Personal Wealth Management / Financial Planning

Stocks Dig the Long Game

Trust in stocks' resiliency to benefit from their long-term gains.

Let's play a game. Here are three charts with no information. If I only told you each one represented an investment's performance, which investment would you have wanted to own: A, B or C?

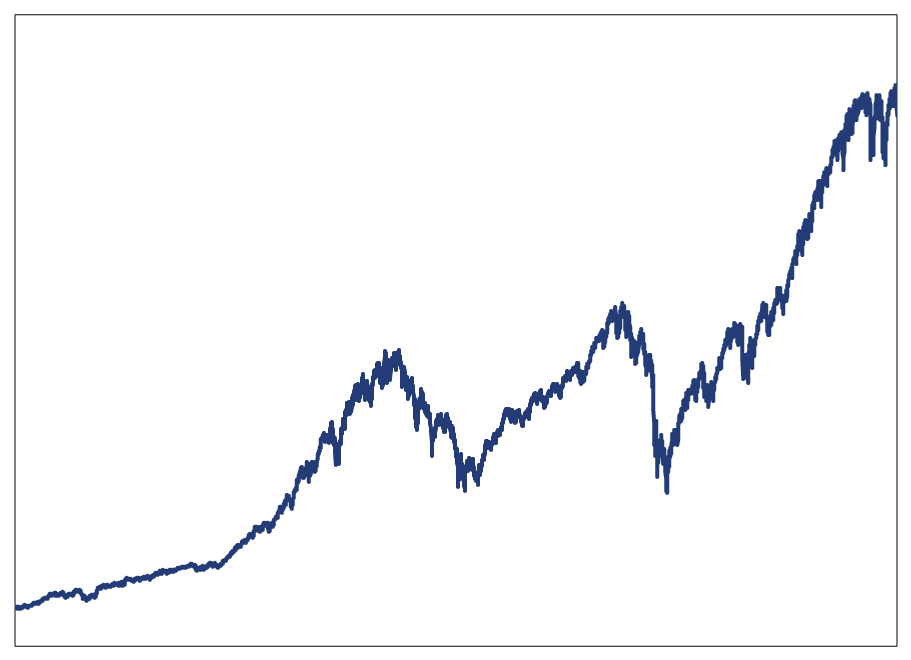

Chart A

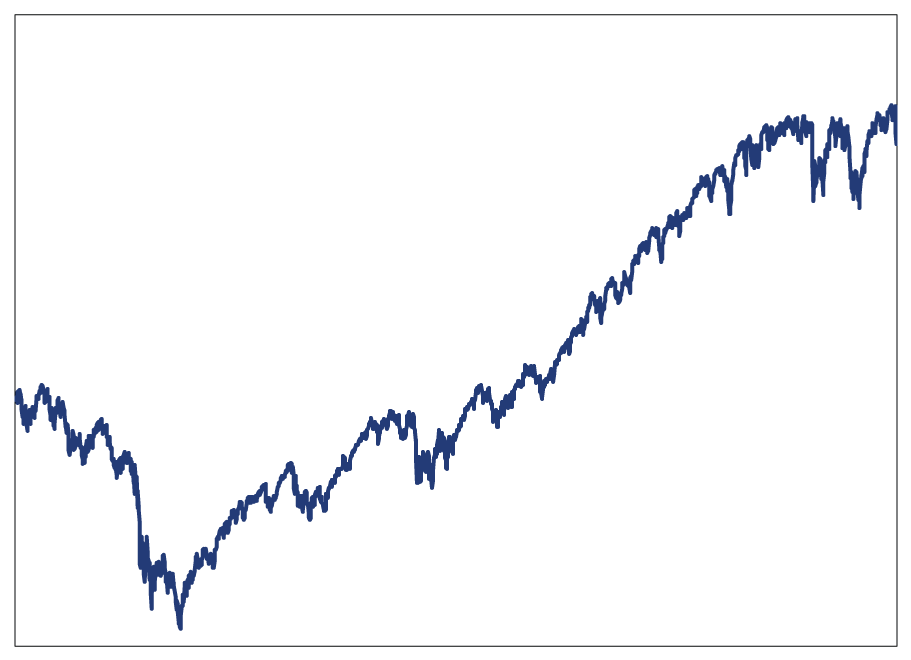

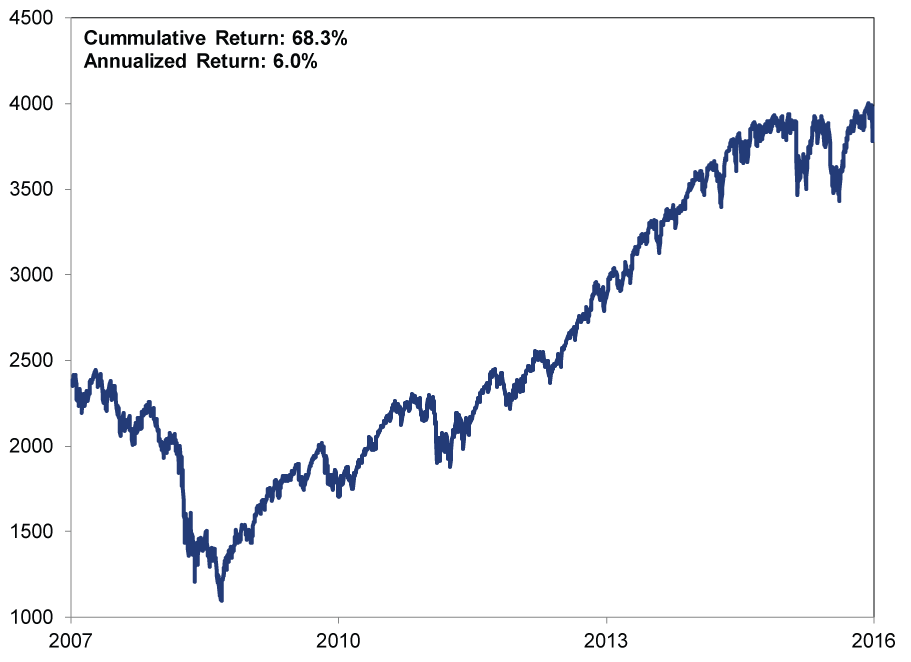

Chart B

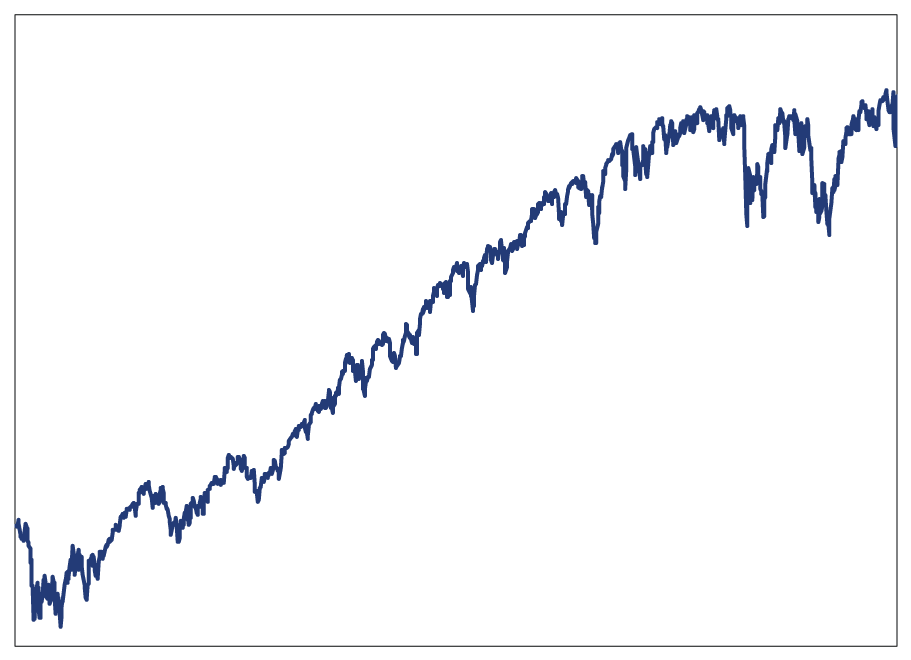

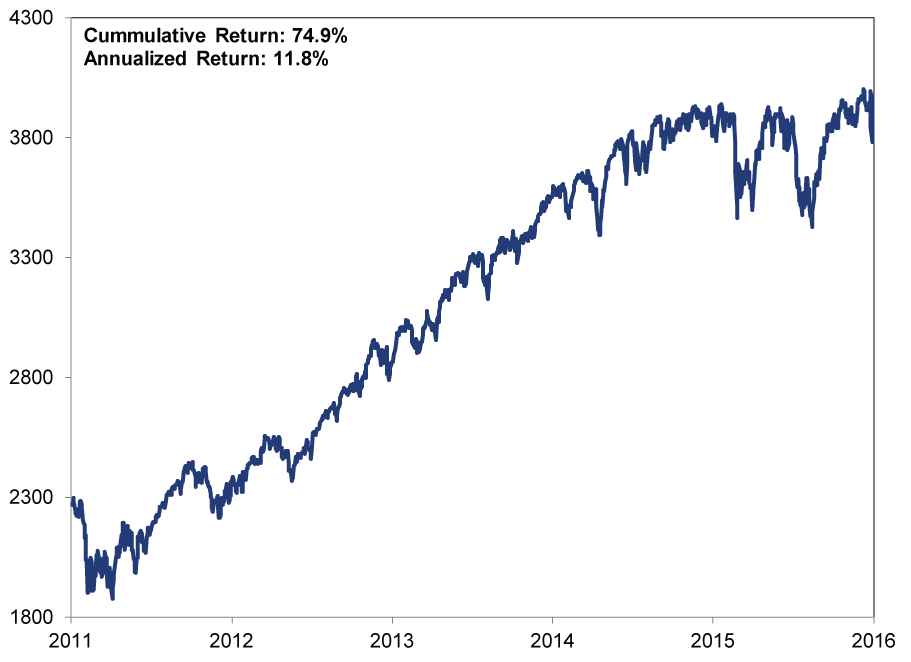

Chart C

Don't overthink this. Unless you enjoy your investment dropping in value, you likely chose Chart C, right? It has mostly risen higher!

All right, ready for the big reveal? All three charts are the S&P 500-just at different points in time (more on this later). Here are the same three charts again, with a little bit more information.

