Personal Wealth Management / Market Analysis

Surveys to Shut Down US Data Worries

While the government shutdown has delayed some official statistics, other datasets point to growth.

As folks fret the lack of official data due to the government shutdown, we already have some compelling evidence the US ended 2018 on a growthy note—thanks to the Institute for Supply Management’s (ISM) December manufacturing and non-manufacturing purchasing managers’ indexes (PMIs). Both were in expansionary territory: 54.1 for manufacturing and 57.6 for non-manufacturing. Yet many headlines glossed over this. They instead highlighted December’s relatively weaker readings and fretted their future implications. In our view, this misperceives how PMIs work—an example of dour sentiment clouding folks’ view of positive data.

PMIs are monthly business surveys that track economic activity across various sectors. Businesses report activity in categories ranging from new orders and employment to inventories and prices. PMI aggregators then crunch the numbers to determine how many respondents grew, how many contracted and how many reported no change. Generally speaking, readings above 50 mean more firms expanded; readings below 50 mean more firms contracted. Hence, over 50 implies broad growth, while under 50 suggests contraction.

This quick glance at business activity has limitations. PMIs indicate only the breadth of growth, not the magnitude. As surveys, they are technically opinions and lack the nitty-gritty detail “hard” data provide—so they don’t have a one-to-one relationship with GDP. However, they provide a handy snapshot of the economy, and December’s numbers confirm 2018’s snapshot was expansionary.

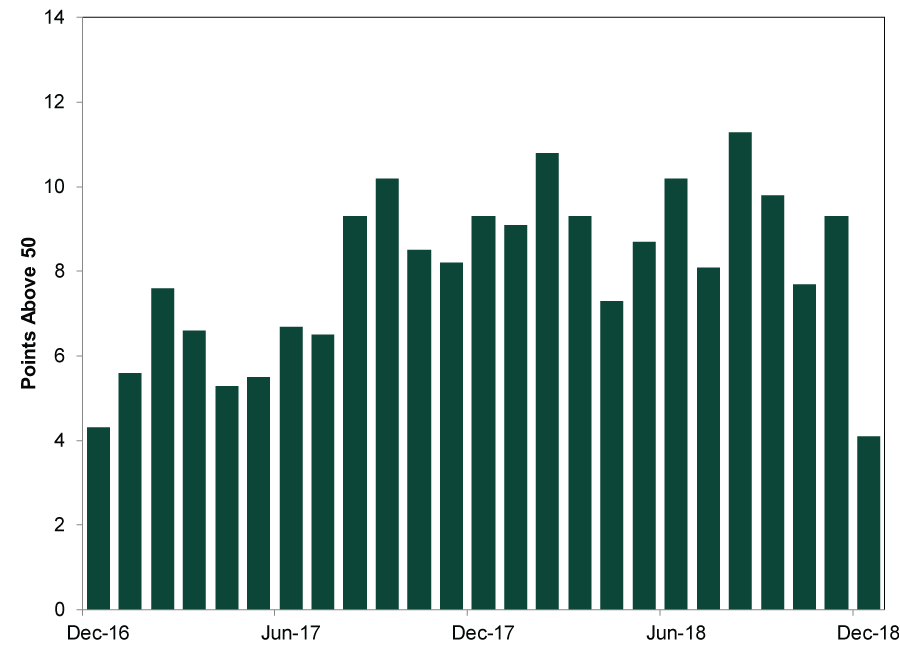

Exhibit 1: ISM Manufacturing Since December 2016

Source: FactSet, as of 1/10/2019. ISM Manufacturing Purchasing Managers’ Index, December 2016 – December 2018.

