Personal Wealth Management / Economics

The ‘Retail Recession’ Label Doesn’t Fit

Department stores' recent woes aren't a sign the US economy is headed for recession.

It was some department stores' turn in the Q1 2016 earnings season spotlight this week, and to say their results were weak understates the media reaction pretty dramatically. Declining sales and profits led to cries the US is in a "retail recession" and assertions the consumer is tapped out-bad signs for US growth looking forward. But we'd humbly suggest that is incorrect. A recession is a broad-based decline in economic output. This is more a story of narrow, virtually anecdotal data points and a shift in shopping habits-away from department stores and towards online and specialty retailers. Despite some retailers' recent woes, there is ample evidence US consumers are in fine shape, and that the economy is not headed for recession anytime in the foreseeable future.

On Wednesday, Macy's reported Q1 sales fell over -7% y/y while earnings tumbled -29% y/y. The following day, Kohl's said Q1 year-over-year revenues fell more than expected and earnings slid -50%. The carnage continued after market close on Thursday when Nordstrom reported Q1 earnings contracted -61% y/y, badly missing estimates (though sales grew about 1%). All lowered their guidance for full 2016 results. Friday, JC Penney joined the "party," also posting poor results.

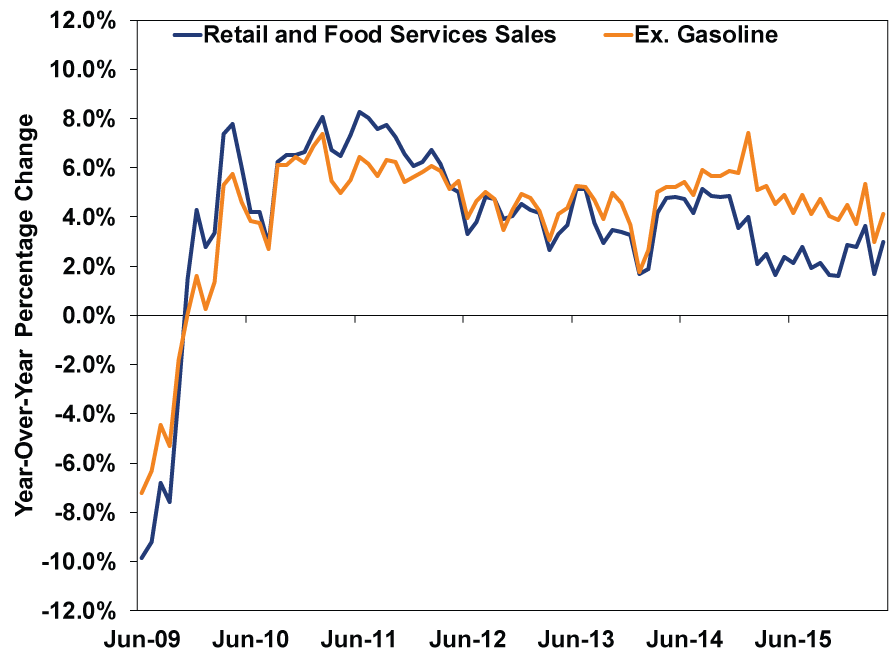

To hear the media tell it, this is a sign consumers are materially tightening their belts. And, with consumer spending accounting for roughly 70% of US GDP, they suggest it signals a weak economy-and maybe an approaching recession. That narrative, however, is based on only a handful of companies, and is pretty darn odd when you square it up against broader economic data like, we dunno, US retail sales. April's data happened to be reported Friday, and beat estimates with 1.3% m/m growth (3.0% y/y). And, as Exhibit 1 shows, this isn't a new thing-retail sales are growing at a fine clip, which is especially clear when you remove the negative influence of falling gas prices by excluding gas station sales. (Which reversed in March and April.)

Exhibit 1: Retail and Food Services Sales and Sales Ex. Gas Stations

Source: Federal Reserve Bank of St. Louis, as of 5/13/2016. Seasonally adjusted retail and food service sales and sales excluding gasoline, June 2009 - April 2016.

