Personal Wealth Management / Market Analysis

The World Beyond Covfefe, Comey and GE2017

May PMIs are the latest data points confirming the global expansion.

A fresh batch of economic data-May purchasing managers' indexes, or PMIs-largely tell this tale: Businesses around the world are expanding. This isn't breaking news if you follow these monthly releases religiously, but most regular folks don't.[i] However, when media flash a story on the latest, they often pen a headline focused on a single, eye-grabbing tidbit that omits more important context and details. Focusing only on headlines or even just the one month of data usually obscures the more telling bigger picture-something we recommend investors keep in mind when consuming financial media.

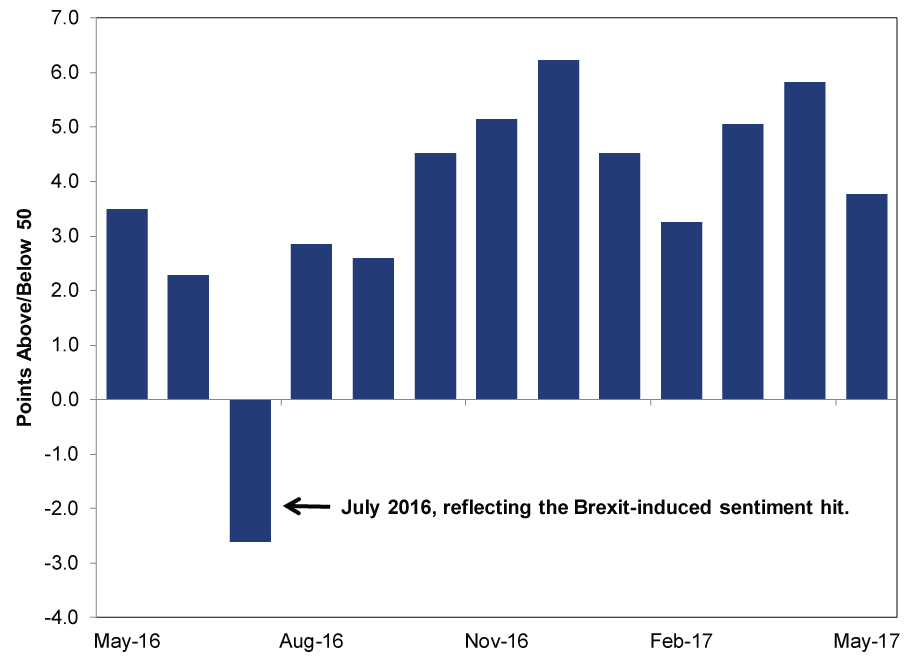

Brexit Still Hasn't Hurt UK Services

Media Reaction: The May IHS Markit/CIPS Services PMI disappointed some who had hopes of an economic rebound. Others blamed the lower reading on General Election jitters and weak consumer spending.

MarketMinder Take: While the May UK Services PMI of 53.8 was lower than April's 55.8, this doesn't necessarily mean economic growth slowed. PMIs are surveys estimating the breadth of growth, not the magnitude. Readings above 50 mean more respondents expanded in the month than contracted, but the degree is unknown. For example, fewer businesses may have expanded overall, but those that did could have grown gangbusters. More importantly, this May report is further evidence firms in the UK's largest economic sector haven't stopped growing despite rampant fears Brexit was going to slam business activity. As IHS Markit noted, input prices eased to an eight-month low in May as headwinds from the Brexit-induced weaker pound have started fading (to the extent it even impacted most services firms, which is debatable). We don't believe this trend will meaningfully reverse either, even with British politics in upheaval after yesterday's General Election. The market reaction has been rather ho-hum, especially compared to last year's short spell of negative volatility immediately following the Brexit vote. For all the talk of sterling's post-election plunge, it is basically right where it was when PM Theresa May called the election in April.

Exhibit 1: CIPS/IHS Markit UK Services PMI and Brexit

Source: FactSet, as of 6/7/2017. From May 2016 - May 2017.

