Personal Wealth Management / Market Analysis

The Year in Fixed Income: A Tale of Two Halves

Corporates shine in 2016's back half and should continue to start 2017.

2016 was a tale of two halves in the bond market. When uncertainty swirled early in the year, 10-year US Treasury rates fell in July to what Global Financial Data reports was the lowest since 1786. Bond prices and yields move inversely, so given the falling rates, Treasury prices surged. However, as the year progressed, uncertainty gradually fell and rates rose. This changed everything in bonds, leading to Treasury underperformance and corporate bond outperformance. Here is a look back at the year in interest rates, and a few forward-looking lessons we can draw from it.

To flash back, in early 2016 we noted 10-year Treasury yields would likely end the year little changed from the 2.24% they began at, though we expected volatility along the way. We counseled readers not to buy forecasts of four Fed hikes, particularly given the election, which incentivized inactivity on short-term rates. While the magnitude and scope of rates' decline by July was perhaps bit bigger than we envisioned, with two trading days left, rates have rallied and are slightly up on the year. Moreover, the Fed hiked exactly once this year, after the election. That is in keeping with our expectations in January. Exhibits 1 and 2 show the year in interest rates.

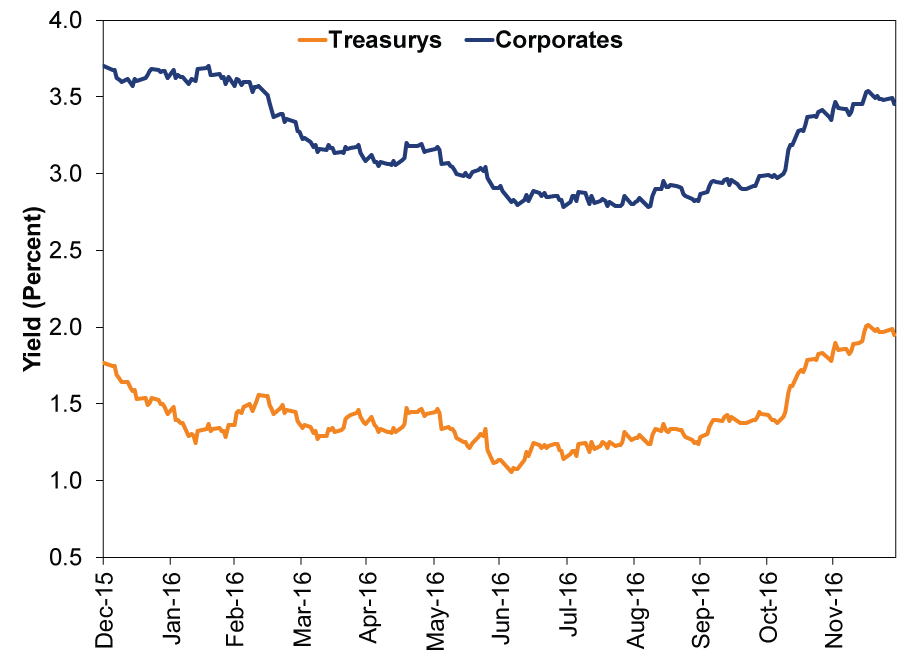

Exhibit 1: Investment Grade Yields "Smiled" ...

Source: FactSet, as of 12/29/2016. Bank of America Merrill Lynch Treasury and US Corporate Index yields, 12/31/2015 - 12/28/2016.

