Personal Wealth Management / Economics

The Other Volcker Rule: State Budget Transparency

Three cheers for state budget transparency, but even if former Fed head Paul Volcker's crusade doesn't win, the risks for investors seem small.

Former Fed head Paul Volcker has fought a lot of things in his time. Inflation. Meddling Congressmen. Banks' proprietary trading. Shady state budgeting joined the list last week, courtesy of the Volcker Alliance's new report, "Truth and Integrity in State Budgeting," which shed light on state houses' accounting gimmickry, investigated the long-term impact and called for reform. Most of the conclusions are sociological, but buried within-and spotlighted in the media coverage-were long-running fears of crashing municipal debt markets, big unfunded liabilities and constant budget-plugging holding back growth. Don't get us wrong, consistency and transparency in state budgeting would be grand, but the economic and market impact either way is likely negligible.

The report seems overall less concerned with the amount of red ink on state ledgers than with the lack of consistency and transparency across state budgeting practices. Forty-nine states have balanced budget laws. Vermont, which doesn't, follows the herd. Yet there is no uniform definition of a balanced budget, beyond the fact spending can't exceed revenue, leaving lots of wiggle room for states to use accounting tricks to match inflows and outflows on paper, even if they don't in real life. They'll shift the timing of payments and receipts between fiscal years, float long-term bonds to finance near-term projects, delay pension and benefits contributions and cover recurring costs with nonrecurring revenue. Per the report, this lets huge debts stack up, forcing perpetually cash-strapped states to get creative when it's time to pay the piper. These long-term obligations often accrue off-budget, so they're out of sight, out of mind. State legislatures often don't have the full picture and thus debate budgets with a short-term focus. The report says practices like these "preclude accurate, informed consideration of policy tradeoffs," which is fancy talk for "prevent full debate and tough choices." Per the report, this all raises the risk of state bond defaults, balloons pension deficits and jeopardizes economic growth with "stop-and-go" funding for vital programs.

Volcker's solution is one we'll raise a glass to: Getting everything out in the open so politicians and the public can see what's what and debate reform, allowing investors to more accurately assess the risks. The report compiled detailed records for three states-California, New Jersey and Virginia-showing the various accounting tricks and how they have (or haven't) addressed problems that arose. The ultimate goal is to compile and publish the full monty for all 50 states. To which we say, hear, hear! As the report notes, there is no one source for state financial information. Many receipts and expenditures flow through agencies, which issue their own debt and have their own funds-and use their own pet tricks to balance the books when duty calls. Getting the full 411 on revenue, expenditures, debt and funds requires a scavenger hunt, spreadsheet and calculator.[i] Heck, sometimes even states don't know how much money they have. A uniform, central repository would make life easier for states and muni bond investors alike. Investors would have more information, credit ratings agencies would have even less influence and markets would be able to price information in much more efficiently. Think of it as the state equivalent of the eurozone injecting consistency into national accounting.

But other than that, the implications are mostly political. The alleged economic risks inherent in opaque state budgeting seem overstated to us. Take the notion of a state bond default crisis. It is entirely possible a state or three could encounter tough sledding when tax revenues fall during a recession. No state has defaulted since the Depression, but infrequent doesn't mean impossible. Even in normal times, default is possible, though odd-bankruptcies of the sovereign and corporate variety usually take place after downturns, not before. But markets know state finances vary. They know, for example, that New Jersey is not Texas. California is not Florida. Just as muni markets knew Detroit, Stockton and the other 48 municipalities declaring bankruptcy since 2010 are not like the rest of the $3.6 trillion muni bond market. The likelihood of some chain reaction is incredibly low. Default would be bad for bondholders left with devalued IOUs, but it isn't like state spending would just stop. Nor does defaulting on a few issues equal defaulting on all bonds. You'd probably get some state income tax hikes, but if California could endure those in 2013 without derailing growth, that isn't necessarily the biggest headwind in the world.

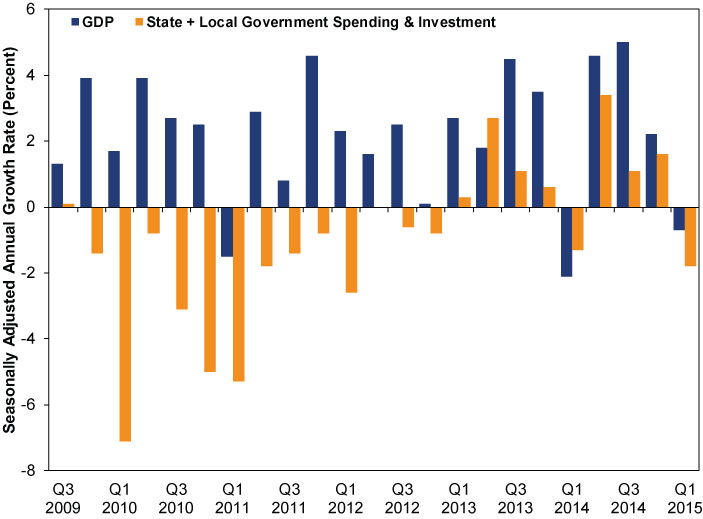

As for the economic impact of stop-and-go program funding, we reckon it is tiny-tough for those impacted, but likely not an economic swing factor. In California, for example, Governor Jerry Brown once proposed plugging the budget by closing state parks. Annoying for the state's hikers, campers and other outdoor enthusiasts, including some of your friendly MarketMinder editors! But probably not a recession trigger. State and local government spending has fallen in 14 of 23 quarters since this expansion began, sometimes by a lot (Exhibit 1). It did not tip the scales. There probably is some benefit to finding savings through long-term efficiency gains rather than ad-hoc plugs-seemingly the Volcker Alliance's goal. But the status quo isn't so terrible.

Exhibit 1: Quarterly GDP and State/Local Spending Growth in This Expansion

Source: Bureau of Economic Analysis, as of 6/12/2015. Percentage change in real GDP and state and local government spending and investment, Q3 2009 - Q1 2015.

Finally, as to unfunded liabilities, states aren't powerless to address these. Some, like Kansas, have authorized "pension obligation bonds" to fill funding gaps, presuming future earnings will exceed today's ultra-low borrowing costs.[ii] Other states have tweaked some once-generous payout rules, like that extra 13th month of benefits Detroit's pensioners used to receive when the fund's annual return exceeded its long-term average target. Illinois recently addressed its own creeping pension issues by adjusting cost of living calculations, the retirement age and benefit caps. Small tweaks like that can massively improve a fund's long-term viability. Cuts can be hardships for those directly impacted. But the broader issue simply isn't a severe macroeconomic risk.

Still, we're keen to see how this all shakes out, because we are oddly fascinated with byzantine budget trickery.[iii] But we reckon this is about where the broad interest for investors ends.

[i] Maybe a private detective, too.

[ii] Obviously there are pros and cons here, and we'd be remiss not to point out that Illinois is presently dealing with some of the drawbacks. But it is a solution nonetheless.

[iii] Hence our endless obsession with Greece.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today