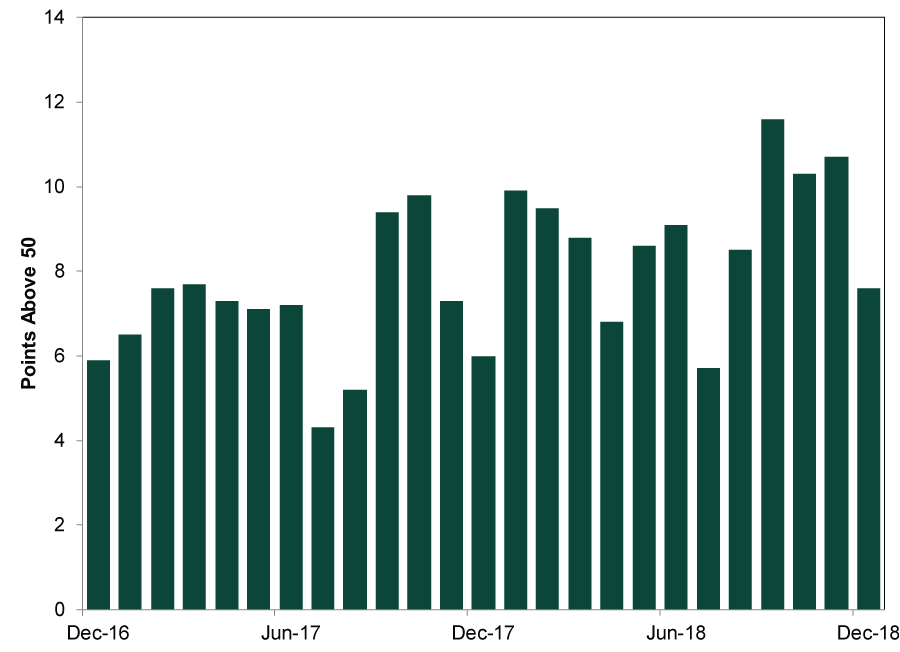

Exhibit 2: ISM Non-Manufacturing Since December 2016

Source: FactSet, as of 1/10/2019. ISM Non-Manufacturing Purchasing Managers’ Index, December 2016 – December 2018.

However, December’s reports triggered more concern than cheer from financial media—especially ISM’s manufacturing PMI. Folks zeroed in on “the largest one-month drop since the end of 2008, during the financial crisis.” (It actually wasn’t, as May 2011 tops it.) The New Orders subindex—PMIs’ most forward-looking component—fell 11 points. In a vacuum, these tidbits look troublesome, but the details suggest the dour reaction is off base. The monthly change in a PMI is less important than the level. October 2008’s -5.9 point drop put the gauge at a deeply contractionary 38.9.[i] But December 2018’s 54.1 still indicates a majority of businesses expanded. Even after an 11-point drop, the New Orders index registered 51.1—to us, that says more about how growthy New Orders have been than inherent weakness. Over the past two years, the manufacturing PMI’s New Orders index has been below 60 just three times. December’s Supplier Deliveries index was also down to 57.5 from 62.5, implying deliveries were still slowing, but at a more manageable rate than past months. Overall, one slower PMI reading doesn’t mean contraction looms or a slower trend is underway—especially when other data are solid. For example, the Fed just announced December industrial production rose 0.3% m/m, and the manufacturing component jumped 1.1% m/m—the biggest gain since last February.[ii]

Plus, manufacturing represents only 11% of US GDP.[iii] The services sector, which is part of the non-manufacturing PMI, is much larger at about 69%[iv]—and December’s non-manufacturing PMI was quite robust. Of 16 non-manufacturing industries, only 1 (Mining) reported contraction. The New Orders index enjoyed an uptick, from 62.5 to 62.7. Yet media were down on these numbers, too. The Wall Street Journal said December’s non-manufacturing PMI “was well below economists’ expectations for a 58.4 reading” while Reuters pointed out this was a five-month low. The fact these PMIs showed the vast majority of the US economy was growing was seemingly an afterthought.

Keep these growthy figures in mind as headlines fret over government shutdown-related delays of some widely watched US data series. Moreover, stocks are leading indicators. They price in economic growth well before backward-looking data confirm it happened. While economic data are still handy for investors, US government agencies aren’t the only source for it. If you seek trade information, you can check other countries’ tallies of trade with the US. PMIs also track export orders and imports. Curious about retail sales? See private-sector tallies, with the caveat that they tend to be narrower and more volatile than the government’s. You can also dig into the non-manufacturing PMI, which covers the retail industry as well as hospitality and food services. The press release will tell you whether these industries reported expansion. If you miss the durable goods orders report, then review the industry breakdown of the manufacturing PMI’s new orders component. In December, industries known for manufacturing durable goods reported growing new orders. If you miss GDP, comfort yourself with The Conference Board’s Coincident Economic Index. Or, even better, behave like stocks and look forward—at the Leading Economic Index. It is high and rising, signaling continued expansion.

In our view, the economic fundamentals underpinning the US expansion remain intact. No single dataset is perfect, but taken in tandem, all the numbers we have say the US economy is on firm footing. With leading indicators pointing to more growth ahead, we believe US recession fears remain off base.[i] Source: FactSet, as of 1/11/2019.

[ii] Source: US Federal Reserve, as of 1/18/2019.

[iii] Source: FactSet, as of 1/17/2019.

[iv] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today