Personal Wealth Management / Market Analysis

The Great Global Disconnect: Headlines Versus Data

The global economy continues to grow against a backdrop of fears it won't.

While many headlines and sentiment have shown their skeptical streak lately, the data just don't seem to want to cooperate and collapse. In fact, what we see in comparing sentiment and recent data seems much more like what we've seen during the five-plus year course of this big bull market.

First, let's take a trip around the World Wide Web and assess the economic headlines grabbing eyeballs. All these headlines hit in the last two weeks:

- The World's Biggest Economic Problem (We'll give you three guesses which region this is![i])

- China's Lack of Drama Is Likely an Intermission

- Global Growth Worries Echo Across the Pond

- China's Economy Suffers Its Worst Quarter Since the Financial Crisis (It grew only 7.3% y/y.)

- Is a Global Economic Storm Brewing?

- Spectre of Eurozone Crisis Returns, Stocks Plunge

- Fears About Eurozone Economy Hammer Markets

- Markets Are Right to Worry About Euro Zone

Most of the theses underpinning these articles are very well known to investors: China faces a big slowdown-a hard landing-which will ripple globally; the eurozone is an economic quagmire; the US can't grow alone; global growth is faltering; did we mention the eurozone is an economic quagmire? Economists have their standard prescriptions: Fiscal stimulus; don't hike rates yet!; more (misguided) quantitative easing; weaker currencies; debt forgiveness.

Now, not everyone is focused on the negative. Some notice positives. Some even highlight odd false positives, like the notion American consumers insulate the nation against global economic conditions. Which has been true roughly never. Or that a long list of charts[ii] plotting various late-lagging indicators, faulty surveys or tiny contributors to growth (employment data, consumer sentiment and home sales) represents ironclad evidence of incontrovertible growth.

But still, there are better data-from around the world-showing growth continuing up to the present, and some suggesting it looks poised to keep going from here.

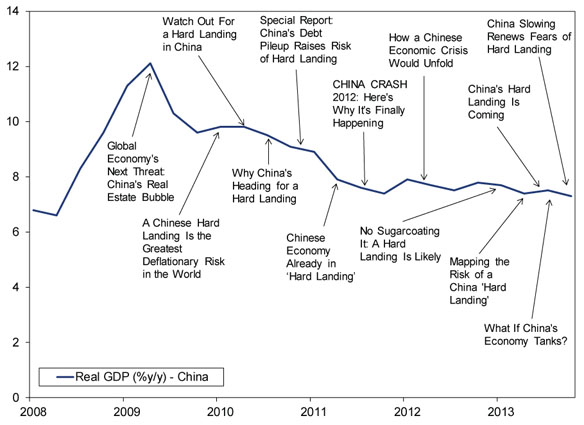

This week, the Flash HSBC China manufacturing Purchasing Managers' Index (PMI) accelerated, logging an expansionary 50.4 reading. While the gauge isn't a perfect view of China's economy, as it omits the large, state-run firms, the acceleration cuts against those dogged hard landing fears. And it all follows Tuesday's Q3 GDP report, which showed China's economy grew 7.3% y/y. That's a touch slower than Q2's 7.5%, but a drop of 0.2 percentage point is not the stuff of a hard landing. It is not far removed from the trend we've seen for years now. Exhibit 1 shows Chinese year-over-year GDP growth rates since Q4 2008 along with a selection of hard landing headlines, for your enjoyment.

Exhibit 1: The Often-Feared, Yet-To-Be-Seen Chinese Hard Landing

Source: FactSet, China quarterly GDP growth rates (y/y), Q4 2008 - Q3 2014. You can see the headlines for yourself here, here, here, here, here, here, here, here, here, here, here and here. Though, you may not want to. We found more, but fitting them all would have been tough.

On a more forward-looking note, The Conference Board's Leading Economic Index for China (LEI) has surged of late, rising 0.9% in September. This follows 1.3% and 0.7% gains in July and August and marks the seventh consecutive rise.

Europe seems to be where most fearful headlines originate. And we'll not argue eurozone growth is hot, but it needn't be when most investors seem to think it's an economic vortex about to drag the world down. Thursday morning, October's Flash eurozone Composite PMI showed a slight increase in the percentage of firms reporting growth-to an expansionary 52.2 from September's 52.0, easily beating analysts' forecasts for a slowdown. In fact, it beat every forecast Reuters obtained in a poll of economists, further illustrating how dour folks are about the eurozone. More headlines seem fixated on arguing over which eurozone nation is actually Europe's sick man than they appreciate the figures aren't negative across the board. Eurozone LEI dipped in September, but the primary detractors were sentiment gauges, among the less predictive components.

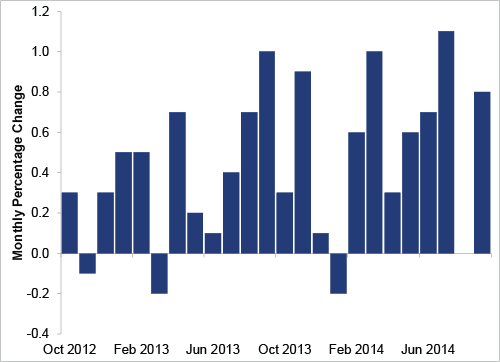

Even if there is a dip, there is scant evidence weak eurozone growth or even a recession will cease the expansion or bull market. This bull market endured an 18-month long eurozone recession while world stocks rose 34%. Today, we don't have a eurozone recession, and figures from the UK and US show continued growth. UK Q3 GDP grew a healthy 0.7% q/q (2.8% annualized), a touch slower than Q2's 0.9% q/q clip, but respectable nonetheless. US GDP won't be published until next week, but arguably more important for stocks was Thursday's news US LEI rose 0.8% m/m in October-reaccelerating from August's flat reading and the seventh positive read of 2014's nine to date.

Exhibit 2: The Conference Board US Leading Economic Index, Monthly Percentage Change

Source: FactSet, as of 10/24/2014, October 2012 - September 2013.

When you actually scan the data, there are some negatives. But most of them are one-offs, like US retail sales falling -0.3% m/m in September after seven straight monthly increases. Or German exports falling sharply in August, but from all-time high levels set in July. The big picture is that the majority of the world is growing, against a backdrop of fears it won't. Overall, that is the same recipe resulting in five-plus years of bull market thus far. We see little reason to think that won't continue going forward.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Surprise! It's the eurozone. We know! Who'da thunk it?

[ii] Investors underpinning strategy with this list are setting themselves up for disaster.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today