Chart A

Source: Global Financial Data, as of 7/18/2016. S&P 500 Total Return, from 7/1/1988 - 7/1/2016.

Chart B

Source: Global Financial Data, as of 7/18/2016. S&P 500 Total Return, from 7/1/2007 - 7/1/2016.

Chart C

Source: Global Financial Data, as of 7/18/2016. S&P 500 Total Return, from 7/1/2011 - 7/1/2016.

Now, for many investors, the million dollar question is: "How can I avoid those drops and only experience the upside?" My answer: You can't.[i] Or, more specifically, I am not aware of anyone who has an established public record of perfectly timing the market.[ii] However, fret not! You don't have to be a mythical expert market timer to benefit from owning stocks. For long-term, growth-oriented investors, time in the market matters a whole lot more than timing the market and trying to nail those perfect entry and/or exit points.

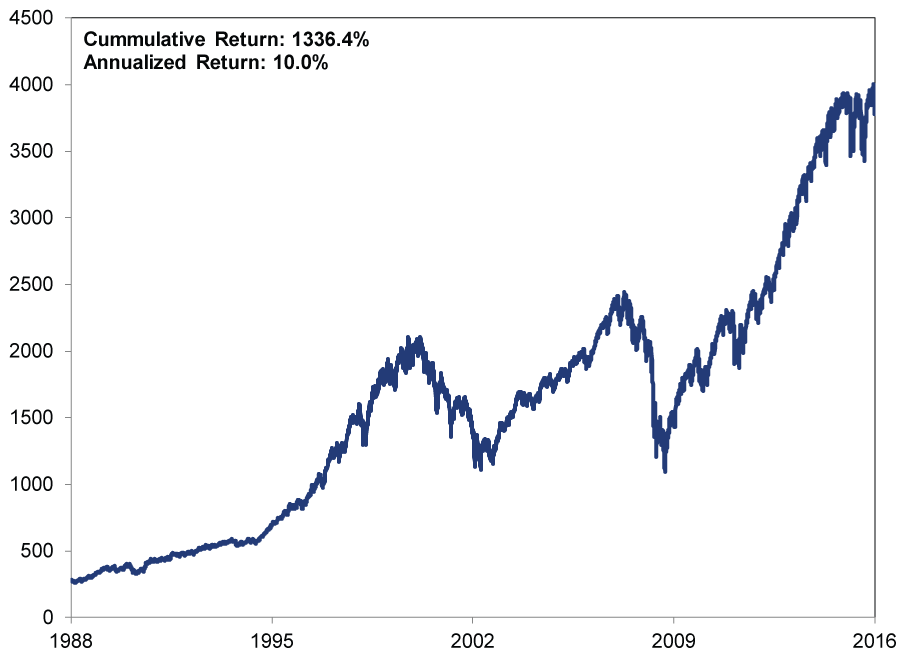

Though bumpy in the short term, stocks' long-term performance bests many other common asset classes. [iii] From 1926 - 2015, stocks[iv] returned 9.9% annualized. Corporate bonds[v] trailed at 6.1%, while 10-Year Treasurys were lower still at 5.3%. Muni bonds?[vi] 4.2%. What about gold, everybody's favorite precious metal? Since 1974,[vii] gold has returned 5.5% annualized compared to the S&P 500's 10.1% over the same period. While each of these assets likely beat stocks here and there over select time periods, in the long run, stocks shined brightest. Maybe, just maybe, there is some other private investment that outperforms stocks. Maybe. However, that would be awfully hard to document, and in all likelihood, that asset lacks one of stocks' most attractive features: liquidity, the ability to convert it to cash in a hurry without materially dinging the price.

