. Go, pundits, go! And we kinda enjoy reading all that stuff, because it's darned entertaining! By no means are we suggesting you ignore any of this. Just don't accept sensational storytelling at face value, and remember: Facts often get in the way of a good story, so they are often cherrypicked or omitted.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Whether this is because they are fluent in academese where we are not, or because-in the spirit of William Randolph Hearst and Joseph Pulitzer-they default to the most sensational negative interpretation possible, we have no idea.

[ii] If we were superstitious, we'd be tempted to say we jinxed ourselves last week when we observed no one was saying this. We simply didn't give them enough time. Mea culpa.

[iii] Should you like to learn more, we refer you to the early work of Paul Krugman, who explored this theoretical point in a 1979 paper. While we have some minor quibbles with parts of the argument, it makes the mechanics of these situations crystal clear.

[iv] Debt denominated in currencies other than a country's own.

[v] Dare we say, there is a quantum leap?

[vi] In case you were wondering, the euro is officially an Emerging Markets currency. Because Greece is an Emerging Market. Except, they went backwards to get there, so we call them a Submerging Market.

[vii] Quite right, too. That would be ridiculous.

[viii] An incorrect theory. See this for more.

[ix] China is the obvious exception here, with the renminbi trading within a fixed bandwidth of the US dollar. Most believe it is nowhere near its market exchange rate. But China has nearly $4 trillion in forex reserves at last count. They can likely handle it.

[x] They did the same with housing prices earlier in this expansion. They're doing it with oil prices now.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today