Personal Wealth Management / Economics

The Affordable Care Act’s Affordability: Taxes

The US election results seemingly have given rise to heated rhetoric over the Affordable Care Act’s implementation. Let’s analyze the likely economic and market impact.

As always, MarketMinder’s commentary on politics and politically related issues attempts to be non-ideological. Neither party, in our view, is superior for the economy or markets, and both parties have historically championed policies we both liked and disliked. Our commentary is limited to the likely market and/or economic effects of proposed or enacted legislation. Similarly, our commentary will not discuss or broach societal implications.

While the US election may be behind us, many politically based issues remain heated and thorny. One major remains the Affordable Care Act (ACA), the health care reform law signed by President Obama in 2010.

Following the Supreme Court’s ruling in favor of the ACA’s constitutionality last June, it seems some opponents of the Act pinned their hopes of repeal on the election of Mitt Romney. Since his defeat about two weeks ago, they now presume implementation is certain.

And there’s little reason to think it isn’t certain to proceed. But realistically, that’s not a change from where the probabilities stood before November 6. As we’ve written, President Obama was favored to win before the election—incumbents are just darn hard to unseat. And even if Mr. Romney had won, he would likely have needed a filibuster-proof Senate majority and the Republican House majority to pass legislation overturning the ACA. That, too, was unlikely—and results showed the Senate really wasn’t much in play. In other words, with neither the pre- nor post-election Congressional make-up, the ACA was highly likely to be implemented. Therefore, it seems unlikely ACA implementation poses a material surprise for stocks. Whatever you think of the legislation’s economic merits (discussed more later), at this point it isn’t so much whether the law is good or bad, this lack of surprise power means investors who dislike it have probably already acted—meaning it is unlikely to prove a lasting, material market mover.

That is not however, to argue the ACA has no impact.

On an industry-level, the ACA (and most legislation like it) has a tendency to create losers and winners. As we’ve written, hospitals seem poised to benefit in the near term as more folks are covered and fewer uninsured patients seek treatment they can’t afford. It seems likely to be a wash for managed care firms. And it could potentially negatively impact other Health Care sub-industries, on balance.

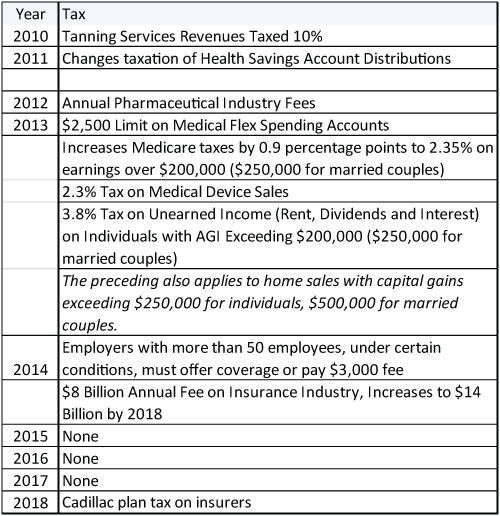

Outside the Health Care sector, the principal impact seems likely to be new taxes associated with the legislation. Exhibit 1 shows these new taxes and the year the specific provision will be implemented.

Exhibit 1: Affordable Care Act Taxes By Year of Implementation

Source: Kaiser Family Foundation, Fisher Investments Research.

To be sure, we’re no fans of higher taxation. Or new taxes. (Blech.) But from an investor’s point of view, these taxes seem most likely to, like the industry effects, create winners and losers. It’s just very unlikely a tax on dividends or passive real estate rental income serve as bear market catalysts. However, taxes can adjust behavior—of individuals or corporations. As we’ve written, when you tax something, you tend to get less of it. A dividend tax could drive some firms to buy back shares (bullish) instead of paying cash dividends (also somewhat bullish).

But aside from these investment implications, an important consideration: The tax employers will be forced to pay for not providing coverage is lower than what many firms’ medical benefits cost per employee. So the company can save money by pushing employees toward government-subsidized purchases on health insurance exchanges. Perhaps that’s why a McKinsey study conducted after the ACA’s passage showed many firms planned to simply cease coverage if the ACA was enacted. So while some companies that wouldn’t otherwise offer health insurance will be forced to or pay the tax, others may get a profitability boost as their insurance-related costs drop. Again, winners and losers. The ACA’s embedded incentives seemingly push private firms away from providing insurance, which could mean that, over the longer term, the ACA does to private health insurance what FDR’s New Deal did to private unemployment insurance when it enacted government-backed unemployment coverage. (Yes. That once existed. And it was fairly common.) Again, winners and losers.

We realize fully this isn’t the line of logic you’ll likely hear in the punditry, who figure the ACA is either a massive boon or incredible bust. And far be it from us to suggest the law is perfect—or even good. But ultimately, those who overstate the economic impact of the law are likely doing so because they’re overly focused on one segment of the economy and not taken the full spectrum into account.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today