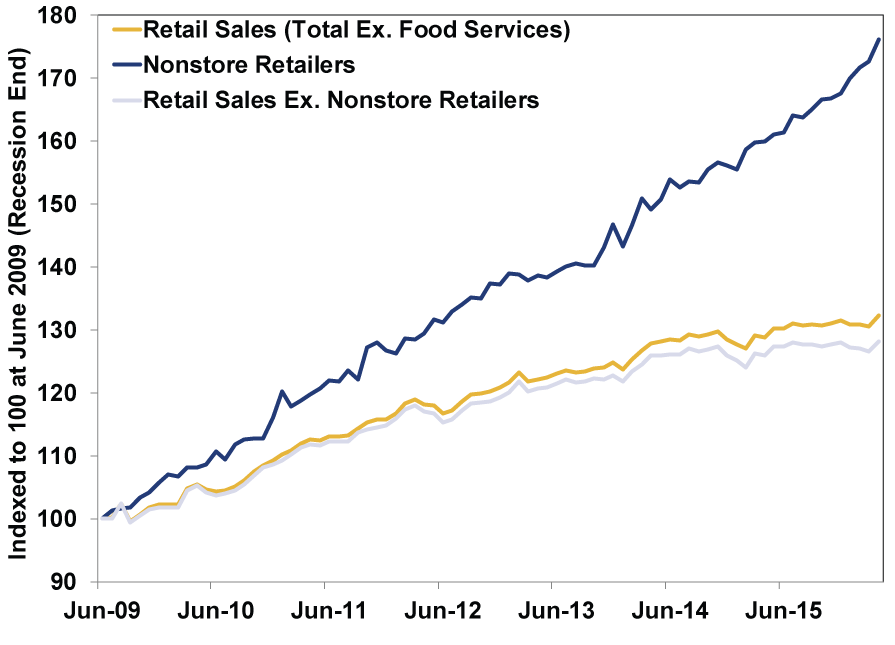

But within these retail data are clues to what's really behind these big retailers' earnings issues-and it isn't a tapped out consumer at all. It is in part just competition from newer, specialty retailers. But also, notably, nonstore retailing-a technical term covering internet and catalog retailers-has vastly outgrown brick-and-mortar sales throughout this expansion. Exhibit 2 shows the growth in retail sales in goods (which excludes food services sales), nonstore sales and goods sales ex. nonstore sales since the 2007-2009 recession ended.

Exhibit 2: Online Shopping is Growing By Leaps and Bounds

Source: Federal Reserve Bank of Saint Louis, as of 5/12/2016. Total retail sales excluding food service, nonstore retail sales and total retail sales minus nonstore sales, 6/1/2009 - 3/1/2016.