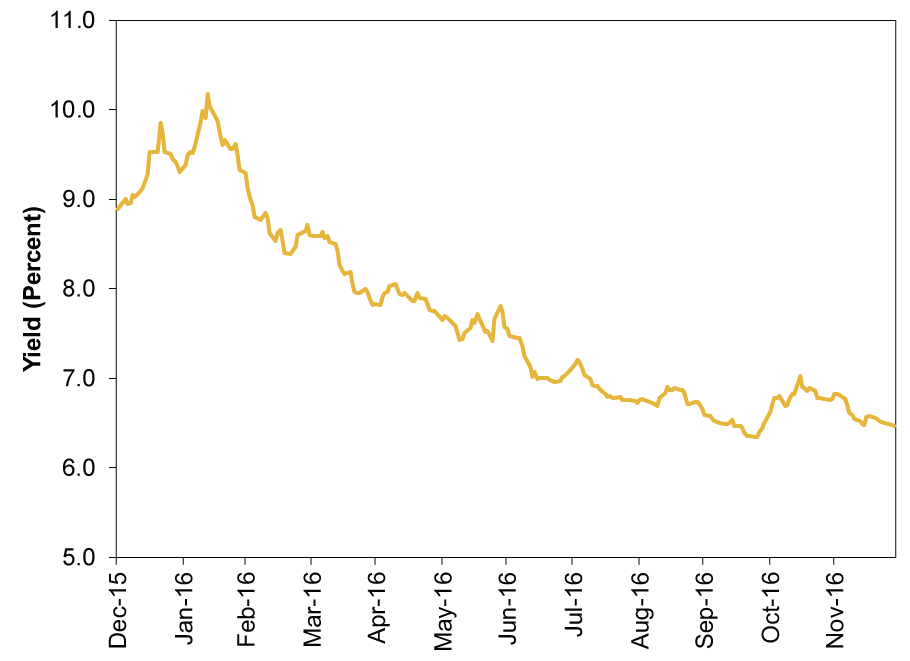

Exhibit 2: ... While High Yield Credit Risks Fell

Source: FactSet, as of 12/29/2016. Bank of America Merrill Lynch US Corporate High Yield Index yields, 12/31/2015 - 12/28/2016.

Corporates Outdistance Treasurys

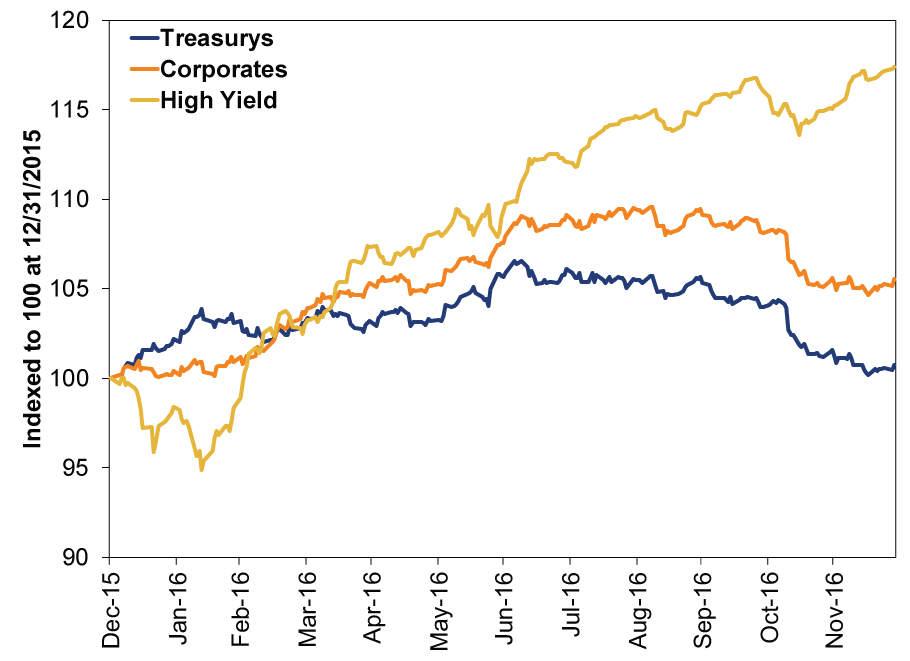

Investment grade yields "smiled" (☺) in 2016-first down and then up-driving the dichotomy between first half versus second half performance of corporates (and their high-yield cousins) against Treasurys. This had a huge effect on bond returns. Exhibit 3 shows Treasury total returns (interest and price movement-blue line) opened up a gap to begin 2016 against US corporates (orange) and US high-yield corporates (yellow). However, by the middle of March that gap had closed. Corporates outperformed from there, with the separation increasing through the second half, particularly for high yield.

Year to date, investment-grade corporates returned 5.5% versus a big fat bagel for government bonds, while US high yield corporates shined, up 17.4%.[i] So much for "so goes January, so goes the year."

