Personal Wealth Management / Market Analysis

The UK’s Brexit Wish List

What does Prime Minister Theresa May's recent speech mean for Brexit?

Will Brexit be hard, or will Brexit be soft? This question has dominated Brexit chatter since last June's vote, and on Tuesday, Prime Minister Theresa May gave us an inkling of an answer: She intends to withdraw the UK from the EU's single market, fitting the textbook definition of a hard Brexit. Then again, within the 12-point outline of her administration's starting point and negotiating priorities were several provisions to soften the blow, illustrating the danger of relying on narratives and snappy jargon for your investing cues. Now, a speech isn't a binding agreement, and talks-which have yet to begin-could always yield an unexpected result. However, May's speech does add more information and clarity than we had before, and less uncertainty lets markets start pricing in the future.

Much of May's focus was sociological, from immigration control-a major theme during the referendum campaign-to protecting workers' rights. Yet there were some notable items for investors, including May's desire for new free-trade agreements, not only with the EU, but other countries as well. She also revealed Parliament would weigh in on the final deal, and the eventual agreement's rollout would be gradual and deliberate to ensure a "smooth and orderly Brexit." In other words, sudden, immediate surprises are unlikely, giving markets ample time to digest the actual rule changes.

Because May stated the UK would forgo single market access, many outlets concluded Britain chose the "hard" Brexit path-scrapping what's on the books and starting fresh-rather than the "soft" Brexit where the UK and EU reach a modified arrangement while keeping much of the status quo intact.[i] A blank slate inevitably means more unknowns, so many critics argue a hard Brexit would hurt the UK economy, since unknowns are apparently automatically bad (and, according to the narrative, presumably mean high trade barriers). The negative feedback is voluminous: Some say May "wants to have her cake and eat it" and her speech added more uncertainty. Others worry it will cause more corporate insolvencies and hurt the Brits more than their Continental counterparts. Already, some experts assume long-term GDP figures will suffer based on straight-line math. The pound's fall over the weekend before May's speech allegedly signaled currency markets' disapproval of a hard Brexit-so commence freak-out.

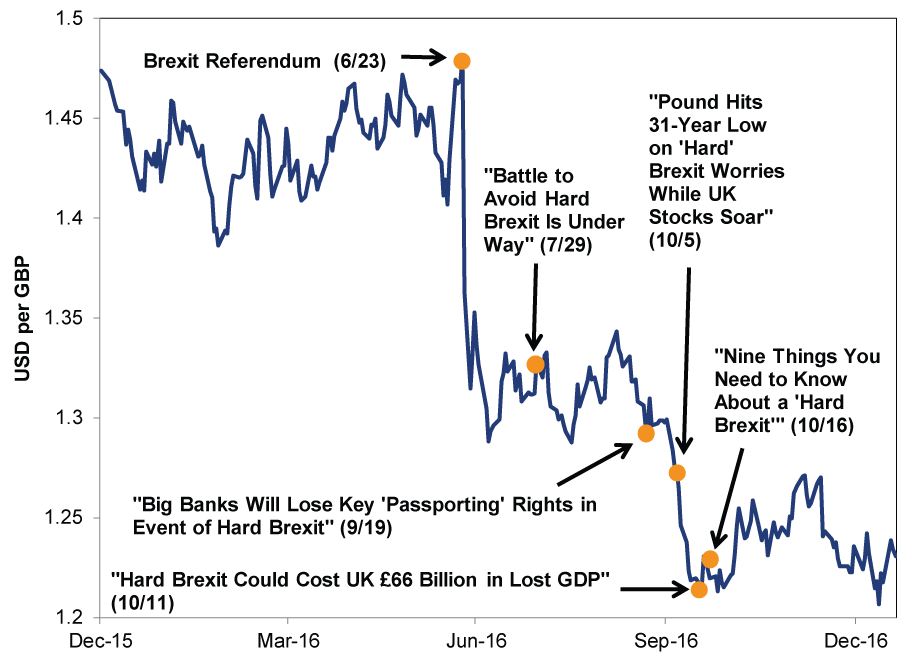

However, these warnings sound eerily similar to the economic doomsday scenarios many warned would immediately follow a vote to leave. The projected recession and extended market turmoil never arrived, and while we don't recommend using the past to forecast the future, we aren't ready to call May's speech an impetus for economic disaster just yet. Plus, following May's speech, the pound actually rose, despite myriad concerns to the contrary. Far be it from us to read much into one day of market movement, but if headlines are banging on about how a well-telegraphed event will definitely cause one thing to happen, and then something else occurs, it's a reminder that markets move before widely known events, not after. See Exhibit 1 for more evidence that a hard Brexit scenario isn't sneaking up on anyone.

Exhibit 1: "Hard Brexit" Isn't Breaking News

Source: FactSet, as of 1/19/2017. From 12/31/2015 - 1/19/2017. Headlines, in chronological order, are from here, here, here, here and here.

Then again, all this hard/soft Brexit talk oversimplifies matters and overlooks nuance. We've long suggested shedding labels and focusing on how the UK's trade relationships would change, which likely remains unknown until negotiations end. We still don't have some key answers: Will the UK still be able to trade freely with Europe? Will UK service firms still be able to do business across the Channel? Will Britain ink new free-trade deals with other nations, like the US? All still mysteries today-and will be for a while-but May's speech does lay some groundwork about the UK's ambitions.

And it shows the silliness of the prevailing narrative. Let's say both the UK and EU acknowledge a big, sweeping free-trade deal would benefit both sides and agree to one. The UK would be out of the single market-hard Brexit! But wait, a "comprehensive, bold and ambitious free-trade agreement" sounds kinda like a soft Brexit. Either way, in practice, the result could be very similar: Goods and services flowing between the UK and EU with minimal friction. The differences are largely semantic, and semantics aren't economic negatives. Another potential positive: A hard Brexit could free up services trade in a way the EU's single market currently doesn't. Also, being unbound from the EU means Britain can negotiate bilateral trade deals, since it wouldn't have to get all 27 other nations to buy in. UK officials are already talking to their counterparts in India, and there is interest from Canada, the US, Australia and New Zealand as well. Just as negative ninnies forecast the worst-case scenario of this "hard" Brexit, we could envision a pretty good one.[ii]

Again, don't make too much of May's speech or call it a sign of things to come. Rather, take it for what it is: The UK government establishing its priorities before formal Brexit negotiations begin and giving markets a starting point for determining probable outcomes. Even though there is nothing conclusive yet, these Brexit developments have been publicized and widely discussed since last June's referendum, allowing markets and investors to digest them. Whenever negotiations formally begin, we expect more of the same.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today