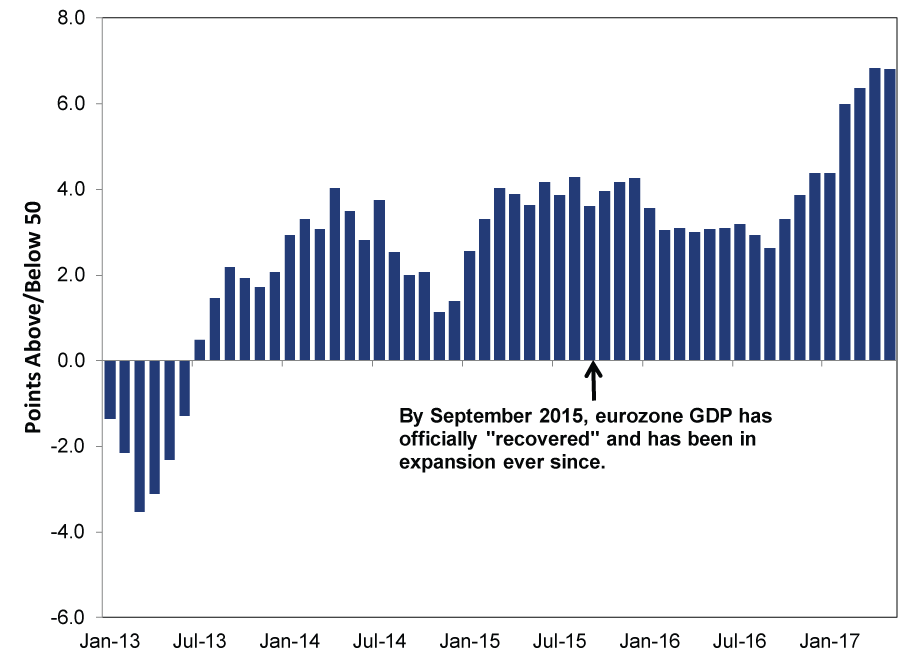

About That Eurozone "Recovery"

Media Reaction: May eurozone business activity was strong and puts "the economy on a path towards a sustained recovery." Germany and France expanded at the fastest rates in six years, though ECB central bankers are still likely to temper their optimism.

MarketMinder Take: We have no qualms with being optimistic about the IHS Markit eurozone May composite PMI of 56.8-a repeat of April's final and May's flash readings. New orders also matched April's pace, a sign further growth is likely. Along with Germany (57.4) and France (56.9), Italy (55.2) and Spain (57.2) also showed expansion, confirming the currency bloc's four largest economies are chugging along. Our only question: Why so late in recognizing this? It isn't breaking news. Even at the start of the year, some pundits worried political developments could stymie growth, a fear we believed was vastly overwrought at the time. Eurozone GDP has risen 16 straight quarters, composite PMI has exceeded 50 since July 2013 and the economy overall has been in expansion since mid-2015-yet many experts are just starting to acknowledge this, a bullish sign sentiment still has room to improve.

Exhibit 2: IHS Markit Eurozone Composite PMI Since January 2013

Source: FactSet, as of 6/7/2017. From January 2013 - May 2017.

