Personal Wealth Management / Market Analysis

The DOL Gets a Homework Assignment

The skinny on the White House's plans to apply the fiduciary standard to any investment professional advising on a retirement account.

As always, our political analysis is non-partisan and ignores ideology and sociological factors. Our aim is solely to assess how the proposed rules impact investors. Oh and full disclosure: MarketMinder's parent company, Fisher Investments, is a registered investment adviser held to the fiduciary standard.

President Obama gave a big speech at AARP on Monday and made the announcement the world was waiting for: He had picked up his AARP card. Kidding![i] He said he told the Department of Labor to write rules requiring any investment professional advising on a retirement account to "put the best interests of their clients above their own financial interests."[ii] He goes on: "You want to give financial advice, you've got to put your clients' interests first. You can't have a conflict of interest." And not to be overly literal, but we have a hard time seeing how a uniform fiduciary standard, as outlined on The White House Blog Monday, will do this-or solve any of the issues described in Obama's speech. A fiduciary standard can't eliminate conflicts of interest or ensure investors receive top advice. Well-intended as these plans seem to be, they won't fix all that ails the brokerage industry, and the onus will remain on investors to look beyond rules and designations when picking an adviser.

According to the White House: "Under our current system, your advisor can accept a back-door payment or hidden fees for directing you toward a retirement plan that's not in your financial best interest. ... Right now your financial advisor-someone who's supposed to be acting in your best interest-can direct you toward a high-cost, low-return investment rather than recommending a quality investment that works better for you. That's because those lower-return investments come along with hidden fees that benefit their Wall Street firms on your dime. On average, these conflicts of interest result in annual losses of about one percentage point for affected investors."

This is oversimplified to the point of inaccuracy. The use of "advisor"-with an O-implies they are discussing brokers-financial-product salespeople-who call themselves "advisors" to avoid the brokerage world's icky stigma. AdvisOrs are not required to act in their clients' best interest. Most are subject to the suitability standard, which merely requires them to sell products and investments that are justifiable based on the client's age, risk tolerance and other similar factors. They need not disclose potential conflicts of interest. Registered Investment Advisers-with an E-are subject to the fiduciary standard, which requires them to reasonably believe they're putting clients' interests first and disclose all potential areas of conflict. Many brokers are dual-registered and follow one standard or the other depending on the situation, blurring the line between sales and service.[iii]

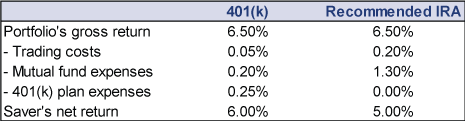

The administration's beef is with the suitability standard, which they say causes those annual "losses" of about one percentage point for each impacted investor, or $17 billion annually worth of returns missed because folks are in an allegedly inferior option. How? They believe brokers' compensation-commissions and revenue-sharing agreements with mutual fund companies-incentivizes them to move investors from low-cost retirement plans to IRAs with higher-priced funds. In their hypothetical example, on page 17 of this report, they show a hypothetical choice between a 401(k) plan "invested in an index fund holding a mix of stocks and bonds"[iv] and an "IRA investment [that] matches the risk characteristics of the 401(k) investment and earns an identical expected return before accounting for any costs [yet whose] frequent trading strategy results in significantly higher trading costs." So, in other words, an actively managed fund. We are then shown this table:

Exhibit 1: Hypothetical Example of How Brokers Eat Your Savings

Source: "The Effects of Conflicted Investment Advice on Retirement Savings," WhiteHouse.gov, February 2015.[v]

The difference between the 401(k)'s net return and the IRA's net return is the one-percentage-point "loss." The paper goes on to apply the 6% and 5% return to the $1.66 trillion in IRA money invested in "load mutual funds and annuities" to calculate that $17 billion annual "loss." Folks, it isn't a loss. It is a skewed estimate of supposedly missed return that has zero bearing in reality. Here are some reasons why:

- It ignores the return of the actual funds used.

- It assumes all 401(k) plans are invested in index funds.

- It ignores everything about annuities.

- It uses an arbitrary assumption for mutual fund trading costs, which are not disclosed.

- It assumes high fees are the sole way subpar recommendations subtract value.

This speaks to the larger problems with the administration's analysis, as laid out in a 30-page report by the White House Council of Economic Advisors. It overfocuses on mutual funds, assumes an IRA is something you "purchase," assumes studies showing high-load funds underperform no-load funds prove IRA investors leaning on brokers' advice are getting subpar returns, and it ignores what brokers actually do. Here are some issues with this:

- These studies measure mutual fund performance over long stretches of time. Other reports show the average mutual fund investor owns each fund for 3.3 years. The White House study ignores the impact of this short-term trading.

- IRAs are not products you buy.

- It ignores brokers who sell individual stocks.

- It assumes revenue-sharing agreements, where mutual fund companies pay trail commissions to the brokerage house distributing the funds, automatically influence brokers' recommendations. However, brokers don't directly receive these payments, and they frequently aren't accounted for in the broker's compensation package.

