Personal Wealth Management / Market Analysis

The Lay of the Land Up North

As our Canadian friends celebrate a holiday, what better time to check in on Canadian stocks?

Happy Canada Day! Between the holiday and a Canadian team being in the Stanley Cup finals for the first time since 2011,[i] what better time to celebrate our friends in the Great White North with a check in on Canadian stocks? Especially after they were again among the developed world’s best-performing nations in Q2, finishing June up over 20% year to date.[ii] What is behind the party? Will it last? Read on!

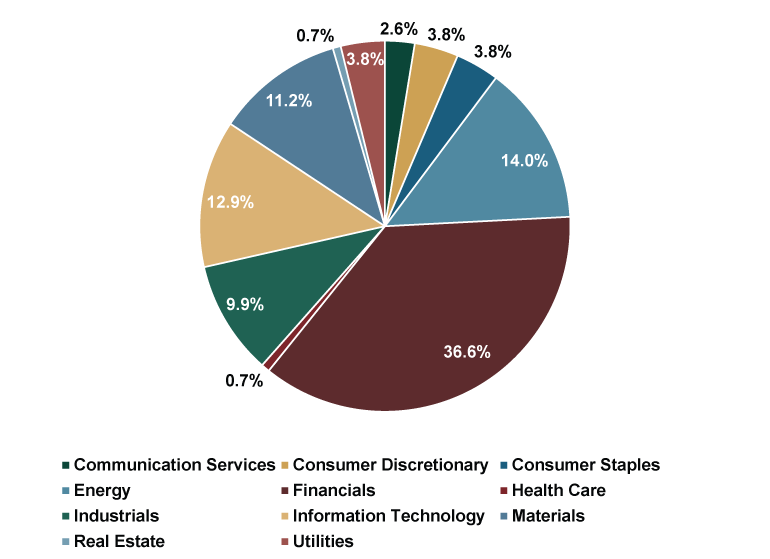

If you have been following Canada’s battle against COVID, you might wonder how Canadian stocks are rockin’ and rollin’ while the country’s lockdowns are among the Western world’s longest lasting. The answer, in our view, is simple: Markets are looking a lot further out than lockdowns and reopenings, allowing sector trends to enjoy greater influence over returns. Year to date, that has been a mighty tailwind for Canada. Its market cap is about half Energy and Financials, which happened to be the first half’s top-performing sectors globally in 2021’s first half. Those two sectors comprise just 17% of MSCI World market capitalization.[iii] Exhibit 1 shows the full breakdown, with apologies to those of you who believe pie charts are a sin against graphic design.

Exhibit 1: Is It a Pie or a Hockey Puck?

Source: FactSet, as of 7/1/2021. MSCI Canada sector weightings at market close on 6/30/2021.

It isn’t just Energy and Financials’ big relative size that boosted Canadian returns versus global markets—both Canada’s Energy and Financials sectors outperformed their MSCI World sector counterparts. Canada’s oil industry is a bit funky. Canadian oil prices tend to trail the US and global benchmarks, while extraction costs in Canada’s oil sands are relatively high. As a result, when oil prices fall, Canadian Energy companies usually take it on the chin harder. But when they recover, Canadian producers can benefit disproportionately from the relief rally. That all flows through to Canadian bank earnings, given their high credit exposure to the oil industry.

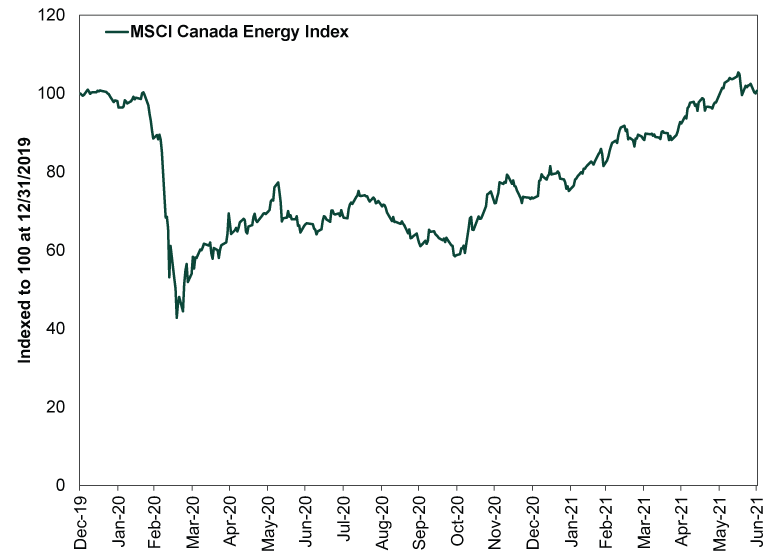

This time around, given its geographic proximity, we suspect Canadian oil got an extra boost from the US’s swift post-lockdown demand jump. Lest you get too excited about any of this and want to chase heat, however, consider Exhibit 2 and note that Canadian Energy stocks only just reclaimed their pre-pandemic high. That journey took much longer than global stocks overall. Then ask whether oil’s current supply/demand imbalance is likely to have much surprise power looking forward, given a) it has been widely discussed for months and b) producers globally have ample spare capacity.

Exhibit 2: Canadian Energy’s Long, Slow Trip to Breakeven

Source: FactSet, as of 7/1/2021. MSCI Canada Energy Index return with net dividends, 12/31/2019 – 6/30/2021.

Looking forward, a new headwind might loom courtesy of political uncertainty, too. Since the last election in October 2019, Canadian stocks have benefited from gridlock. Prime Minister Justin Trudeau heads a minority government, incapable of passing anything without external support. But lately, some polls suggest his Liberal Party could improve their standing if an election were held, as Trudeau's approval rating has improved tied to the COVID vaccination campaign and the government’s fiscal response—one of the rare pieces of major legislation to squeak through. He may—and we emphasize may—be able to gain a majority if the election was today. It isn’t scheduled until 2023, but now there are rumblings that Trudeau will try to seize the moment by dissolving Parliament in August, starting a five-week campaign for a September snap election.

Now, approval ratings aren't ironclad and polls have had a bad run in recent years, so we don’t think it is a given that the Liberals’ higher popularity will bring significantly more seats in Parliament. Canadians vote by constituency (or “riding,” if you would like to use the official lingo), rendering national polls less meaningful than they might otherwise seem. But if Trudeau calls a snap contest and ekes out a majority, it could diminish gridlock and stoke uncertainty. Add that to the fact we don’t expect value stocks or Canada’s biggest sectors to lead over the next 12 to18 months or so, and in our view, Canada’s big first-half boom probably falls into the ‘twas nice while it lasted category.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today