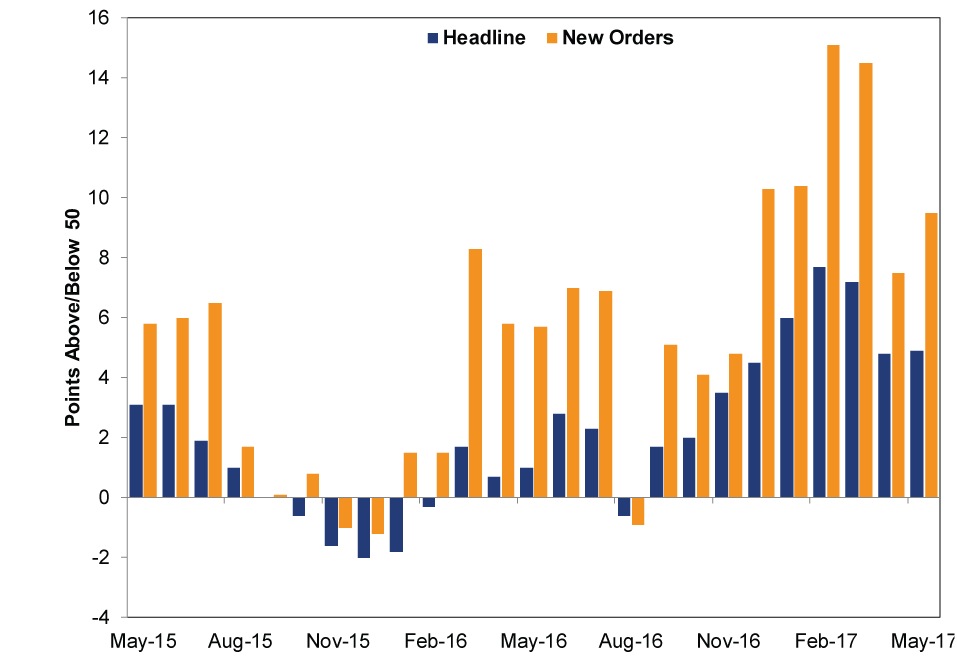

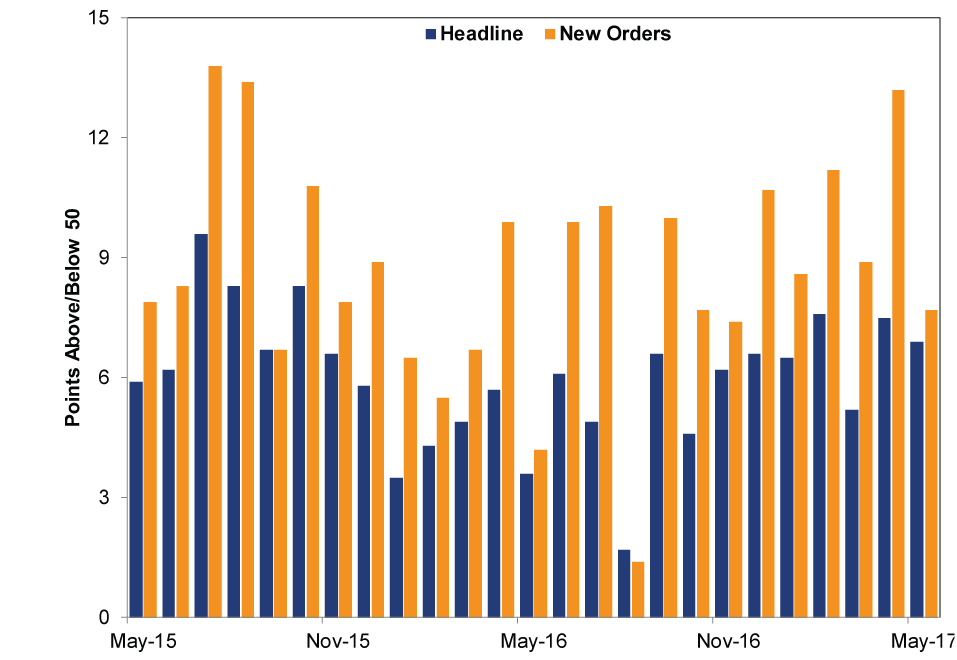

US PMIs Are Doing All Right

Media Reaction: The Institute for Supply Management's (ISM) US May manufacturing and non-manufacturing PMI elicited largely positive responses. Some analysts see manufacturing as "back into a leading position in the recovery." While the non-manufacturing PMI slightly slowed from April, others believe the economy "remains on course to recover from the disappointing start to the year" and is "on solid ground right now."

MarketMinder Take: The reactions to ISM's May PMIs were largely positive after manufacturing ticked up from April's 54.8 to 54.9 and non-manufacturing hit 56.9, slightly down from April's 57.5. Couple these expansionary reads with forward-looking New Orders-59.5 for manufacturing, 57.7 for non-manufacturing-and future growth looks likely. Expanding PMIs have been the norm for the US for a while now, manufacturing's soft patch in late 2015-early 2016 notwithstanding.

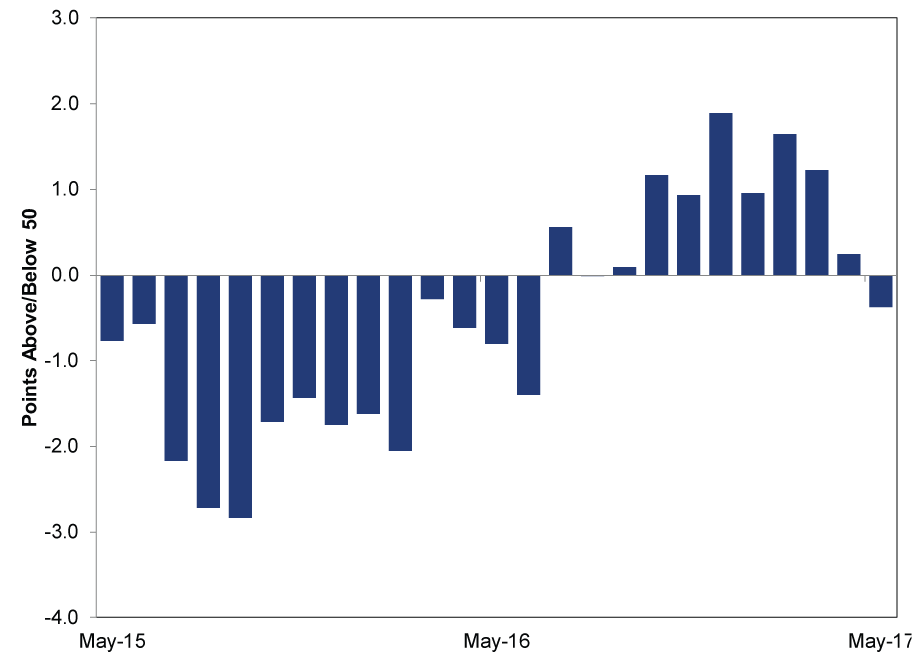

Exhibit 3: ISM Manufacturing PMI-Headline and New Orders

Source: FactSet, as of 6/7/2017. From May 2015 - May 2017.

