Personal Wealth Management / Economics

The Fruitless Folly of Forecasting the Fed

Forecasting Fed moves is an exercise in futility, as two financial writers illustrated Thursday.

For months now, the financial punditry has engaged in the wildest of wild goose chases, the snipe hunt of all snipe hunts: Attempting to divine the timing of a fed-funds target rate hike based on data, officials' commentary and events. You can rest assured that virtually any event, related to economics or no, will be analyzed by someone in terms of what it all means about the possibility the Fed hikes. Here is a short list: China's 3% mini-devaluation; the VIX; the strong dollar; stock market volatility; income inequality; falling oil prices; Emerging Markets in-and-outflows. There are more. All those are in addition to the two regular ones, unemployment and inflation, consistent with the Fed's odd dual mandate. Now, all the speculation is overwrought: As we've discussed on these pages many times, Fed initial hikes have no history of regularly derailing bull markets. But also, a couple of articles caught my eye that shed light on just why we think it's impossible and fruitless to try to foresee the Fed's actions.

In the course of explaining why he believes the Fed is bent on "normalizing" monetary policy, Bloomberg's Noah Smith provided a wonderful explanation (in bullet points!) as to why Fed actions can't be forecast:

The Fed's Fear of the Unknown

Noah Smith, Bloomberg

Smith writes:

The Federal Reserve and all of the economists who staff it and advise it are basically groping in the dark. For example, the Fed is wrestling with whether to raise rates this month or in those that follow. To make this decision, it must consider:

1) Which macroeconomic theory (or theories) to believe in.

2) How strongly to believe these theories.

3) How important economic growth is.

4) How important financial stability is.

5) How important inflation is.

6) How the Treasury will react to the Fed's decisions.

7) How other events in the world, such as the China slowdown or the Greece debt mess, will play out."[i]

You just can't know which of these seven (or more) factors rule the day in the minds of the Federal Open Market Committee, the Fed panel enacting monetary policy. Now, Smith's piece, while good, buys into one theory I don't: the presumption rate-hike calculus is harder this time, because rates are at zero. Well, zero to 0.25%.[ii]

First, policymakers abroad have already demonstrated over the course of roughly a year that the zero-bound is fiction; made up; of little import. The ECB has two policy rates in subzero territory presently. Zero is another number. But for the Fed, it's probably more salient to note that the hike would be from next to nothing to slightly above next to nothing. We are not talking about a hike to 2%. Nor does this put America on a rate-tightening course inevitably bound for those levels. The Fed can hike. And then stop, cut or hike again. It faces the same decision literally every time it meets. It is always hard for them to forecast the impact of their move, they are always biased, and there are always external factors folks argue they should consider.

Onto this stage, enter a very interesting piece by FT Alphaville's Matthew C. Klein.

Greenspan's Bogus 'Conundrum'

Matthew C. Klein, FT Alphaville

Klein goes to great pains showing even The Maestro (Alan Greenspan, not Bob Cobb of Seinfeld fame) operated on biases!

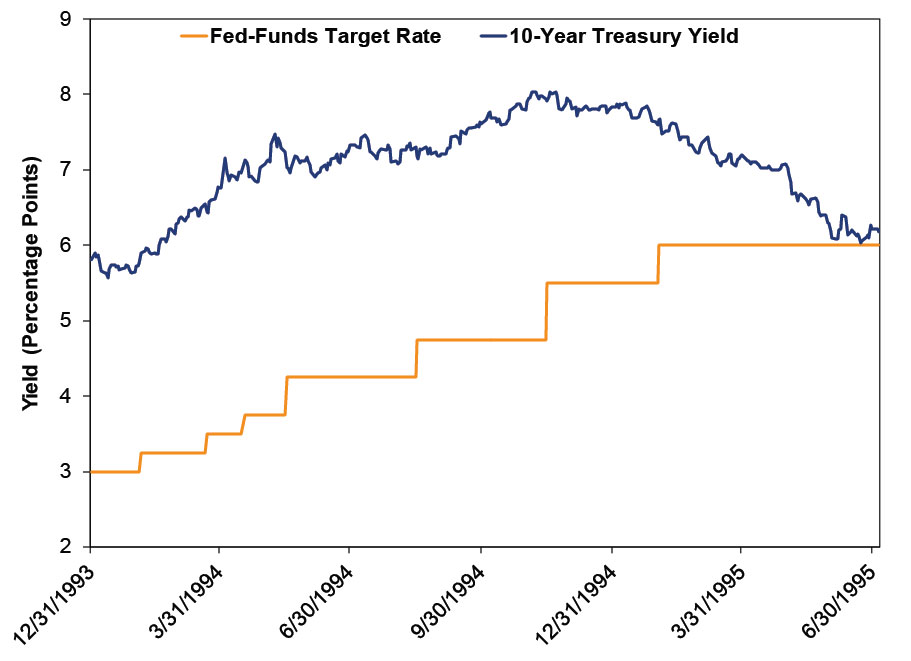

When the Greenspan Fed tightened rates 17 times in the period 2004 - 2006, driving fed-funds from 1.00% to 5.25%, the 10-year bond yield rose by only about a half a percentage point. Greenspan testified to Congress that this should have driven up 10-year yields far more, according to theory. He argued the yield curve is effectively a series of one-year maturity notes and bonds. The short end, he claimed, historically exerted a heavy influence over the long. That they did not is the "conundrum" Klein's title refers to.

