Personal Wealth Management / Market Analysis

The Often-Rumored, But Rarely Seen Grexit

Politicking over a Greek exit from the euro resumes.

We don't think German Chancellor Angela Merkel is pointing out the exit to Greece here. Photo by Milos Bicanski/Getty Images News.

According to an unnamed source cited by German newsmagazine Der Spiegel[i], German Chancellor Angela Merkel may play chicken with Greece. Unlike her 2012 statement that there was no alternative to keeping Greece in the euro, this mysterious insider claims there is now an alternative supported by the Merkel government: Booting them, should the anti-austerity Syriza win Greece's January 25 snap election and press their demands for relaxed austerity and a third Greek default. Now, with sentiment toward the eurozone so black, the mere mention of Germany backing Grexit, however unreliably sourced, stoked speculation the euro crisis had returned. The theory presumes the following:

- That Syriza will win the Greek snap election.

- That it will follow through on its campaign promises.

- That this unnamed source is actually correct and represents the eurozone position broadly.

- And that Grexit would be Very Bad for the euro's future, despite there being few signs to date.

Interested in market analysis for your portfolio? Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

However, this seems like a time for a pause and some perspective. You see, we've seen this movie before. Talk of allowing Greece to leave the euro was political bluster then, and we are darned skeptical it is so different this go round.

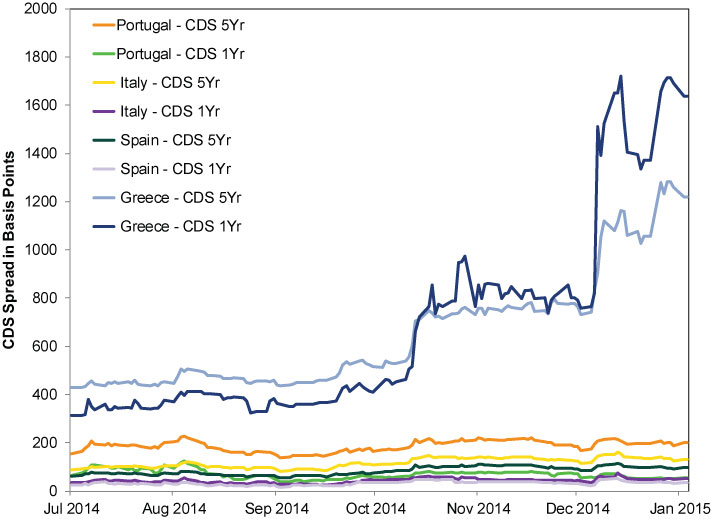

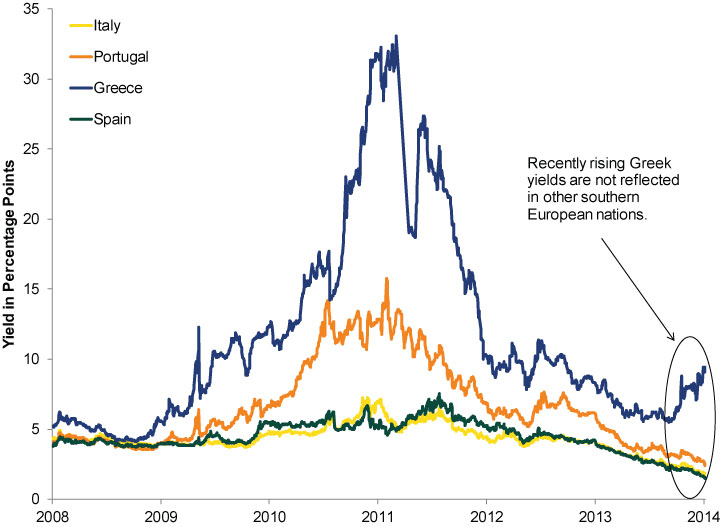

Here is at least one thing the theory gets right: Signs of contagion are sparse. The cost of buying insurance against a Greek bond default is rising sharply, but basically nowhere else in Southern European have sovereign credit-default swap spreads budged. (Exhibit 1) 10-year bond yields are down outside Greece. (Exhibit 2)

Exhibit 1: Southern European Sovereign 1 & 5 Year CDS Spreads

Source: FactSet, as of 01/05/2015. 06/30/2014 - 01/05/2015.

Exhibit 2: Southern European 10-Year Bond Yields

Source: FactSet, as of 01/05/2015. 12/31/2008 - 01/05/2015.

This all seems perfectly rational, given Greece has long sought an intentional third default we have labeled, ThreefaultTM.[ii] If you are a business insuring against default from a nation that has defaulted twice in the last three years, and that nation is arguing they should go for the trifecta, you should probably charge more for that insurance. And there is just no sign that Portugal, Spain, Italy or really any other place in the eurozone is in the same boat as Greece.

But the Spiegel report and others suggest the lack of broad reaction across the eurozone is a risk-you read that right-because it is giving Merkel and other eurozone officials false confidence. The mistaken belief that the game was fundamentally changed by the European Stability Mechanism (ESM), the permanent bailout facility created in reaction to the debt crisis. They suggest she and other officials have undue confidence in the ESM's ability to backstop an imperiled eurozone sovereign should a selloff follow a Greek boot. Hence, contagion. One commentator claimed Grexit could amount to "Lehman Brothers squared."[iii] Another fantastically suggested there is "a whiff of 1914" in the politicking that could end very badly (though there is no mention of who is this go-round's Archduke Franz Ferdinand). Some even attribute the euro's fall to its lowest level against the dollar since 2006 as a sign the currency's existence is in doubt. Which overlooks existing negative interest rates on certain deposits and short-to-medium term sovereign debt, the potential for more ECB action and the fact the dollar's strength isn't limited to the euro. Seems like correlation without causation.

Let's be clear: Rumors of Germany being willing to push Greece out have existed for literally years. Here is one from the same source as the current, dated November 12, 2011. Here is another from The New York Times, dated May 17, 2012. Oh and here is one more from Der Spiegel, dated July 23, 2012, again citing an unnamed source within Merkel's government claiming Germany was about to cut off aid to Greece, triggering a euro exit. Sound familiar? For what it's worth, Merkel is denying the report today, suggesting her position hasn't changed.

Now then, we wouldn't be surprised if the media's unnamed insider wasn't saying something that has a grain of truth to it. Which is really just the nature of politicking, and all the media is reporting said politicking at face value. Some have even cited that this could be mere bluffing (though most claim that's dangerous in its own right). But consider: Merkel could be trying to set herself up for a bit of a win-win regarding Greece. She has taken a ton of heat domestically over an allegedly soft stance on Greece. By leaking that Germany may take a hardline position, it could not only aid her constituency's view of her, but also give support to current Greek Prime Minister Antonis Samaras' claims that electing a Syriza government would spell an ouster from the euro for Greece, something Greek voters seem skeptical of lately. Even if that fails and Syriza is elected, this could also be Merkel warning them to moderate their position, which they'd probably have to do anyway, as they stand little chance of winning a parliamentary majority on their own. Polls recently show them with a very narrow lead, but this predates former Prime Minister George Papandreou announcing he'll split from the socialist PASOK party and form a new movement, which could siphon some of Syriza's supporters.

Long and short, there is a lot of sound and fury over some pretty speculative reporting, but in our view, this is much ado about very little.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Who we presume is "familiar with the situation."

[ii] We didn't really trademark this, that's a joke.

[iii] This is an erroneous reference to the role Lehman Brothers' failure played in 2008 that seemingly hinges on the notion it was bad because Lehman was Too Big to Fail.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today