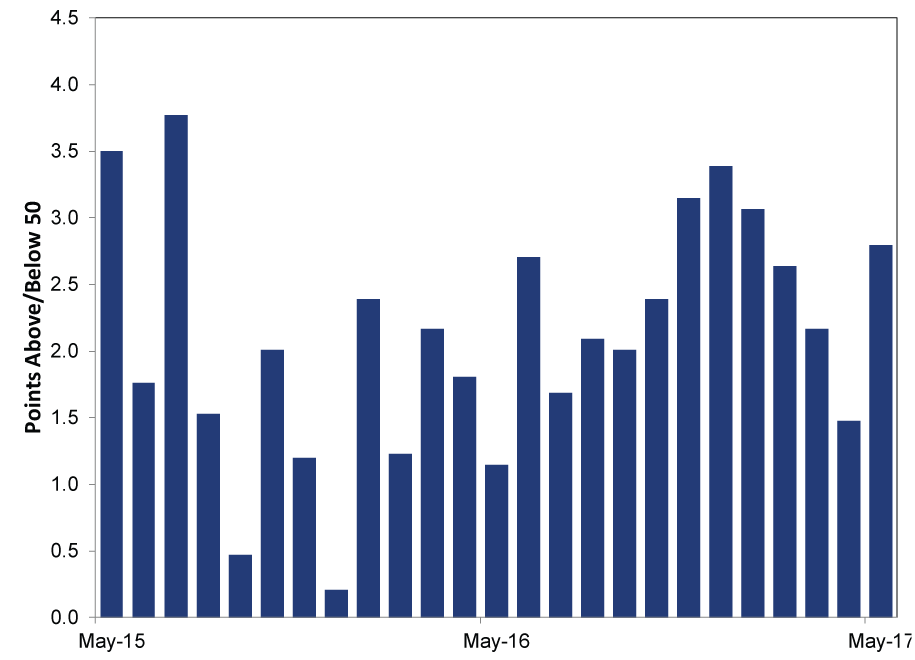

Exhibit 4: ISM Non-Manufacturing PMI-Headline and New Orders

Source: FactSet, as of 6/7/2017. From May 2015 - May 2017.

Non-manufacturing PMI covers a large swath of the US economy, so the consistent readings over 50 are evidence of a broadly growing private sector: the backbone of the US economy. Aside from some murmurs about slow Q1 GDP growth, folks seem generally more optimistic about the US economy than they were in the past-and especially compared to the UK and eurozone. This optimism can last (and escalate) for a while.

What to Make of China's Caixin PMIs?

Media Reaction: China's Caixin PMI data prompted mixed responses. After official PMIs garnered a somewhat positive reaction, the Caixin manufacturing PMI's 11-month low-and drop below 50-raised questions about the divergence. However, Caixin's services PMI, released a couple days later, hit a four-month high, and some noted the services sector "bolstered the Chinese economy in May."

MarketMinder Take: Why the divergence between the official (51.2) and Caixin (49.6) manufacturing PMIs? They don't cover the same businesses. The Caixin PMI focuses more on small- and medium-sized enterprises while official PMIs also include big state-backed firms. Smaller manufacturers face more headwinds than their larger peers-for instance, they have a harder time securing financing from the big state-owned banks. This issue is even more acute recently with China's recent push to limit "frothier" sectors and reduce financial sector risk.

Exhibit 5: Caixin Manufacturing Since May 2015

Source: FactSet, as of 6/8/2017. From May 2015 - May 2017.

But bouncy contractionary manufacturing numbers haven't stopped the burgeoning services sector (more than half of Chinese GDP)-let alone the broader economy-from growing.

Exhibit 6: Caixin Services Since May 2015

Source: FactSet, as of 6/8/2017. From May 2015 - May 2017.

Overall, these data are consistent with China's recent situation: Services and consumption are becoming larger economic drivers, and GDP growth, while slowing, has shown no signs of crashing.

And before accusing us of focusing only on the world's largest economies, consider: The JP Morgan Global Manufacturing & Services PMI-which compiles responses from over 18,000 firms across 40 countries-hit 53.7 in May, with worldwide services activity hitting a four-month high. While PMIs are just one dataset, they confirm more businesses than not are growing around the world-a bullish underappreciated positive.

[i] And for good reason!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today