Personal Wealth Management /

The Faults of Municipal Default Fears

Recent events in Detroit and Illinois have prompted jitters over municipal finances, but overall, state and local debt is in fine shape.

Almost exactly three years ago, municipal debt fears spiked in the wake of a well-known bank stock analyst’s prediction on 60 Minutes that a tsunami of municipal defaults tallying hundreds of billions of dollars were sure to come in 2011. That forecast didn’t materialize in 2011. Since then, we’ve been told again and again to simply wait—its arrival is merely delayed. But is it so, or is the forecasted default wave merely Godot?

All of this racket picked up again after several headline-grabbing bankruptcies—most notably, Detroit. But cases like Detroit’s are relatively rare—the exception, not the rule. The wave of municipal defaults never came to pass because, overall, state and local finances were better than many appreciated. Nor are they likely to materialize in the foreseeable future—state and local finances are stronger yet heading into 2014, even in some of the problem areas.

Detroit’s bankruptcy was seen by some as a sign of the times of sorts, but it’s very much an outlier. Back in the auto industry’s heyday, Detroit enjoyed steady growth and high tax revenues, which helped it fund generous public benefits. But when the local auto industry declined, folks moved away, tax revenue fell, and high spending became difficult to support. The bankruptcy filing was the climax of a few decades of decline and unwise public finance decisions—not an indicator of nationwide state and local debt sustainability. Consider: From 2002 through 2011, Detroit’s metro-area GDP shrank -12.2%—the average US metro area grew 13.1%. Detroit residents have one of the highest combined state/local tax burdens in the country, yet the city’s tax revenues are down 40% since 2000. Meanwhile, nationwide state/local tax takes are up 63%. Simply, Detroit isn’t the US.

With Tuesday’s court decision, however, Detroit gets the green light to try and improve its long-term financial outlook. It can now work with creditors to negotiate payments, restructure its pension system and get spending more in line with tax revenue. But it won’t be easy—many of these choices are politically difficult, and public-sector employees and pensioners likely will shoulder some of the load. But some of Detroit’s pension practices were flat-out unworkable—like, for example, paying out an extra 13th month of benefits every time the fund’s annual return exceeded its long-term average target of 8%, forgetting those excess returns must stay invested in order to actually achieve that average over time.

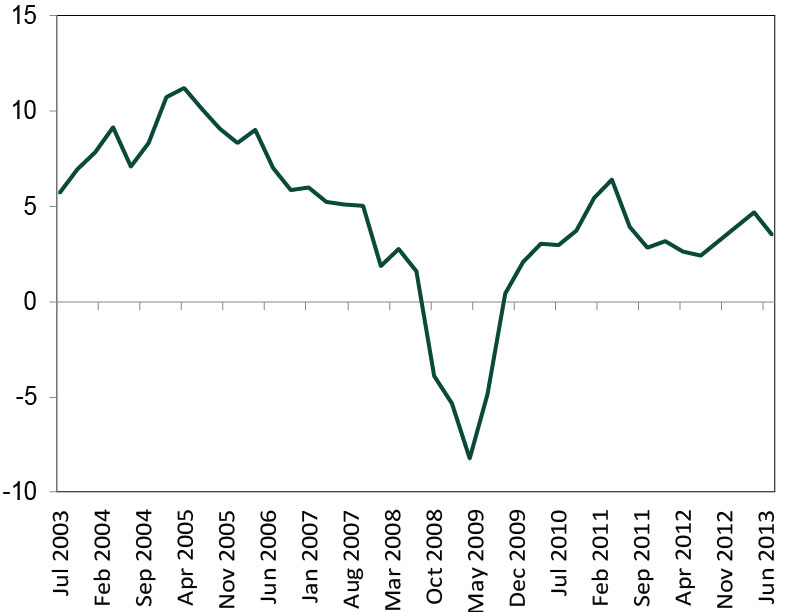

Nationwide, state and local finances look much better. For example, ratings agency Fitch recently announced most states will enter 2014 with stronger finances than 2013. This shouldn’t surprise—the economy is growing! With growth comes rising incomes, sales, property values and corporate profits—a bigger tax base. (Exhibit 1).

Exhibit 1: State and Local Government Current Tax Receipts (Annualized Percent Change)

Source: St. Louis Federal Reserve as of 12/5/2013.

This is a big reason why Moody’s—ever backward-looking—just upgraded its outlook on local government debt from “negative” to “stable.” The total number of non-investment grade issuers has risen from 171 in 2008 to 217 today, but that’s a tiny fraction of the nearly 15,000 municipal issuers. 1.4%, to be precise. Through November 20, only 45 of these issuers have defaulted in 2013—less than half 2012’s total. Those 45 defaults include all “technical defaults,” where the bond’s covenant changed, but payments weren’t missed and investors didn’t take haircuts. Not all of these 45 issues were general obligation (GO) bonds, which were at the heart of Detroit’s bankruptcy. Many were issued or backed by city-run hospitals, nursing homes and other similar agencies—revenue generating enterprises that simply fell short. It seems extremely difficult to argue a handful of defaults among the many thousand municipal agencies mean local governments are teetering on the edge of insolvency. And they were mostly small. The first half of 2013 saw less than $7 billion worth of defaults—$6.4 billion was a high-end estimate of Detroit’s impact. That’s a long, long way from hundreds of billions.

As a result, municipal bond yields are still historically cheap—markets are the best gauge of the risk of default, and low yields tell you markets know the broad risk is exceedingly low. If markets foresaw a high likelihood of a cascade of city and state bankruptcies, yields would be much higher—folks would probably require a far greater premium to take that much risk. But investors are perfectly willing to lend to them at lower rates, so cities can access affordable financing to supplement tax revenues. This gives most states and cities more than enough leeway to manage debt levels.

It’s a similar story with state and city pension plans—a widely feared source of potential muni mayhem. While headlines decry certain high-profile cases, only a handful of states have unfunded pension liabilities. Even in some of these perceived “problem” areas, officials are addressing the issue. Exhibit A: Illinois. Now, Illinois’s issues aren’t as acute as Detroit’s, but the state’s financial situation isn’t the most robust nationally and state public employees’ pensions were quite underfunded, raising concerns about its future finances. On Tuesday, Illinois approved an estimated $160 billion in pension plan cuts to rein in a significant budget shortfall. Changes include adjusting the cost of living calculation, raising the retirement age for younger employees and capping salary amounts used to calculate pension payments. Even seemingly small changes like this can help put the long-term trajectory of a pension plan on more fiscal sound footing. Despite some opposition, that the state was able to pass such measures shows, when necessary, authorities can make tough, but important, decisions to rein in budgets and address underlying issues.

Illinois is just one state—and Detroit is just one city. 2011 didn’t prove to be the year of the muni bond default. Neither did 2012—or 2013. In our view, 2014 isn’t likely to see that wave of defaults either. Overall, state and local finances are relatively healthy and it’s likely that trend continues along with the economic expansion.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis New Tax Year, More British Business Tax Fear2026-04-08

-

Market Volatility How Investors Should Think About the Ceasefire2026-04-08

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today