Personal Wealth Management / Economics

The Big GDP Bang Analysts Project

Across the developed world, expect huge Q3 2020 growth rates. Don’t overthink the implications.

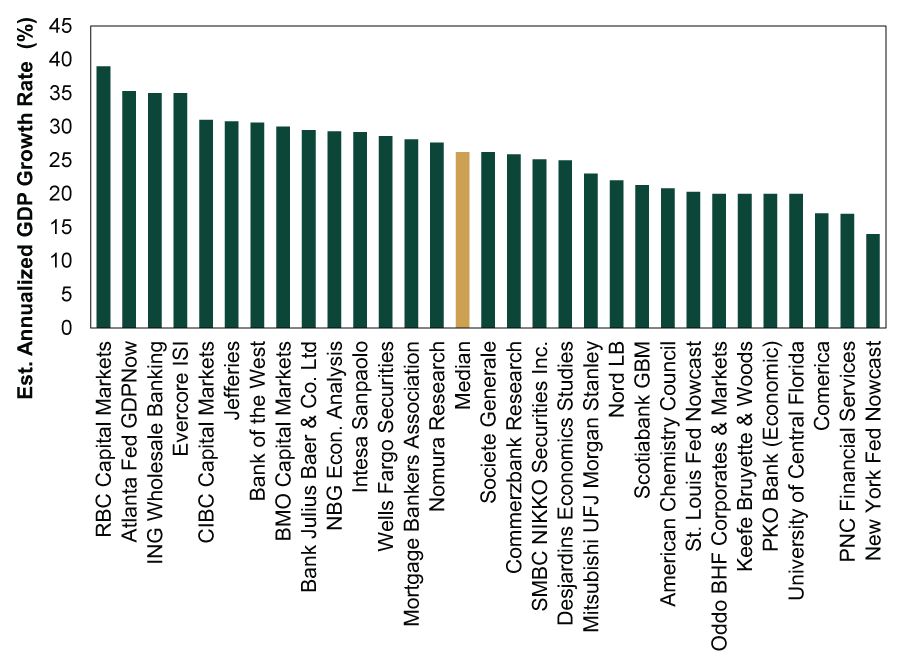

Twenty days from now, in what is sure to be a heavily covered release, the US Bureau of Economic Analysis will unveil its advance estimate of US Q3 2020 GDP. After a historic decline in Q2, expect the reverse: a historically huge surge. How large? Estimates tracked by FactSet run the gamut from 17.0% annualized to 39.0%.[i] The Atlanta, New York and St. Louis Fed’s nowcasts—attempts to estimate GDP growth in real time using incoming data throughout the quarter—put Q3 at 35.3%, 14.0% and 20.3%, respectively.[ii] The median of these 30 total forecasts is 26.1%. Similarly huge jumps—if not huger—are expected in most of the developed world. The takeaways from this for investors are limited, but we do think putting these data in perspective can help manage expectations.

The third estimate of US Q2 2020 GDP put the springtime contraction at -31.4% annualized, the biggest drop since … ever. Now, as we told readers (probably too often), that doesn’t mean GDP fell by roughly a third. That is the rate of decline if contraction lasted a year at that quarterly clip. Similarly, if the median Wall Street estimate holds, the 26.2% annualized jump wouldn’t mean that GDP grew by more than a quarter.

As for those estimates, Exhibit 1 plots 30 forecasts of US Q3 GDP, as tracked by FactSet, and the three regional Feds. For some perspective, America’s highest-ever growth rate since quarterly GDP data began in 1947 was Q1 1950’s 16.7% annualized.[iii] All of Wall Street’s current estimates exceed this. Only the bears over at the New York Fed estimate a weaker-than-record growth rate.[iv]

Exhibit 1: Range of US Q3 GDP Growth Forecasts

Source: FactSet, as of 10/9/2020. Forecasts range from Oddo’s made on July 22 to RBC’s on October 8, and all are subject to revision.

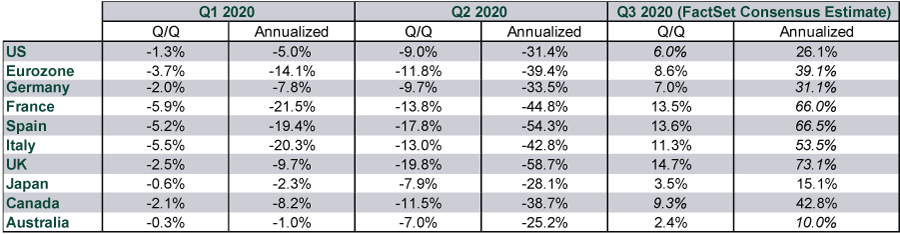

Forecasts for other major nations are even bigger. Exhibit 2 shows this in both quarter-over-quarter and annualized terms, to facilitate comparison.

Exhibit 2: Median Q3 GDP Growth Forecasts for Selected Developed Nations

Source: FactSet, as of 10/8/2020. Italicized figures represent our conversion of the data from annualized to quarter-over-quarter, or vice-versa. The other estimates in the Q3 column were provided by FactSet.

It is important to note, in our view, that these enormous growth rates are due largely to the exceedingly depressed base they build off of. When you shutter a wide swath of the economy, a sharp contraction is the outcome. No matter the nobility of the purpose, a downturn is a feature of lockdowns, not a bug. Their point is to cease in-person activity. Reopening businesses, then, virtually assures a rush of activity. Despite loads of economists talking up policy responses, that simplistic tale is what Q2 and Q3’s rollercoaster data reflect.

Looking ahead, the median of 28 estimates tracked by FactSet reflects this, putting Q4 US GDP growth at 5.2% annualized. That would historically be quick, but it obviously isn’t going to set any records. This, plus the associated slowdowns in various other data series like nonfarm payroll growth and retail sales, has many pundits worrying the recovery is slowing—losing steam. It is slowing, of course, but that shouldn’t surprise. Once the base is higher from businesses having reopened, slower growth rates are only natural. They are a sign that a semblance of normalcy is returning. So no, Q4 2020 GDP won’t spike massively like Q3. That is a good thing.

Of course, we probably also won’t see pre-COVID output levels in Q4 either. But these are pretty arbitrary markers. For stocks, they hold little significance. There is no sign reaching pre-recession output levels has ever influenced stocks in the past. Now shouldn’t be different. Besides, we think markets—discounters of conditions 3 – 30 months ahead—are likely looking well beyond 2020 at this point, to a time when COVID and the related lockdowns are a bad memory.

So, our advice: Set your expectations for a massive Q3 US GDP report in 20 days’ time. But don’t overthink the implications, because there aren’t many.

[i] Source: FactSet, as of 10/9/2020.

[ii] Source: Federal Reserve Banks of Atlanta, New York and St. Louis, as of 10/9/2020.

[iii] Source: US Bureau of Economic Analysis, as of 10/8/2020.

[iv] Come on, we don’t know that they are actually bearish. That is a joke.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the Iran Flare Up2026-07-08

-

Market Analysis Can Germany Engineer Faster Growth at Last?2026-07-07

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-07-07

2026-07-07 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 29 - July 32026-07-07

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today