Personal Wealth Management /

There Is Nothing Magical About Record Highs

Market index levels aren’t telling of where stocks will head next.

Buy low. Sell high. That’s every equity investor’s goal, and it seems simple, right?[i] Markets have been clocking one all-time high after the next, which may make it seem logical to presume markets are now high—especially with headlines haranguing about the allegedly dreary state of the world. But bull markets tend to set many new record highs along the way—it’s a function of their tendency to, you know, go up. Determining when stocks are actually “high” and not time to buy will take far more analysis than looking at an index level, which holds zero predictive power for future market direction. How folks react to market movement, however, can give you a clue—it’s a sign of sentiment, and in our view, sentiment surrounding recent records suggests this bull market has plenty of new highs ahead.

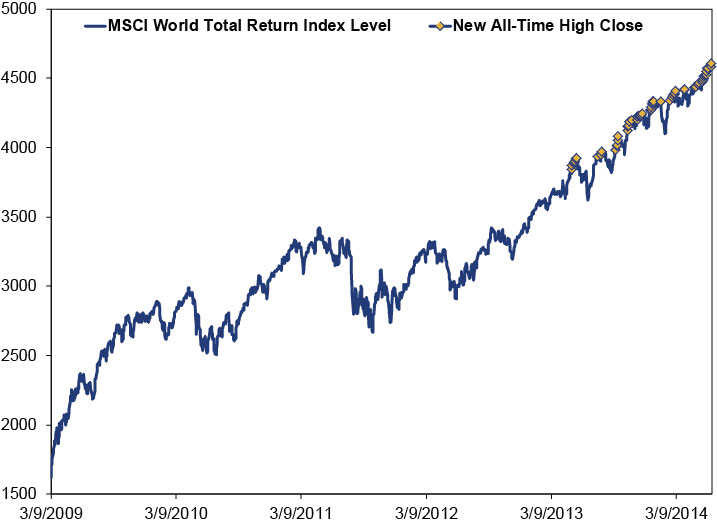

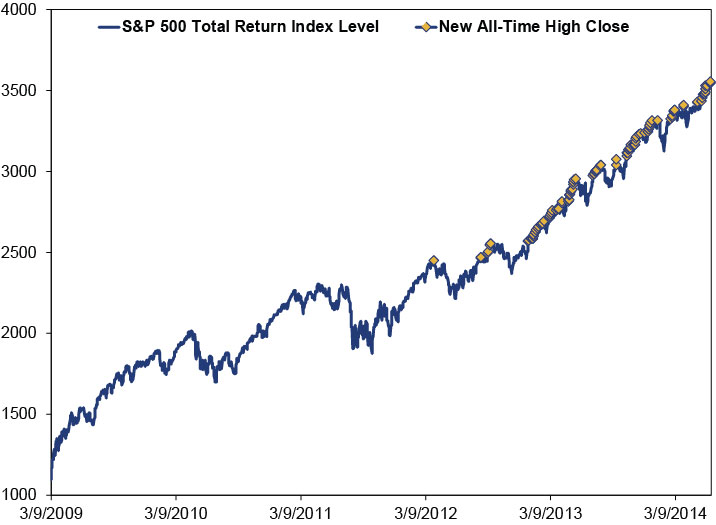

Since the bull began, the MSCI World Total Return Index and the S&P 500 Total Return Index have hit 62 and 106 all-time highs, respectively, through Friday’s close. (Exhibit 1 and 2) Plenty other indexes have steamrolled through round numbers, landmark levels and all-time highs, too, and many major financial publications are on big round-number watch: Dow 17,000, S&P 2,000. The NASDAQ is inching toward its Tech Bubble-era peak. The FTSE 100 is also very close to its 1999 record high (6,950.60). Germany’s DAX just marched past 10,000.

Exhibit 1: MSCI World Total Return Index

Source: FactSet, as of 6/23/2014. MSCI World Total Return Index, 3/9/2009-6/20/2014.

Exhibit 2: S&P 500 Total Return Index

Source: FactSet, as of 6/23/2014. S&P 500 Total Return Index, 3/9/2009-6/20/2014.

Now, the correct interpretation is simple: Past returns don’t predict future performance. All-time highs are just things that happen as markets rise, which is what markets tend to do more often than not. Yet rather than seeing all-time highs as normal in a maturing bull, the media seems more intent in puzzling over why they’re happening. They see it as a sign of disconnect with what they see as a still-troubled world: Ukrainian troubles, Iraq, bouncy economic data, the Fed supposedly dialing back its so-called stimulus and the like—irrational exuberance, if you will. Yet the world has been imperfect since right about the dawn of always. Stocks simply do not need a pristine economic or geopolitical environment to advance, whether to new highs or to bounce off the bottom of a bear. That stocks are rising amid strife and turmoil isn’t a sign investors are blind to risk. It is just stocks doing what stocks do.

Fears accompanying all-time high announcements is a good sign—it means we haven’t reached the confetti-dropping bullish celebration of our supposedly “new economy” that typically happens when markets are euphoric. It also shows folks are focused on the wrong things and ignoring what really matters. Consider: Headlines have spent the past year-plus grousing about record-highs, calling Dow 15000 a “disconnect” from a “ho-hum economy” and the S&P at 1700 “astoundingly expensive” and at risk of a “historic crash.” The triple threat of Dow 16000, S&P 1800 and Nasdaq 4000 “fed fear of bubbles” last November. For all the reasons they’re doomy and gloomy now. Yet, through it all, corporate earnings and revenues kept rising. The world wasn’t a perfect place, but its many troubles didn’t knock the profitability of publicly traded companies—what you own if you own a stock.

Looking ahead, the question isn’t when stocks will finally wake up and realize countries are fighting and growth slowed a few months ago. Stocks already know! The world’s worries have been widely discussed for a long, long time. What really matters is whether investors’ expectations for the economy and earnings are too high or low. While folks aren’t as dour as they were in 2009 or 2010, they don’t exactly expect the moon. Headlines are hung up on a Q1 GDP contraction, waiting to see whether it’s revised down again this week—few notice the high and rising Leading Economic Index, wider yield curve spread, pickup in bank lending or rising manufacturing orders. Stocks see all that—they see the high likelihood growth continues. But people don’t. There remains a big wall of worry for this bull to climb.

[i] We guess if you are a short-seller your goal is to sell high and buy low, which is the same thing, just in the reverse order.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today