Personal Wealth Management / Economics

The Grass Is Greener Than Many Think

Friday’s US Q4 2011 GDP report showed growth continued—and accelerated for the third quarter in a row.

In Friday’s report, US real GDP accelerated in Q4 2011 for the third consecutive quarter—logging +2.8% growth. Based on this advance estimate, 2011’s four quarters now read as follows: +0.4%, +1.3%, +1.8% and +2.8%. Full year growth came in at +1.7%, a deceleration from 2010’s +3.0% rate, but growth nonetheless. To be sure, that’s not the quickest rate we’ve ever seen in America, and Q4’s report missed consensus analyst estimates of +3.0% growth. Predictably, this led some to label growth “anemic.” Others continue to claim, “At this rate, we’ll never reduce unemployment.” But do the facts support such assertions? Much of the answer hinges on how you define the economy.

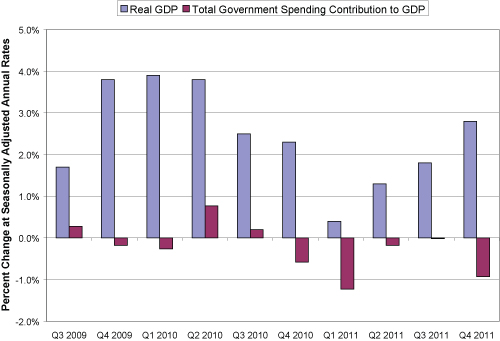

In general, inherent calculation quirks make headline GDP growth a less-than-perfect reflection of economic health. And Friday’s report was no exception. The single biggest drag on headline growth—detracting nearly a full percentage point—was total government spending (federal, state and local combined). In the quarter, government spending fell -4.6%, paced by a -7.3% reduction in federal government spending. And this is not a new trend. For the year, government spending shaved nearly half a percentage point off headline growth. And as shown in Exhibit 1, Q4 2011 marks the fifth consecutive quarter of reduced total government spending—the longest such streak since the mid-1950s.

Exhibit 1: Percent Change From Prior Period in Real GDP and Total Government Spending

Source: US Bureau of Economic Analysis.

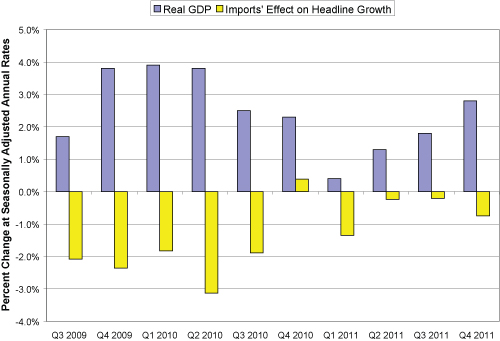

In addition to reduced government spending, Q4’s +4.4% rise in imports detracted -0.75% from headline growth. Depending on what you’re analyzing, accounting for imports as a drag may be valid. But in measuring overall vibrancy, healthy and rising import demand doesn’t equate to a moribund or weak economy. Now, the net exports calculation is nearly always wonky, but the degree to which imports have detracted from GDP in recent years has had no small effect—shown in Exhibit 2.

Exhibit 2: The Import Effect—Real GDP and Import’s Detraction from Headline GDP

Source: Bureau of Economic Analysis.

While government spending fell and imports rose, the other major components of GDP grew. Consumer spending rose +2.0% annualized in Q4, accelerating from Q2 and Q3. For the year, consumer spending grew in every quarter and increased +2.2%. Exports also grew in every quarter last year—logging +4.7% annualized growth in Q4 and +6.8% for the year. (Yes, imports and exports both grew—a more important metric, in our view, than simply clocking whether we exported more than we imported.) Business investment rose at a sharp +20% annualized rate in Q4—the fastest clip since Q2 2010, driven by inventories’ snap back from a sharp dip in Q3. Business investment grew throughout 2011, registering +4.7% growth last year. Even business investment’s subcomponent—residential real estate investment—grew in the year’s final three quarters. (And we’d note, despite the housing market’s weakness, it detracted only -0.03% from headline GDP in 2011.)

Unemployed workers aren’t going to be hired by GDP, no matter how huge the percentage change is. Equity investors do not buy shares of the BEA’s report. And the simple fact is headline GDP growth doesn’t directly equal the economy. Digging below the headline number, it’s easy to see the overall economy is generally improving and in better shape than many appreciate. Add in rising corporate revenues, private-sector employment and corporate profits per employee, and it’s even clearer. And those factors are all positive things if it’s a job, investments or just general economic health you seek.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today