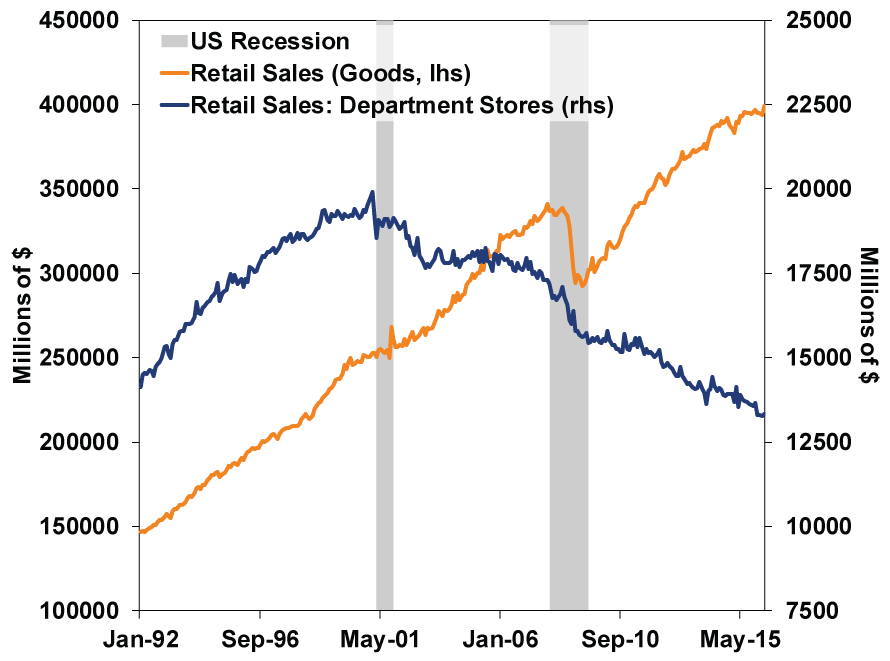

And, as you might expect after viewing Exhibit 2, S&P 500 internet and catalog retailers' profit growth has been quick. In the last three quarters, earnings have grown 143.0% y/y, 30.2% and 58.0%. This isn't a new trend, though. It's been happening for years because shopping online is, to many, much more convenient than trekking out to the local mall. And when folks do venture out, long-term trends show they are increasingly less wont to shop at big department stores. (Exhibit 3)

Exhibit 3: Declining Department Store Sales Is a Long-Term Trend

Source: Federal Reserve Bank of Saint Louis, as of 5/12/2016. Total retail sales (goods only) and retail sales at department stores, January 1992 - April 2016.

So why are so many fretting faltering brick-and-mortar store sales now? It's likely a manifestation of recent widespread recession fears.

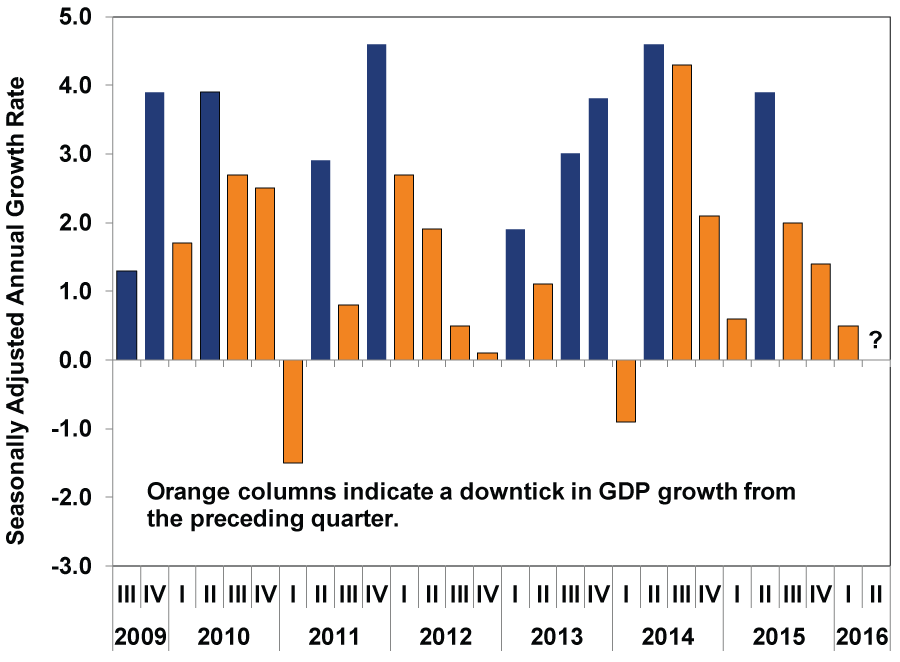

But these fears are unfounded. It's true US GDP growth slowed to 0.5% annualized in Q1, stoking weak economy fears. Folks fret this means the US is near recession by extrapolating the slowdown into the future, but that isn't how economies work. Growth rates typically wobble throughout expansions, and there is little evidence Q1's slow growth is a harbinger of worse to come. In this very expansion, growth has slowed or briefly contracted a handful of times, yet these periods did not foreshadow a recession. (Exhibit 4)

Exhibit 4: Slowing GDP Doesn't Necessarily Mean Recession Ahead

Source: Bureau of Economic Analysis. US GDP, seasonally adjusted annual rate, Q3 2009 - Q1 2016.

