Personal Wealth Management / Market Analysis

These PIIGS Went to Market

A look at falling Italian and Spanish debt yields.

A month into 2012, there’s still ample focus on the PIIGS. After all, as recently as Q4 2011, yields at auction for some maturities of both Italian and Spanish debt were hitting 7%—a level many believed (incorrectly, in our view) was automatically disastrous.

For the two PIIGS still going to debt market (Italy and Spain, the others have been bailed out), where are we now?Debt auctions so far have largely gone just fine, with ample coverage and falling yields.

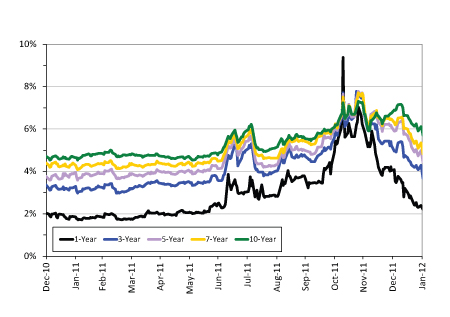

Italy represents 59% of the PIIGS debt to be rolled over in 2012 and is thus the core eurozone issue in 2012. But it gets past some key funding hurdles fast—by April, Italy will have rolled over 47% of its debt coming due in 2012. In February alone, the country must roll over €53 billion. Early auctions this year have been encouraging—yields thus far on all maturities have moved lower from 2011 peaks, as shown in Exhibit 1.

Exhibit 1: Italian Yields on Key Maturities (Since 12/31/2010)

Source: Thomson Reuters; as of 2/2/2012.

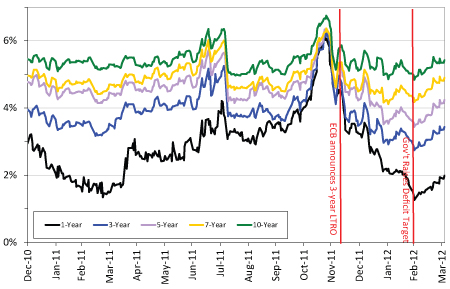

Spain represents a healthy chunk of maturing 2012 PIIGS debt, but must rollover less than half the amount Italy does. And only a month into 2012, Spain’s already addressed a significant portion of their refinancing needs (roughly 46% of debt with maturities greater than one year). (See Exhibit 2.) Spain has no additional debt of significance maturing until July, when €11.2bn of 10-year bonds come due.

Exhibit 2: Spanish Yields on Key Maturities (Since 12/31/2010)

Source: Thomson Reuters; as of 2/2/2012.

Will subsequent Spanish and Italian auctions go so well? Hard to know, but expectations remain very dour, so even mediocre results will likely prove a nice positive surprise—another incremental tailwind for stocks this year.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today