Exhibit 3: High Yield Led in the Back Half of 2016

Source: FactSet, as of 12/29/2016. Bank of America Merrill Lynch Treasury, US Corporate and US Corporate High Yield Index total returns, 12/31/2015 - 12/28/2016.

A Quick Bond Basics Review

That's all what happened, but to understand why, let's review some bond basics. First, as noted at the outset, bond prices move inversely to their yield. Simple enough. If rates rise, bond prices fall and vice versa. This is because new issues with higher rates are more desirable than existing issues with lower yields.

Second, not all bonds respond equally to rising rates. Knowing how much prices move for a given change in yield-a bond's "duration"-is key. High duration means a bond's price will move a lot even if its yield just moves a little. Low duration bonds' prices won't change nearly as much for an equivalent rate change. Calculating duration can get involved, but generally speaking, the longer the bond maturity, the higher the duration.

Third, corporates and high yield often move like equities-because credit quality is tied to profitability-but usually to a lesser degree (since they are higher in the capital structure).[ii] When fears of recession or a bear market rise, corporates usually fall to an extent. After all, corporations pay interest with revenues.

Last, Treasurys are considered default "risk free"[iii] assets because they're backed by the US government (really the IRS). And the two things you can count on in life are death and taxes. It isn't surprising the sharp correction-and fears of worse-sent investors to Treasurys in early 2016, driving yields down. Falling rates caused bond prices to rise, but not equally. Longer duration bonds rose more, but higher risk corporates rose less, while high yield fell with equities.

What We Learned for 2017

With that in mind, let's consider 2016. The year started with high uncertainty about the economy, earnings, banks and politics. But this subsided throughout the year.

Corporates were aided by better earnings expectations as 2016 progressed, causing investors to pay up for them. As a result, their price increases caused them to not respond to rising rates as much as Treasurys.

Earnings began to improve by the second half and weakness was mostly confined to the oil patch. Earnings excluding Energy were down only in one quarter and are just off record highs. Full year calendar earnings for the S&P 500 are expected to be flat but up 3.6% ex. Energy. [iv] And as poor Energy comparisons drop out, the consensus outlook is for 11.5% earnings growth in 2017 (8.2% ex. Energy).[v]

For high yield, and high-yield Energy bonds in particular, the January bottom in oil prices proved especially fruitful. Fears of widespread high-yield Energy bond defaults faded. Only a 3% default rate is expected next year vs. 18.8% in the year through November, according to Fitch. Oil prices didn't need to recover per se, they just needed to stop falling. That they did recover substantially-WTI crude oil is up 45.5% year to date-helps explain the extra boost. (But expect oil to remain range bound from here, with US production ramping up.)

Fears over bank solvency were rampant in early 2016-partly due to oil patch exposure, partly fears over a contagion stemming from Europe-but also faded later. And, importantly, political uncertainty fell-those fearing a calamity from Brexit and/or the US election were likely comforted by markets' response. The vast reduction in uncertainty made demand for high-quality sovereign debt fall and demand for higher yielding corporates rise.

Looking forward, we expect further corporate outperformance, at least initially next year. But we aren't sold on the notion rates are going to materially rise. There is a near-uniform view rates will rise in 2017, similar to 2014, when the world was convinced the Fed's taper meant higher rates. That increases the probability markets already reflect the view that higher rates are coming, mitigating the likelihood that actually happens.

[i] Source: FactSet, as of 12/29/2016. Bank of America Merrill Lynch Treasury, US Corporate and US Corporate High Yield Index total returns, 12/31/2015 - 12/28/2016.

[ii] We're getting beyond bond basics here, but in a bankruptcy event the bondholders will recoup before equity holders, so lower risk but also less return and hence less volatility (in general!) versus the stock.

[iii] They're actually not risk free. While you don't have to worry about getting paid, inflation risks and opportunity costs figure prominently when owning Treasurys.

[iv] Source: FactSet Earnings Insight Report for week ending 12/23/2016.

[v] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

-

Expert Commentary Ken Fisher on Crypto, Inflation, AI Bubble and Annuities

2026-06-16

2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today