Personal Wealth Management / Market Analysis

Striking Gold?

What should long-term investors consider in the wake of gold’s worst quarter as a freely traded commodity?

In the long term, gold is a better hobby than investment. Photo by David Paul Morris/Getty Images.

What to do about precious metals?

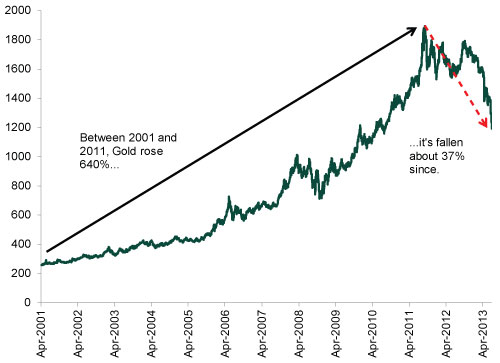

That appears to be the question du jour, given gold’s -25% decline in Q2—its worst quarter since controls on free trading were relaxed in 1973. And Q2’s decline isn’t an isolated incident. Gold’s off more than 37% from its 2011 peak—a bear market by nearly anyone’s definition.

Exhibit 1: Gold Spot Price

Source: Federal Reserve Bank of St. Louis, 04/01/2001 – 06/28/2013.

Gold’s shiny cousin, silver, has fared no better. From its 2011 peak, silver has slid roughly 60%.

On this website we’ve frequently discussed the mythology that hangs around gold. Today we’ll not do so. (For one, recent price movement has made it perfectly apparent shiny objects are no stable stores of value).

Assuming you’re an investor with long-term goals, asking whether and when gold and silver recover isn’t the right question. A more important consideration is what, if any, role gold and/or silver should play in your portfolio over your entire investment time horizon. Or, said differently, will gold and silver potentially contribute to the long-term returns you need to reach your goals? Or detract from them?

In the long run, gold and silver are more volatile than stocks and bonds. According to finance theory, more volatile assets should have higher long-term returns to compensate for the additional gyrations. Yet the opposite is true of gold and silver. Stocks easily exceed gold’s long-term return, implying the commodity’s risk/return trade off isn’t in investors’ favor.

Exhibit 2: Growth of $1 Invested in November 1973 (Log Scale)

Source: Global Financial Data, Inc., accessed 07/01/2013. Gold spot price and S&P 500 Total Return Index 11/1973 – 06/2013. US 10-Year Treasury Total Return Index (Constant Maturity) 11/1973 – 05/2013.

Some might argue gold’s a hedge against equity volatility. Yet this would require a strong negative correlation over time. Over short periods, gold and stocks can move in opposite directions. Gold’s certainly been negatively correlated to the big bull market over the last two years, falling while stocks rose. Yet in 2008—when you would want an asset negatively correlated to stocks—they moved in the same direction, as gold initially fell more than 25% during the financial panic. Simply, there is no discernible long-term relationship between the two assets—and no predictable pattern to the short bursts of negative correlation. With subpar long-term returns and no meaningful negative correlation with stocks, gold isn’t reliably useful to equity investors over long or short periods.

In our view, there’s just little place in a growth-oriented portfolio for a long-term gold investment. If you have one, it’s likely costing you opportunity. But some gold bugs will be frozen, we’ll bet, because of the recent decline. They’ll hold, awaiting a rebound. They’ll try to foresee the bottom. Media coverage probably won’t much help their efforts. Many observers seem confounded by the movements. Some still persistently and doggedly cling to a stubbornly bullish view—a view likely held throughout this golden bear. But most coverage seems to ponder the future—is this the bottom or is there further to fall?

Our advice is to avoid falling into this trap. Focus on your goals and get allocated with an eye toward achieving them. However long you’re not allocated in a strategy likely to reach your goals is a period where you’re taking serious risks, increasing the likelihood you don’t get where you want to go. Whatever happens to gold and silver in the near term—a bounce, a further downdraft, a flatline—incorrect allocation is a fundamental error and one we believe should be corrected post haste.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today