Stocks have provided this return despite a chaotic, imperfect world. Consider what has happened globally over the above charts' timeframes. Since 1988, the Berlin Wall fell, the Savings & Loan crisis came to a head and the Gulf War started and ended ... and that was all before we were robbed of the 1994 World Series. In the second half of the 90s, there was the Oklahoma City bombing, the Asian Contagion and the Tech Bubble. After entering the 21st century, there was 9/11, the War in Afghanistan and a second Iraq War. Need more chaos? Over the past decade, the Financial Crisis struck, Europe suffered a Greece-led existential crisis and Britain voted to leave the EU. I'm not even including the scores of other terrorist attacks, political bombast (remember the debt ceiling and the Fiscal Cliff?), multitude of scandals and other "negatives," real and perceived. We have had seven presidential elections, and after the eighth, the next leader of the free world will likely be either a career politician dogged for decades by corruption allegations or a businessman-turned-reality TV showman with a penchant for bombast. Through it all, stocks have chugged on higher-a sign of their resilience.

That certainly doesn't mean it has been a pleasant or comfortable ride. Bear markets inevitably follow bulls, and if you started investing around the beginning of a bear market-an extended market decline of more than -20%, driven by fundamental reasons-your view of stocks may understandably be more jaded and skeptical. However, that 9.9% long-term annualized S&P 500 return includes both the Great Depression and the 2008 Financial Crisis, two of history's biggest bears, and 11 others. Just as stocks can have really bad years, they can have really good ones too-and the good tend to outnumber the bad. If you're invested for the long term, your portfolio could recover from even the worst of bear markets given enough time. Real-life example: Let's say you started investing in the S&P 500 on 10/9/2007, the final day of the last bull market. If you stayed invested from then to now, your portfolio would be up double digits.I'm not advocating you simply just buy and hold-if you can identify a bear near its beginning, when there is far more downside ahead than behind you, it makes sense to adjust your portfolio as appropriate. However, avoiding bear markets isn't required to enjoy long-term growth, provided you fully capture the surrounding bull markets.

Now, despite their many attractive qualities, stocks can be pretty bouncy in the short term, and it's impossible to pinpoint the perfect time to start owning them. However, nailing the entrance is unnecessary, in my view, because whenever you actually start investing is ultimately an arbitrary date. Consider when you started investing: Perhaps it was when you had sufficient savings to start preparing for the more distant future, or maybe it's when you inherited a portfolio your family started for you. Regardless, random, just like how I selected the start dates for Charts A, B and C. Their respective start dates align with the years I was born,[viii] when I started college[ix] and when I started working at Fisher Investments. Nice little milestone dates for me, but most likely meaningless to you.

More importantly, while your start date won't preclude you from enjoying stocks' future returns, your actions-or lack thereof-will. Though you don't ever get to choose your returns, remaining disciplined and focused on the long term will allow you to benefit from stocks' growth, regardless of when you began investing. Sure, if you started at the beginning of a correction or even a bear market, your total return number might not look as nice compared to someone who started investing at the beginning of a long bull market. However, how your portfolio compares to someone else's is irrelevant-what matters a whole lot more is whether you have an allocation appropriate for you. Remember, stocks' future returns don't depend on the past, and if you require long-term growth, you need to own assets that will give you the highest likelihood of reaching your personal investment goals. For many folks, I believe stocks' combination of growth, resiliency and liquidity makes them the best vehicle for getting there.

[i] Feel free to reach out if you'd like to send $1 million my way.

[ii] There could be someone out there who is perfectly calling the market and is laying low to avoid drawing attention to herself, which would actually be a sign of her brilliance. If you are an expert market timer and have the proof to back it up, I'd love to hear from you!

[iii] Figures in this paragraph are from Global Financial Data, as of 2/11/2016.

[iv] I'm using the S&P 500 here because of its robust time series.

[v] US AAA Corporate Bonds, >20-year maturity

[vi] US Muni Bonds, >10-year maturity

[vii] This is around the time gold started trading freely.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today