Personal Wealth Management /

This Is Your Brain on Markets

Your mind can play tricks on your portfolio—being aware of them early may be your best defense.

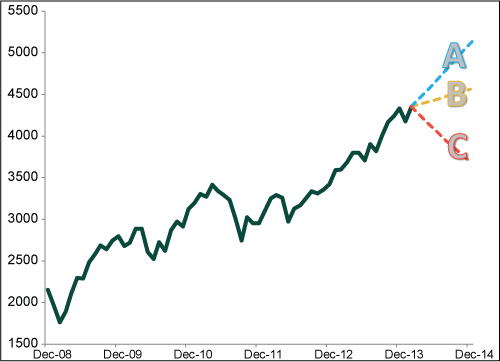

Quick! Look at Exhibit 1! Which line best represents how you think markets will fare in the balance of 2014? A, B or C?

Exhibit 1: MSCI World Net Return Index

Source: Factset, MSCI World Net Return Index Level, 12/31/2008 – 02/28/2014. Lines A, B and C are hypothetical, straight-line extrapolations of returns used to illustrate a point. No market, ever in history, has provided smooth, straight-line returns.

What was your decision based on? My experience suggests most folks would base their choice at least partly on the direction of the line representing the actual results. Their outlook would hinge on past returns—a fallacy of the highest order in investing.

Past returns do not presage the future, but folks often eschew this fact, particularly at inflection points in markets—tops of bulls and bottoms of bears. Typified by extremes in mass psychology, the popular sentiment in media and the public is likely to be some variation of, "It's different this time." "The economy has changed."

In the 1990s, this was “The New Economy.” After a hot 1999 with 85% returns, most folks zeroed in on the NASDAQ and thought the good times would keep a rollin’. On cable television, debaters fought over whether 1999 was just a sign of a super bullish cycle ahead—or if the New Economy had fundamentally eliminated “bust” from the economic cycle, leaving only “boom.” (And, I guess, “and.”) Forecasts went ever further into the future and reached higher and higher heights. In Exhibit 2, the dashed blue line extrapolates the tech bubble’s trend forward—what many projected Tech stocks would do—the yellow line is the actual dot com bust that followed.

Exhibit 2: Hypothetical Extrapolation of Q4 1999 NASDAQ Returns vs. Actual Result

Source: Factset. NASDAQ Composite Index level, 09/30/1999 – 09/30/2002. Hypothetical line (blue dashes) is a straight-line extrapolation of average daily return for the period 09/30/1999 – 03/24/2000 for illustrative purposes only. No market, ever in history, has produced straight-line results.

At the last bear market’s depths in March 2009, many thought a very dissimilar “new economy” had emerged. 1999’s and 2009’s new economies, only about a decade apart, were light years separated in sentiment terms. In 2009, it was again different this time—but for the worse. More downside lurked. A new depression. Stocks, some said, were dead. Many investors thought if stocks ever recovered, it would take a decade (or more) to do so. In Exhibit 3, the dashed blue line extrapolates the trend of the financial panic’s trend from September 2008 through March 2009. Instead of plunging toward zero by autumn, the yellow line shows the sharp, V-shaped bounce higher typical of new bull markets.

Exhibit 3: S&P 500 Price Index Level, August 31, 2008 – December 31, 2010

Source: Factset, S&P 500 Price Index level, 08/31/2008 – 12/31/2010. Hypothetical line (blue dashes) is a straight-line extrapolation of average daily return for the period 08/31/2008 – 03/09/2009 for illustrative purposes only. No market, ever in history, has produced straight-line results. And if the blue dashed line ever actually happened, stocks would likely not be your most immediate concern.

Your mind extrapolates recent returns forward, often to lengths you’d never think rational in a time less fearful or less greedy—true of professionals and individual investors alike. Today is not a time of extreme sentiment like those shown in Exhibits 2 and 3. But should this bull market peak as they most often do, extreme greed will come, and eventually, sickening, mind-bending fear. The key is to prepare yourself now for these eventualities—to understand they are a function of your brain on the extremes of a normal market cycle. Markets may not make your brain sizzle in a pan, but they can just as easily fry it. Any questions?

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Chart of the Day: Oil’s Substitution Effects, Illustrated2026-06-03

-

Economics Rising Credit Card Delinquencies in Context2026-06-02

-

Market Insights Ken Fisher on Inflation, Sell America, US National Debt and More - June 20262026-06-01

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US Jobs, Estate Planning

2026-06-01

2026-06-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today