However, Klein shows bond yields behaved nearly the same as the 2004 - 2006 experience in the 1988 - 1989 timeframe. To that, we'll add another: 1994 - 1996. Long rates initially rose along with short, but then flattened out while hikes continued. By the end of the cycle, long rates were falling while the Fed was still hiking. This may be why the Fed cut rates for a spell thereafter. It didn't hike again until 1999.

Exhibit 1: Fed Funds Target Rate and 10-Year US Treasury Yields

Source: FactSet, as of 9/3/2015. 12/31/1993 - 7/5/1996.

Hence, what Greenspan said he was thinking at the time doesn't seem to have been very "data dependent." The theory doesn't seem to match the actual experience.

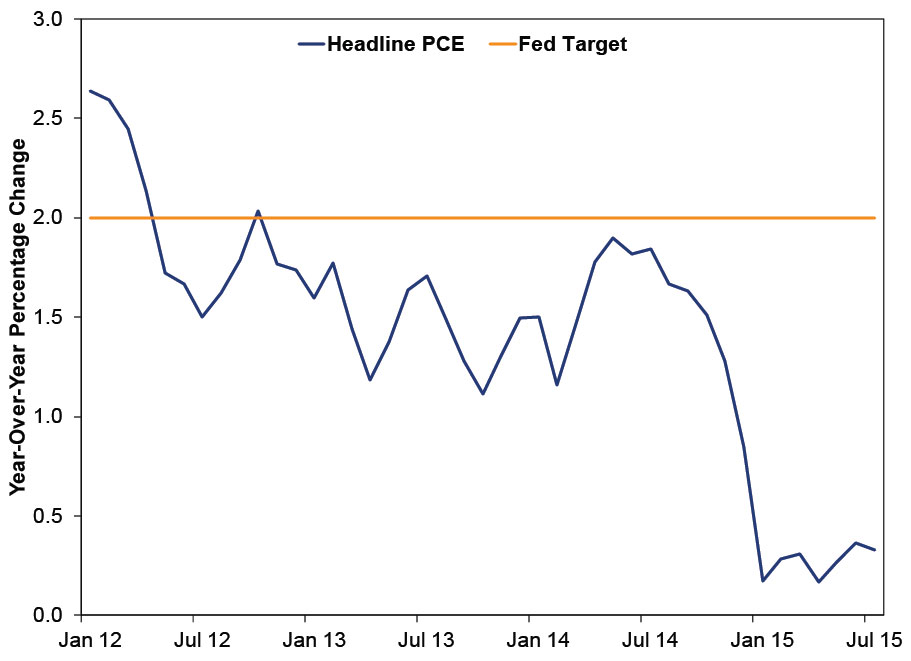

Now then, the Fed folks are different now. But for another example of the fact you still can't forecast the Fed's actions-even based on their own stated intentions-consider the headline Personal Consumption Expenditures price index (PCE including food and energy). The Bernanke Fed announced in January 2012 it would target 2% inflation based on this index. In 2015, it has trended away from the Fed's target, yet the Yellen Fed has stated outright they expect to hike rates this year. (Exhibit 2) Did they abandon their inflation target? Swap the index and not tell anyone? Forget about it? Was Yellen not on board with it? Maybe they just won't hike? What gives?

Exhibit 2: The Fed's 2% Inflation Target and Headline PCE Price Index

Source: Federal Reserve Bank of St. Louis, as of 9/3/2015. Headline PCE price index, year-over-year percentage change, January 2012 - July 2015.

Ultimately, you can't know the answers to those questions. And that is the point. The Fed is a cabal of individuals subject to their own biases, thoughts, whims and urges. If you think parsing fedspeak is a good way to decipher their future behavior, more power to you. Maybe it's fun! And that's great. As for me, I'm opting out.

[i] To that list, we'd only add: "How does Janet Yellen feel this might impact her chances of renomination under a new president?"

[ii] Nitpicky I know, but everyone says zero, possibly because the Fed called current interest rate policy ZIRP (zero interest rate policy). If you want to get really technical target rates are in a range, and the effective fed funds rate is at roughly 0.13%.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today