Forward-looking economic data don't suggest weakness looms. Loan availability is a key ingredient in economic growth-hence why tight credit conditions often precede recessions. Yet today, lending is growing nicely and the yield curve spread-long term rates minus short-term-is positive. Banks typically borrow short term (deposit accounts, overnight funding, etc.) and lend long term, so long rates exceeding short means lending is profitable. Profitable lending stimulates loan growth, providing capital businesses need to grow. This is one reason why The Conference Board's Leading Economic Index remains high and rising, and in its nearly 60-year history a recession has never occurred while this has been the case.

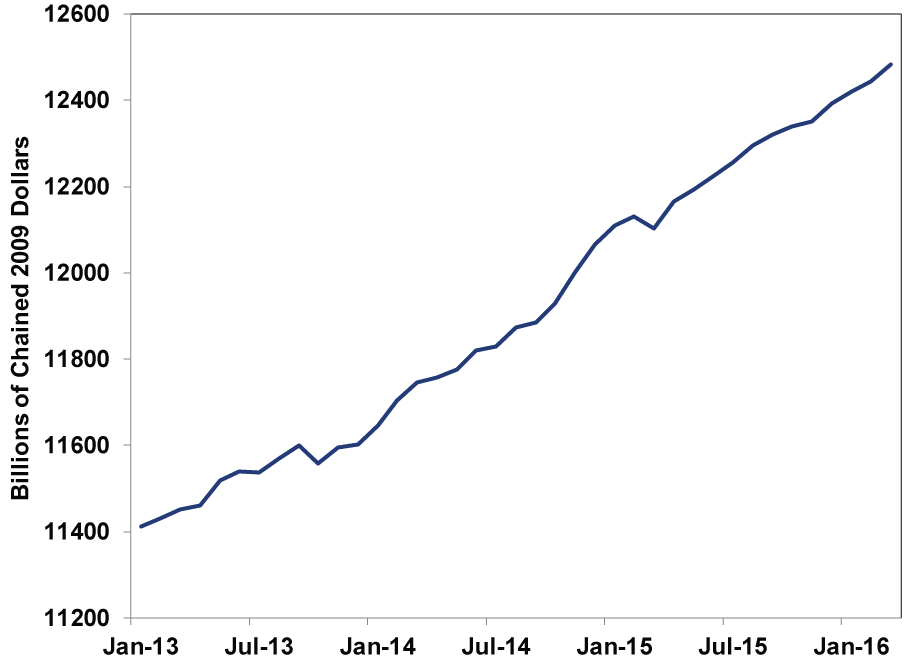

Besides, falling consumer spending tends to result from economic downturns, not cause them. Most spending is for housing, food, utilities, transportation, basic household goods-things people have little leeway to cut back on. Of course, when the economy turns down folks tend to spend less on splashy vacations and other non-necessities, but that isn't happening right now. The S&P 500's Hotels, Restaurants & Leisure industry's earnings grew over 13% y/y in Q1-despite a -122% drop at one trendy Mexican food restaurant that had some widely known issues with food poisoning. This highlights another reason you needn't fret this week's weak retailer results: Spending on goods is just one component of overall spending. Services accounts for the lion's share of the total. Either way, the biggest driver of consumption growth is real disposable income, which is growing quite nicely these days. (Exhibit 5). There is just no sign US consumer spending is on shaky ground, despite the media's take on a handful of brick-and-mortar retailers posting bad earnings.

Exhibit 5: Disposable Income is Rising

Source: Federal Reserve Bank of Saint Louis, as of 5/12/2016. Seasonally adjusted real disposable personal income in chained 2009 dollars, 1/1/2013 - 3/1/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation, Sell America, US National Debt and More - June 20262026-06-01

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US Jobs, Estate Planning

2026-06-01

2026-06-01 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 25 - May 292026-06-01

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today