- It assumes brokers acting in a client's best interest would automatically recommend passive funds purely because they are cheaper and active funds, on average, have historically lagged them after fees on several occasions.

- It ignores all the qualitative reasons a broker might believe a higher-cost product might be in a client's best interest.

That last one is the kicker. Fees aren't the sole determinant of whether a product is best-there is no way to quantify "best." It is a matter of opinion, pure and simple. One table in the White House's report shows how 10 academic studies found "conflicted investment advice" was fleecing investors-but that's all in the eye of the beholder. One study's evidence was the fact adviser/advisors recommended active funds, not passive. But what if they believe active funds offer more opportunities for diversification and risk management, and disclosed any revenue-sharing arrangements? Another cited advisers/advisors for recommending active funds instead of "lifecycle funds," Canada's equivalent of target-date funds (TDF). Which overlooks the fact there are major issues with TDFs. They commonly lack transparency regarding fees and asset allocation strategy and are largely based on industry myths about time horizon and risk tolerance. We would suggest an advisor/adviser moving you away from a TDF may be doing you one heck of a service. And, the coup de grace, a GAO report claimed "a service provider could earn $6,000 to $9,000 in fees from a participant's purchase of an IRA, compared with $50 to $100 in fees if the same participant were to invest in a fund within a plan." Again, an IRA is not something you purchase. The GAO report is hazy, but in our experience, the only way an adviser/advisor could earn this commission is if they sell a variable annuity-lousy, in our view, but if they believe that's best and disclose their compensation, it could technically comply with either the suitability or fiduciary standard.

A uniform fiduciary standard wouldn't prevent any of the ills described by the White House. Or issues described throughout the financial press. Again, the adviser must simply believe, reasonably, that what they're recommending is best for the client. Opinion! Opinion based on their own personal biases, knowledge and experience. That varies wildly across the industry. An adviser could believe a variable annuity is so wonderful and their client should own it-even in an IRA, where they'd essentially be paying for a redundant tax shell.[vi] That wouldn't be illegal! They'd just have to disclose the conflicts inherent, like how they are compensated for selling the annuity. Ditto for all those high-priced funds.

Folks, we too are sick of the brokerage world's flashy tactics, opaque compensation and conflicted recommendations. But a uniform fiduciary standard won't erase any of that. The ills come from brokers' compensation model, and that compensation model isn't going away. The DOL already proposed a fiduciary rule that banned revenue-sharing and trading commissions. It went nowhere. We likely won't see their new rule for at least 90 days, but it is widely believed to be a watered down version that leaves the real conflicts intact. The new rules will likely simply require brokers to disclose those conflicts and explain clearly the logic behind their recommendation. Our guess is they'll come up with a fancy bunch of legalese to do this in one lengthy form few, if any, mom and pop investors will be able to unpack.

Plus, as we've written before, rules don't guarantee behavior[vii] or quality. A broker who believes industry mythology, believes a client's age is the sole determinant of asset allocation and believes past mutual fund performance predicts future returns will probably give pretty lousy advice regardless of which regulatory standard governs them. You can't make someone smarter, more ethical or more client-focused by government diktat. The fiduciary standard doesn't differentiate between the 25,000-plus RIAs, and it won't differentiate between the hundreds of thousands of brokers who will be subject to it if the DOL rule takes effect. The onus will remain on investors to do thorough research on any prospective advisEr or advisOr's values, expertise, resources, track record and investment philosophy to determine who will truly put their interests first.

And hey, don't take our word for it-we leave you with a quote from SEC Commissioner Daniel Gallagher: "I am greatly concerned that much of the debate on these issues seems to assume that the 'fiduciary duty' is a sort of talismanic protection that can overcome any competing regulatory concerns. All too often, this is the approach taken by those who simply do not know how the fiduciary duty works in practice. They do not understand or choose to ignore the limitations of the fiduciary duty," acknowledging that "even the SEC has much to learn about the real-world application of the fiduciary duty - an area that receives far less attention than it should."

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] He cracked this joke, not us, so don't blame us if you don't find it funny.

[ii] The SEC is still weighing a separate proposal that would apply a fiduciary standard to every broker and adviser. Dodd-Frank ordered them to investigate the issue, and their opinion is allegedly forthcoming.

[iii] This line was never supposed to blur. The two standards were meant to separate investment sales from investment service in order to minimize conflicts of interest and promote transparency. Draw the line more clearly, and none of this is an issue.

[iv] Side note, there is no such index fund on planet Earth. Index funds are supposed to mirror an index. There is no hybrid stock/bond index. It is a fictional fund, which is your first clue the table is a fictional analysis.

[v] You cannot compute net return like this in the real world. This is not how the actual math works.

[vi] In our view, this is seriously no-no time. But all a broker-pardon, advisOr-must do to be in compliance with the current rules is have a client sign a disclosure stating that they are buying the annuity in an IRA for reasons other than tax deferral.

[vii] See this and this for more on fiduciaries who were busted for fraud.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Oil Prices, UK Politics, Tech Stocks

2026-06-26

2026-06-26 -

Market Analysis Excess Fear Over ‘Excess’ Profits2026-06-25

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today